Credit card vault: Why your payment stack needs one

Payments 101

18 Feb 2026

8 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

A credit card vault gives you control over your payment credentials – cutting failed charges, reducing PCI scope, and freeing you from processor lock-in. Here's how it works and what to look for in a provider.

Who actually controls your customers' payment credentials right now?

If they live inside a single processor's system, the answer isn't you. That processor decides what happens when a card is reissued. They decide how hard it is to switch providers. And if they go down, your billing goes down with them.

A credit card vault – also called a token vault – changes that dynamic. It sits at the center of your payment stack as the single source of truth for stored payment credentials, independent of any one processor.

Understanding how a credit card vault works is crucial for your business because it enables you to:

- Reduce fraud

- Improve payment acceptance rates

- Eliminate processor lock-in

- Cut compliance overhead

- Lay the groundwork to scale into new markets without rebuilding your infrastructure from scratch

This article is for payment operations managers, fintech product leads, and anyone responsible for payment infrastructure decisions. Here, we cover what a credit card vault is, how it works, what it actually unlocks operationally, and where Solidgate Token Vault fits in.

What is a credit card vault, and how does it work?

A credit card vault is a secure, centralized system that stores customer payment credentials like card numbers (PANs), expiry dates, and cardholder names in tokenized form.

Instead of your own systems ever touching original credit card data, the vault replaces it with a randomly generated token that flows through your payment stack to whichever processor you need. The actual credentials are stored securely in the vault, encrypted, and access-controlled.

The token has no intrinsic value. If intercepted anywhere in the chain, it's useless to a fraudster.

Because the token persists across the customer relationship, it powers everything from one-click checkout on the first repeat purchase to the 48th subscription renewal, without the customer ever needing to re-enter their payment details.

Credit card vault vs. network tokenization: What's the difference?

These terms get conflated, but they're distinct layers that work together. To clarify the relationship:

| Credit card vault | Network tokenization |

| Your merchant-controlled credential store; | A card-scheme-issued token that replaces the PAN for a specific merchant-device combination. |

| The infrastructure layer that gives you portability and control. | Lives on top of your vault. |

The best vault implementations support both: they store credentials and handle network token lifecycle management. You get the control of a merchant vault and the approval rate benefits of scheme-level tokenization in one place.

7 reasons your payment operations need a credit card vault

1. Stop losing revenue to failed payments

reported cancelling a subscription last year due to payment or billing problems. On average, subscription businesses risk losing between 5.6% and 8.3% of their customer base every month to payment failures caused by outdated payment details.

That's revenue lost to payment infrastructure, not product problems.

Cards expire. Banks reissue cards after fraud events. Account upgrades change card numbers. Each of these events invalidates stored credentials and turns a paying customer into a lapsed one, often without either party realizing it.

A credit card vault integrated with account updater services resolves this automatically.

When a card is reissued, the network pushes updated credentials to the vault, the token stays valid, and the next charge goes through. No customer action, no manual intervention, no churn.

2. Remove provider lock-in

When a processor holds your raw card data, switching is a project measured in months. You need their cooperation to migrate, you often can't test an alternative without committing to it, and they know it. That leverage shows up in every rate negotiation.

With a processor-agnostic vault, your tokens are portable. Adding a backup processor, running an A/B test on authorization rates, or switching entirely becomes a routing configuration change. Your customers don't re-enroll, and their payment experience doesn't change.

3. Get higher authorization rates

A secure vault that supports network actively improves your authorization rates. Issuers treat network-tokenized transactions as lower fraud risk because the token ties cryptographically to a specific merchant and device. This way, it's useless outside that context.

That trust translates into fewer unnecessary declines.

Across Solidgate's customer base, tokenization via VTS and MDES produces acceptance rates up to 15 percentage points higher than non-tokenized transactions with the same cards. At scale, it's material recovered revenue on every billing cycle.

4. Route payments intelligently across providers

Smart routing requires a centralized credential layer. Without a vault, routing the same transaction to different processors means either:

- Sharing raw card data with multiple parties creates a compliance and security problem

- Maintaining separate token mappings per processor, which scales poorly and creates operational debt

With a vault, a single token gets translated and routed to whichever processor your logic selects.

5. Own your customer payment data

Payment credentials stored in a merchant-controlled vault are a business asset. They represent your relationship with each customer's payment method, independent of which processor handles any given transaction.

That means:

- One-click checkout for returning customers

- Subscription/recurring billing without re-enrollment

- Ability to migrate providers without disrupting a single recurring charge

When credentials live in a processor's system under their terms, that asset is effectively on loan. Storing credentials in a vault you control means that data is yours.

