Network tokenization: How it works and why it matters

Payments 101

Updated 26 Jun 2026

12 min

Anton Tsyslytskyi

Product Manager, Solidgate

Network tokenization does more than prevent fraud. For subscription businesses, it lifts authorization rates, cuts involuntary churn, and grows customer LTV. Here's the full picture.

Network tokenization gets most of its press for one thing: security. Replacing raw card numbers with scheme-issued tokens does meaningfully reduce fraud exposure.

But if that's where the conversation stops, businesses are missing the larger commercial picture.

Businesses that adopt network tokenization don't lead with security when they explain the decision internally. They lead with authorization rates, involuntary churn, and LTV. The average business risks losing between 5.6% and 8.3% of its subscriber base each month to payment failures. That's the problem network tokenization actually solves.

This guide covers what network tokenization is, how it works, why it performs better than gateway tokenization, what it delivers commercially, and what implementing it looks like in practice.

TL;DR

- Network tokenization replaces raw card numbers with scheme-issued tokens managed directly by Visa or Mastercard.

- Unlike gateway tokenization, network tokens are portable across processors and update automatically when cards are reissued.

- The commercial impact compounds: higher authorization rates, fewer failed renewals, and frictionless upsells – adding up to +42.5% improvement in customer LTV for subscription businesses.

What is network tokenization?

Network tokenization is the process by which a card network – Visa, Mastercard, American Express, or another scheme – replaces a customer's real card number with a unique digital substitute called a network token. That token stands in for the PAN (primary account number) at every stage of the transaction, from payment initiation through to issuer authorization. Your customer's raw card number never touches your system.

Because tokens come from the scheme itself, the customer's bank recognizes them at authorization without friction. That direct relationship between scheme and issuer is what drives the authorization rate improvement.

Network tokenization for Visa, Mastercard, and local schemes

Visa and Mastercard each operate their own network tokenization program – Visa Token Service (VTS) and Mastercard Digital Enablement Service (MDES). They are both built on the – the shared technical standard that ensures a network token behaves consistently across processors and acquirers globally.

Some markets have their own domestic card networks operating alongside Visa and Mastercard – country-specific schemes that handle the majority of local card transactions. These local schemes are increasingly subject to tokenization mandates from their own regulators.

For instance, India's RBI, making card-on-file tokenization the standard for recurring payments in the market. Australia's Reserve Bank covering eftpos, the domestic debit network, including requirements for merchants that don't meet PCI-DSS minimums to stop storing raw card credentials.

Accessing VTS and MDES directly requires building integrations with each card scheme and maintaining PCI-certified vault infrastructure. In practice, most merchants access both programs through payment providers that already hold those scheme partnerships – Solidgate, Stripe, and Adyen among them. Coverage of local schemes varies by provider, which matters if you're processing in markets like India or Australia where domestic schemes are regulated.

How network tokenization works

When a customer completes their first transaction through a tokenized flow, the card scheme generates a token tied to that specific card, merchant, and transaction context. From that point forward, the raw card number never travels through your system again.

Each subsequent transaction using that token is paired with a unique cryptogram – a one-time verification code generated for that specific payment. The cryptogram authenticates the transaction without exposing underlying card data.

Even if a token is intercepted, it's useless: the cryptogram has already expired, and the token itself carries no value outside the authorized context.

The token also survives card reissuance. When a card is replaced – due to expiry, theft, or proactive bank reissuance – the card network updates the token automatically. The next billing cycle processes against valid credentials without any action required from the customer or your operations team.

That's the mechanism behind the retention impact. The customer doesn't know their card was reissued, the renewal processes cleanly, and the subscription continues.

Core insight: Each tokenized transaction generates a cryptogram that expires on use, making intercepted data worthless. When a customer's card is reissued, the token refreshes automatically – the payment flow continues without any action from the merchant or the customer.

Network tokenization vs gateway tokenization

Gateway tokenization – sometimes called PSP-level tokenization – is what most payment providers offer by default. When you integrate with a PSP, they store your customer's real card number on their servers and return a token you can use for future charges. That token works within their ecosystem.

The problem is that it only works within their ecosystem.

If you add a second provider for redundancy or better rates in a specific market, your existing tokens don't transfer. If your primary PSP experiences downtime and you need to reroute transactions, you're starting over with each affected customer's card credentials.

