Table of Contents

What is Sutton Bank, and how is it Linked to Cash App?

Sutton Bank is a privately held independent, community bank founded in 1878 and currently headquartered in Attica, Ohio. With its initial purpose to serve the growing needs of local merchants and farmers, the bank has long been a community pillar, staying strong through the Great Depression, times of war and fluctuating economies.

Cash App is a financial technology app developed by Square, a popular payment processor. In December 2021, Square changed its corporate name to Block, separating the corporate entity from its subsidiary businesses that it calls its “building blocks”, namely Square, Cash App, Spiral, Tidal, and TBD. Cash App’s core product is a mobile money management platform that you can use to send and receive money from other people and companies and is currently only available in the United States.

Cash App outsources basic banking functions to two FDIC-insured partner banks, Sutton Bank and Lincoln Savings Bank. Sutton Bank Cash App provides Prepaid Debit Card (Cash Card) related services and is by far the more visible bank partner. When the cash app users apply for the cash card to make online and offline transactions then that cash app debit card is offered by Sutton bank.

Lincoln Savings Bank supports the Direct Deposit feature of the Cash App. Cash App also provides access to market-traded securities and bitcoin. This is done through Cash App Investing, LLC, a subsidiary of Cash App. Cash App’s bank partners are not directly involved in its investment services.

What are the Specifics of Cash App

Cash App is a platform that facilitates peer-to-peer (P2P) money transfers for both consumers and merchants through its mobile application.

In order to login to Cash App users aren’t required to hold a bank account, as the app will work normally without any connected bank account. Nevertheless, if a user wants to access Cash App’s balance easily and especially use that balance for real-life purchases, they will need a Cash Card. Furthermore, users will need to link their Cash app card to Apple pay or Google pay to make transactions. Once the account is set up, users can easily send money to friends, family, and businesses, provided the recipient also has a Cash App account. The money received will be added to the user’s Cash App balance, which can then be transferred to a bank account.

For merchants, it is important to have a “business account” on Cash App. Converting a personal account to a business account can be done easily by going to the “Edit Profile” tab in the app. With a business account, merchants can accept payments from customers through payment links and QR codes.

Conversion on Prepaid Cards from Sutton Bank

For first payments the conversion rate for prepaid cards from Sutton Bank on the US location is higher than in the EEA (European Economic Area), only failing on the MCC 7273 (Dating and Escort Services). For dating businesses the conversion rate on Sutton Bank’s prepaid cards is between 10-25%.

On the other hand, we see an adequate conversion rate for the following MCCs on the EEA locations:

- 7339 (Stenographic and Secretarial Support Services),

- 8111 (Attorneys, Legal Services),

- 8999 (Professional Services–Not Elsewhere Classified).

With regard to the breakdown by BINs, the following BINs show a zero conversion for non-dating services: 486533, 464252, 411361, 451709, 532079, 454677, 493435, 427693, 475410, 415984, 475484, 478402.

Some BINs show quite a high conversion for non-dating MCCs, for instance, take a look at the following results in April 2023:

- BIN 441707 with the conversion rate of 62% for first payments and 18% for recurring payments;

- BIN 408138 with the conversion rate of 42% for first payments and 11% for recurring payments;

- BIN 440393 with the conversion rate of 42% for first payments and 9% for recurring payments.

For dating services some BINs show a better conversion rate than others. We see that BIN 440393 performs best for recurring payments in comparison with any other BIN on dating-related transactions:

- BIN 440393 with the conversion rate of 20% for first payments and 29% for recurring payments for April 2023;

- BIN 411810 with the conversion rate of 21% for first payments and 4% for recurring payments for the same investigated period;

- BIN 408138 with the conversion rate of 7% for first payments and non-representative data for recurring payments for the same investigated period.

For recurring payments the higher the amount of a transaction is, the lower is the conversion rate. On average, conversion for transactions with a token is not higher than 10%.

Prepaid cards are rarely eligible for processing recurring payments, as they hold a limit to their funds. For example, prepaid cards with BIN 411810 simply do not process recurring payments, thus the “Invalid Transaction” error is returned. It is worth mentioning that when a prepaid card runs out of funds, its number becomes incorrect, and accordingly, the “Invalid card number error” is returned for subsequent transactions.

What are the Common Cash App Scams

Cash App’s popularity has been on the rise, in part due to its weekly cash giveaway campaigns such as #CashAppFriday. To become eligible for these giveaways, users must engage with the app on social media platforms by retweeting or replying to posts with their unique ID for sending and receiving money, called $cashtag.

However, scammers have started to target Cash App users and their $cashtags on social media platforms like Twitter, Instagram, and YouTube. According to the Better Business Bureau, these scams have replaced wire transfer or prepaid debit card scams, with victims being blocked by the scammer as soon as they send the funds.