6. Shrink your PCI DSS compliance footprint

(Payment Card Industry Data Security Standard) scope is determined by which of your systems store, process, or transmit cardholder data. The wider the scope, the more expensive and time-consuming every compliance cycle becomes – quarterly scans, annual assessments, and documentation overhead.

A vault removes raw card details from your environment entirely. What remains in your systems are tokens: non-sensitive, out of PCI scope.

Your internal systems qualify for simpler self-assessment questionnaires (typically SAQ-A, the shorter annual self-assessment form, rather than the multi-week SAQ-D process).

7. Scale to new markets without rebuilding your credential layer

Adding a new geography typically means integrating a local processor, adapting to local payment methods, and navigating data residency requirements.

Without a vault, each new market can also mean re-collecting credentials from existing customers or attempting a complex migration with your provider.

A multi-region vault handles this at the infrastructure level. Tokens map to local processors without customer re-enrollment. Data residency requirements like GDPR in the EU get addressed by routing credential storage to vault instances in the right jurisdiction.

Entering a new market becomes a processor and compliance configuration, not a credential management project.

Should you build a credit card vault in-house or use a third-party provider?

The answer depends on how many resources you’re willing to put into this project. For most high-growth companies, the engineering and compliance commitment is way too high. You need to:

- Achieve and maintain PCI DSS Level 1 certification. It’s the highest tier requiring an on-site QSA assessment, extensive documentation, and significant ongoing security investment.

- Build and maintain the account updater integrations, network tokenization connections to Visa and Mastercard, multi-region data residency architecture, and processor translation layers.

- Make the vault scalable. Building a vault that scales with and adapts to your needs demands meaningful engineering and compliance commitment that doesn't get cheaper as you scale.

For most growing businesses, the question isn't really build vs. buy – it's which third-party vault gives you the most control, the broadest processor compatibility, and the clearest path to network tokenization.

The key things to evaluate in a provider:

- Is it processor-agnostic, with full token portability and no re-tokenization required when switching providers?

- Does it support Account Updater for both Visa and Mastercard?

- Does it support network tokenization (VTS/MDES) natively?

- How does it handle multi-payment-method storage – cards, digital wallets, alternative payment methods (APMs)?

- What are its data residency capabilities for the markets you operate or plan to enter?

- What compliance certifications does it carry (PCI DSS version, ISO 27001, SOC 2)?

How Solidgate Token Vault simplifies token management

Solidgate is a offering a unified payments infrastructure layer. Our sits at the core of a broader payment infrastructure stack, natively connected to intelligent routing, subscription billing, and revenue recovery.

It processes over 100 million tokens annually and handles tokenization, storage, and credential lifecycle management across cards, Apple Pay, Google Pay, and other payment methods.

Here’s what our vault allows you to do:

Improve authorization rates on every billing cycle

Solidgate issues network tokens through Visa Token Service (VTS) and Mastercard Digital Enablement Service (MDES). Issuers treat network-tokenized transactions as lower risk, which translates into fewer – up to 15% better acceptance rates compared to standard card-on-file.

Recover revenue you’re currently losing to card changes

When a card expires, gets reissued, or changes, Solidgate’s built-in automatically refreshes the stored credentials. Your next billing attempt goes through without any action from you or your customer.

The result is up to 27% fewer failed payments and up to 7.5% less involuntary customer churn.

Offer one-click checkout and frictionless upsells

Vaulted tokens power repeat payments, subscription upsells, and cross-sells with a single tap – no payment friction, no payment information re-entry.

Solidgate handles Card on File flagging and scheme compliance automatically, so you get the conversion lift without the compliance overhead.

Switch or add processors without touching your customers’ data

Your tokens route to any of Solidgate’s 100+ connected providers, such as Stripe, Adyen, Worldpay, Checkout.com, and others, without re-tokenizing or re-collecting card data.

You can test a new processor, add a regional acquirer, or migrate entirely, without your customers noticing.

Make smarter routing and risk decisions at the token level

Every token is enriched with real-time card metadata – BIN-level insights (Bank Identification Number data that reveals card type, issuing bank, and geography) – before you route.

That means routing logic that actually responds to card characteristics, not just transaction value or volume.