Network tokenization operates at a different level. The token is issued by Visa, Mastercard, or another scheme directly – not by your payment provider. The issuing bank recognizes it natively, independent of which processor submits the transaction. That structural difference produces three practical advantages:

- Token portability: The same token works across any processor connected to the card network. Switching or adding acquirers doesn't require re-tokenization – your stored credential base travels with you.

- Issuer trust: Because the token comes from the scheme itself, issuers treat it with a higher degree of confidence than a raw PAN. That trust difference shows up in authorization rates.

- Automatic card updater: When a card is reissued, the network updates the token.

Gateway tokenization is sufficient for businesses running a simple single-PSP setup with stable credentials and limited cross-border exposure. The moment you're managing recurring billing across multiple processors, or seeing authorization rate variance across geographies, network tokenization can be a more appropriate infrastructure choice.

Network vs gateway tokenization: [A comparison table]

| Network tokenization | Gateway tokenization | |

| Issued by | Visa, Mastercard, or card scheme directly | Your PSP |

| Token portability | Works across any processor connected to the card network | Stored at provider level – not portable across acquirers |

| Issuer trust | Issuer recognizes a scheme-issued token natively – higher inherent trust | Issuer receives the raw PAN at processing time – tokenization operates between merchant and PSP only |

| Card updater | Automatic – network updates the token when a card is reissued | Varies by provider |

| Best for | Recurring billing across multiple processors, multi-market optimization | Single-PSP setup with stable credentials |

Core insight: Network tokens are portable across any processor connected to the card network, and carry higher issuer trust because they come from the scheme itself. Gateway tokens are locked to one provider – switching or adding an acquirer means rebuilding your stored credential base from scratch.

Benefits of network tokenization for businesses

The security benefit is real. But it's not the only reason scaling digital businesses adopt network tokenization.

Smoother checkout means higher conversion rates

Checkout friction is expensive. According to , nearly two-thirds of shoppers still struggle with manually entering their card details, and 25% abandon carts specifically because checkout is too complex or slow. That's a direct, measurable conversion problem.

One of the most practical benefits of network tokenization is one-click checkout. There's no prompting to re-enter a card number, no manual form fields to trip over, and no reliance on a customer remembering to update stored details when a card expires.

The token stays valid because the card network manages credential updates in the background automatically.

For subscription businesses, a tokenized one-click flow means that every upsell, upgrade, and add-on offer can convert at a measurably higher rate than a flow requiring re-entry.

See our guide on .

Lower fraud directly lifts authorization rates

The relationship between fraud and authorization rates is often underappreciated. When issuers see high fraud risk attached to a transaction, they decline it. That decline isn't always about a stolen card. It's frequently about low confidence in the transaction's legitimacy based on risk signals.

Network tokenization removes a significant source of that risk. A token is merchant-specific and paired with a unique transaction cryptogram, which means even if it's intercepted, it's useless elsewhere. The stolen data can't be replayed at another merchant, so the usual mechanics of card fraud simply don't apply.