While Cash App is a great platform for transferring money between individuals using a mobile app, users need to be cautious of potential dangers posed by scammers. Some of the most common Cash App scams include Cash App flipping, fraudulent payment claims, pet sale scams, rental scams, cash App Fridays, investment scams, Cash App impersonation and phishing scams, fake accidental transactions, gift card scams, cat phishing scams.

For instance, through Cash App flipping scammers target Cash App giveaway comment threads to find potential victims whom they direct message, claiming to be successful Cash App “flippers” who can turn a small amount of money into a larger sum, but once they convince the user to send them funds, they disappear with the money, and they might refer to it as a “money circle” scam. Gift card scams mean that scammers persuade victims to purchase prepaid gift cards on their behalf to gain trust before paying out Cash App giveaway money, then use the card information provided by victims to steal the card and never pay out the money.

If a user has been scammed, they may dispute the transaction through Cash App, in case there is a chance of getting a refund for any fraudulent Cash App payments. Then they might contact their financial institutions if they feel their accounts or other financial information, like bank account number, has been compromised.

How to Dispute a Transaction in Cash App

In 2020 a class action lawsuit was filed against Cash App creator Square, Inc. and Sutton Bank by the Financial Justice Initiative on behalf of customers who have reported fraudulent charges. The lawsuit alleges that Square and Sutton Bank did not follow the law when dealing with disputed charges, requiring excessive information from customers and denying claims without adequate proof. That is because quite often users are required to provide evidence of their claims. Examples can include photos, screenshots of messages between merchant and buyer, receipts, shipping, tracking, etc. Relevant documents will vary depending on the circumstance.

The lawsuit further alleges that Square and Sutton Bank failed to provide proper disclosures and explanations for their decisions, impacting thousands of people who use Cash App.

Fraud on the Cash App platform has been widely reported, making it critical for Square and Sutton Bank to provide proper and adequate dispute procedures for their customers.

Cardholders can dispute a transaction if the item was significantly not as described, never arrived, arrived damaged, there were incorrect charges, or if there were fraudulent charges made on their account, by contacting Cash App’s support through the app, website, phone, or mail.

If fraud is suspected on a Cash App account linked to a credit card, users should contact their bank and Cash App immediately to report the fraud and dispute the charge. Reporting fraud to the FTC is also recommended to help prevent future occurrences.

Upon completing a transaction with a Cash Card, the buyer’s account is debited before the transfer to the merchant’s account; during this ten-day pending period, cancellations are possible but disputes are not allowed.

When filing disputes on Cash App, cardholders must provide evidence to support their claims, and the merchant or service provider will have a chance to respond with their own evidence. Filing invalid disputes can result in serious consequences.

For cardholders, there are two potential outcomes of a Cash App dispute:

- Cash App rules in favor of the cardholder, and the funds from the transaction are returned.

- Cash App rules in favor of the merchant, and the funds from the transaction are returned to the merchant.

If the cardholder cannot provide proof to support their claim, the funds will be taken from their account and given back to the merchant. P2P payment apps like Cash App are vulnerable to fraud, including scams using stolen bank account information to fund Cash App accounts, as discussed in the previous section.

What are the Consequences of Cash App Disputes for Merchants

If Cash App determines that no fraud has occurred and the merchant provides evidence to support their case, the company may side with the merchant and return the funds to their account.

If Cash App determines that the merchant didn’t provide the goods or services described to the customer, funds may be returned to the cardholder. It could also happen in the event of fraud.

If a merchant accepts the refund request, the process takes up to 10 days, and the funds are returned to the buyer.

If the matter remains unresolved, the cardholder has the right to file a chargeback with their issuing bank, which can result in chargeback fees and penalties for the merchant.

Even though P2P apps like Cash App may not pose as much of a direct chargeback threat, the dispute process is still a significant risk to consider before using this option for payment.

Consider these scenarios:

- Best-case scenario for merchants is if Cash App rules in their favor and returns the funds to their account.

- Worst-case scenario for merchants is if the cardholder files a chargeback, which can result in chargeback fees and penalties.

- In cases where the cardholder has a credit or debit card linked to their account, they can still file a chargeback, resulting in revenue loss and additional fees for the merchant.

How to Prevent Cash App Chargebacks & Disputes

Under US law, chargebacks exclusively pertain to payment card transactions. Thus, merchants cannot use the chargeback process for transactions made through Cash App that don’t involve a credit or debit card, which may be appealing for those who want to avoid chargebacks.

Cash App may not be suitable for all businesses, especially enterprise operations, and customer support is limited. Strong anti-fraud tools and tactics, such as address verification, CVV checks, and risk threshold rules, are essential when using Cash App for business to mitigate chargeback and fraud risks.