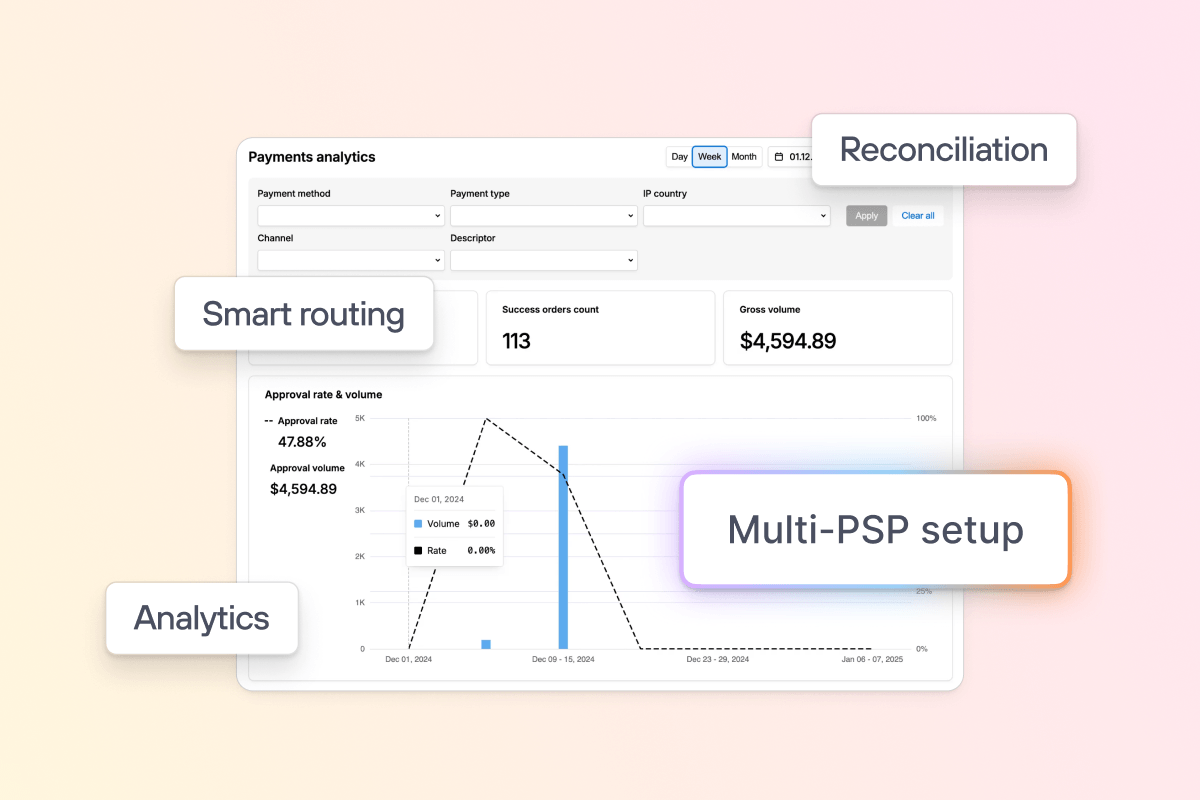

Our no-code, gives you direct control over your routing decisions, with complete transaction visibility from the Solidgate Hub.

Cut your PCI compliance burden

Solidgate Vault is certified to PCI DSS v4.0, ISO 27001:2022, SOC 2 Type II, and GDPR. Raw card details never touches your environment, which means your internal systems stay out of PCI scope — and your compliance cycles get shorter and less expensive.

Get a deep understanding of your payment data and optimize for the best payment routes

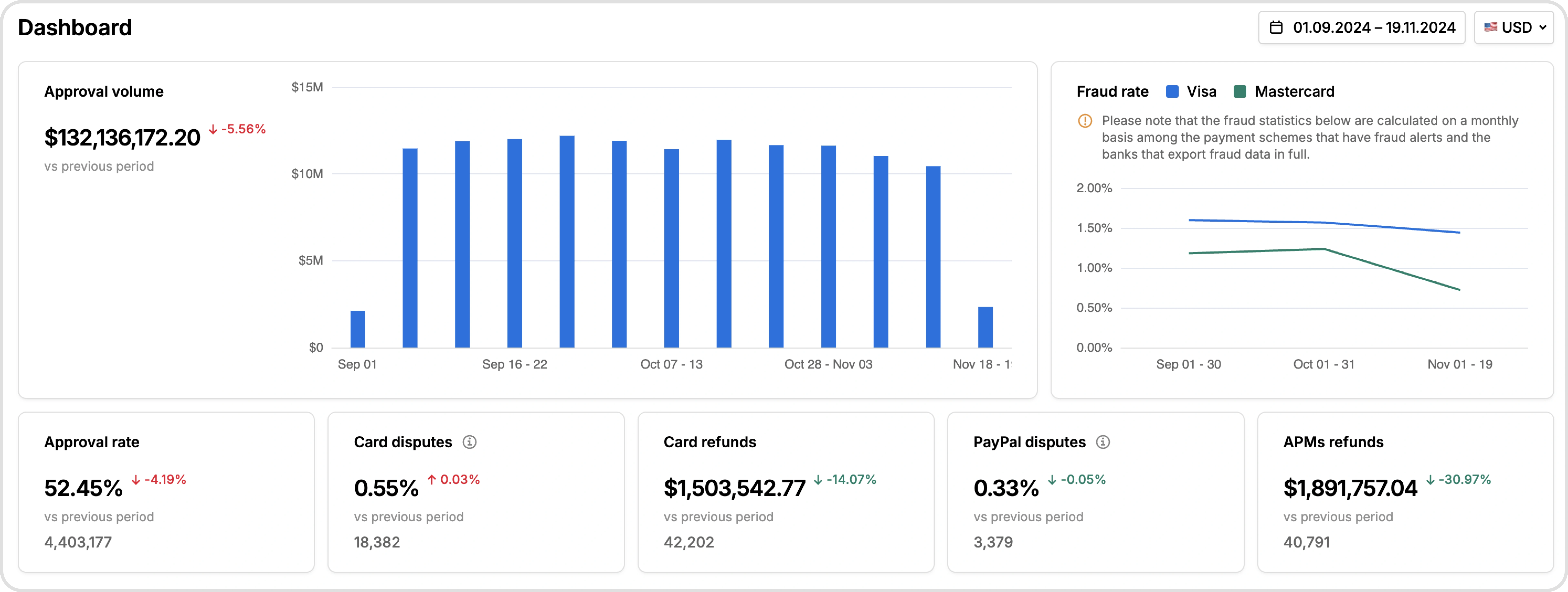

Most payment problems show up in the data before they show up in your revenue. Solidgate Hub gives you a single view across all your providers, payment methods, and token flows.

You get real-time transaction monitoring, acceptance rate trends broken down by acquirer and payment method, and settlement reports across your full multi-provider setup. If a processor's authorization rate drops on a specific card type or geography, you see it in the dashboard and can act on it.

It's the layer that makes routing, redundancy, and processor testing decisions measurable. You can act on it continuously, not configure once and leave.

Why card vaulting is becoming a baseline

Card vaulting does more than protect card data. It’s the infrastructure layer that determines how much control you actually have over your payment operations – who you can route to, how much revenue you recover, and how fast you can move when the business needs to.

Solidgate Vault is built for businesses that have outgrown single-provider dependency. If you're ready to take ownership of your payment credentials, with our payment experts.

Frequently asked questions

By replacing raw card numbers with non-sensitive tokens before any data touches the merchant's own systems. Even if internal systems are compromised, there's no card data present to steal. The vault itself holds the mapping between tokens and real credentials, operates under Level 1 PCI certification, and applies strict access controls to any detokenization.

Tokens stored in a vault can be passed to local processors in any market without re-enrolling the customer. Multi-region vault architecture handles data residency requirements by storing credentials in the appropriate jurisdiction. Entering a new market requires integrating a processor, not rebuilding the credential layer.

When new payment methods are added, a vault-based approach keeps their credentials in the same secure, centrally managed system. PCI DSS scope stays narrow regardless of how many methods the business supports, because tokens rather than raw credentials flow through internal systems. Compliance reviews don't get more complex just because the payment method mix does.

A credit card vault is your merchant-controlled system for storing and managing payment credentials. It issues your own tokens and routes them to processors. Network tokenization (Visa VTS, Mastercard MDES) is a card-scheme-issued layer on top – it replaces the PAN with a network token tied to a specific merchant and device, which the card network manages and keeps updated.

The two work together: a well-built vault handles network token lifecycle as part of its credential management.

Yes, with a processor-agnostic vault that supports import and export of payment instruments. The migration process typically involves a secure transfer from your current token store, with the vault provider handling detokenization and re-tokenization under their PCI-compliant environment.

The key requirement: your current provider needs to cooperate with the export. This is one reason to move to a portable vault before you need to – not when you're mid-migration.

That's the core purpose of a processor-agnostic vault. Your tokens map to any connected processor while the vault handles the credential translation. You add processors, switch providers, or route intelligently across them without touching customer-facing enrollment or re-collecting card data.

Involuntary customer churn happens when a card changes, like expiry, reissuance after fraud, or account upgrade, where your stored credentials become invalid. Without a vault connected to account updater services, that failure is silent: the charge fails, the subscription lapses, and the customer may not notice until you try to reach them.

A vault with an account updater automatically refreshes credentials when the card network pushes updates, so the token stays valid and the next billing attempt succeeds.

Modern vaults store tokenized representations of cards, digital wallets (Apple Pay, Google Pay), and other payment instruments in a unified token model. This matters as payment method mixes get more complex: you don't want separate credential stores per method, each with its own security surface and compliance considerations. Look for a vault that handles multi-method storage natively, so adding a new payment type doesn't mean rebuilding your credential management infrastructure.