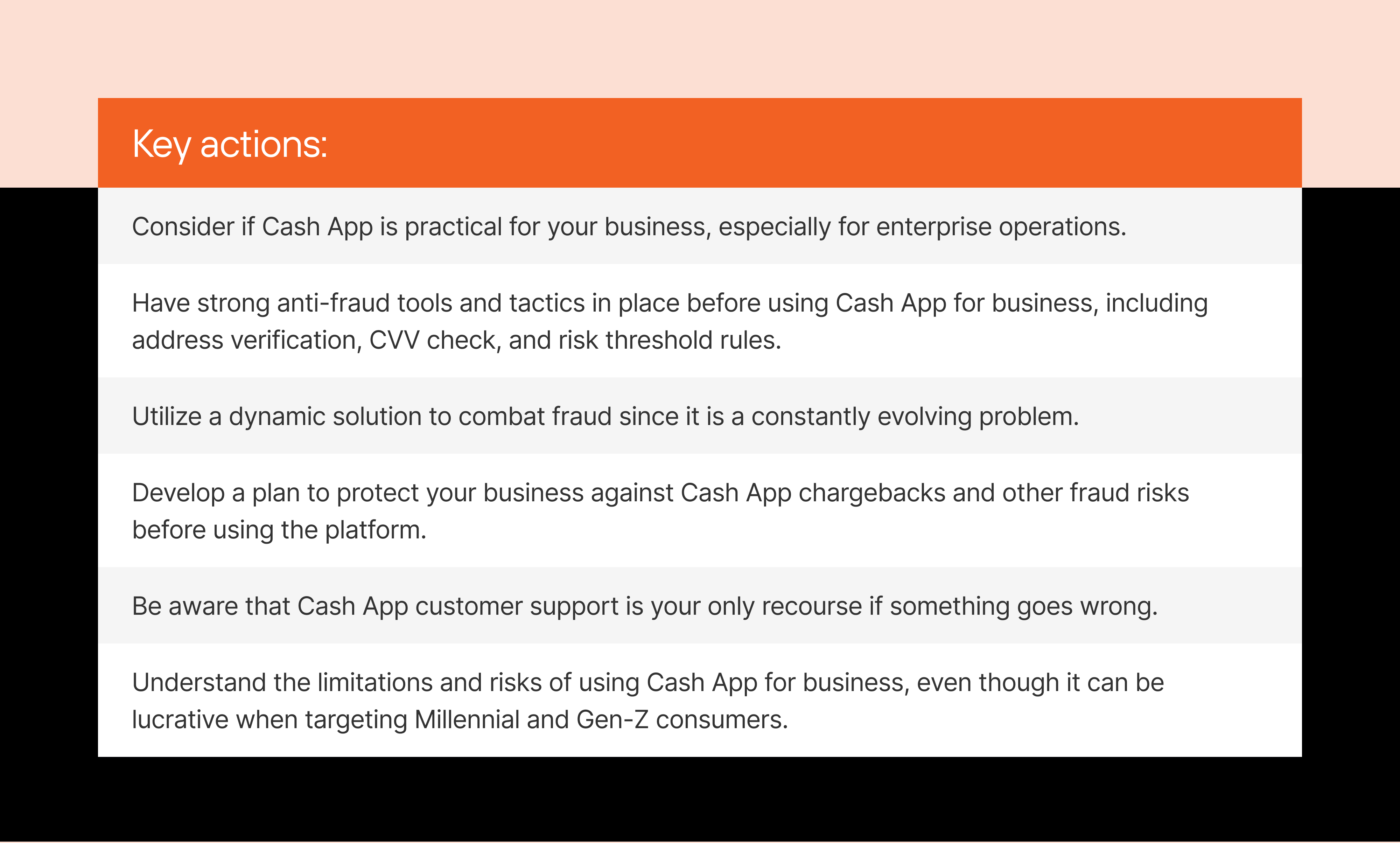

Key actions:

- Consider if Cash App is practical for your business, especially for enterprise operations.

- Have strong anti-fraud tools and tactics in place before using Cash App for business, including address verification, CVV check, and risk threshold rules.

- Utilize a dynamic solution to combat fraud since it is a constantly evolving problem.

- Develop a plan to protect your business against Cash App chargebacks and other fraud risks before using the platform.

- Be aware that Cash App customer support is your only recourse if something goes wrong.

- Understand the limitations and risks of using Cash App for business, even though it can be lucrative when targeting Millennial and Gen-Z consumers.

Conclusion

Cash App has an in-house dispute process for chargebacks that begins after payment finalizes. Chargebacks are only applicable to credit or debit card payments, not bank transfers or Cash App balances. Merchants need to present evidence of transaction legitimacy, and being deemed fraudulent may result in Cash App banning the business from the platform. Fraud prevention measures, such as collecting transaction information, can help merchants avoid friendly fraud. Cash App cannot be the sole source of processing for businesses since it only supports payments from other Cash App accounts. Understanding the Cash App dispute process and maintaining good business practices can help businesses avoid chargebacks and save on account fees. Dispute resolution can take around ten days, but if the merchant contests the dispute, it can take longer. Cash App refunds depend on the circumstances, and scams can be avoided by ensuring legitimate money transfers. Chargebacks on Cash App only apply to card purchases, and users cannot file chargebacks for bank transfers or Cash App balances.