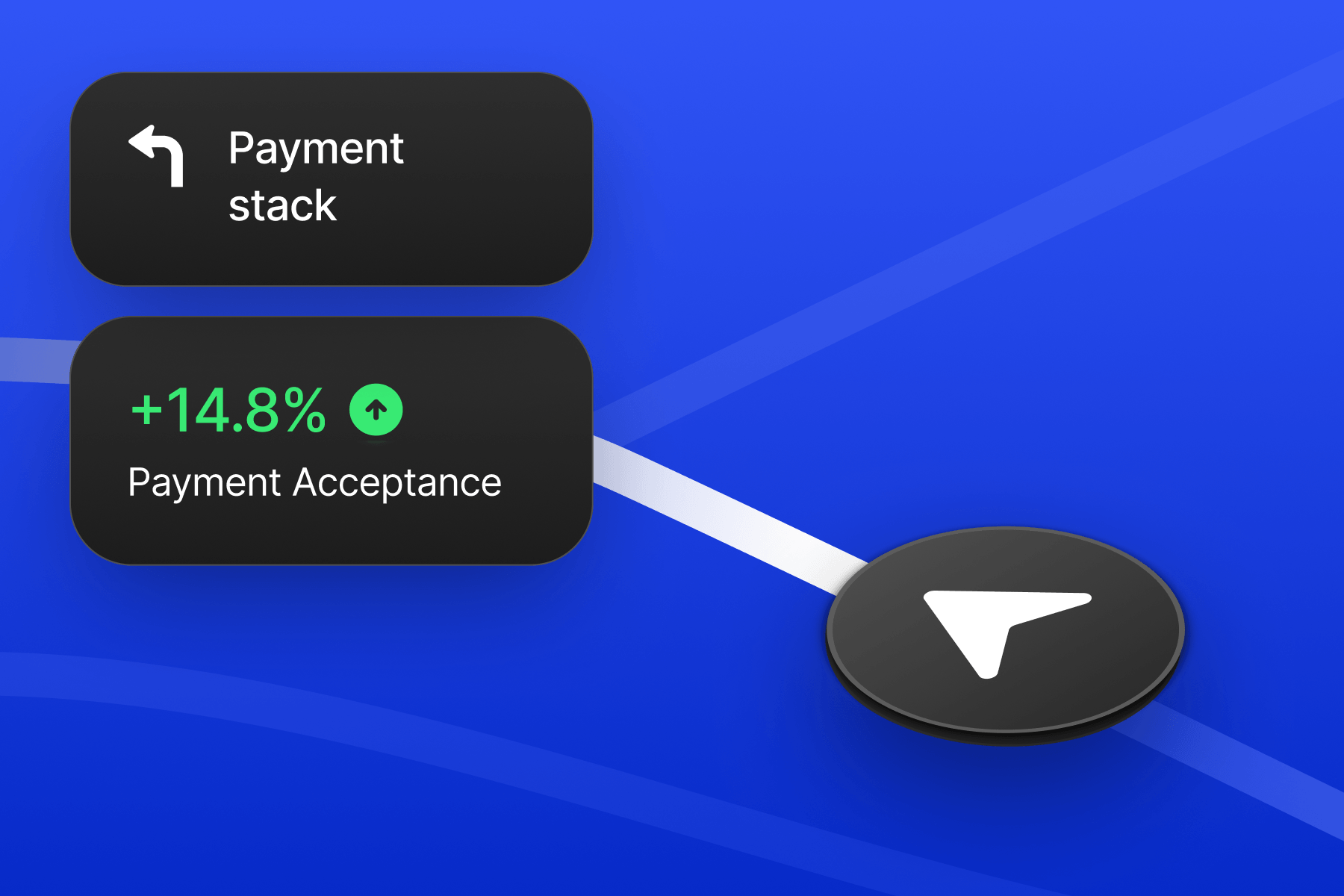

Visa data shows that tokenized transaction volume year-over-year – with approval rates up 6% and fraud down 30%.

For the full breakdown of , read our guide.

Higher customer LTV: less churn, more upsells

Network tokenization affects LTV through three connected mechanisms:

Fewer failed renewals

Subscription businesses lose customers every month to involuntary churn due to outdated card details. Based on our survey of 1,200 subscription businesses, the average business risks losing between 5.6% and 8.3% of its subscriber base each month to involuntary churn.

Learn more:

Network tokenization eliminates most of this category of loss with an automatic card updater. When a card is reissued, the card network automatically updates the token. Your stored credential stays valid, the renewal processes, and the customer never knows anything happened.

Solidgate data shows that merchants adopting network tokenization see retention improvements of up to +7.5% as a direct result of token lifecycle management keeping card credentials valid across reissuance events.

MEGOGO, an OTT streaming platform operating across Eastern Europe and Central Asia, reduced subscription churn by 5% after implementing VTS/MDES tokenization alongside Account Updater.

→ Read the full .

One-click checkout unlocks upsell revenue

Once a network token is provisioned on a customer's first transaction, every subsequent purchase – upgrade, add-on, cross-sell – can complete in a single click with no data-entry requirements.

The contrast with a non-tokenized upsell flow is significant: without a stored token, a customer attempting a $20 add-on faces a full card-entry form with card number, expiry, CVV, billing address, and more. With a token, they see one button. That friction difference drives a measurable conversion gap. Solidgate merchants using tokenized one-click flows see upsell conversion improvements of up to +20%.

Combined LTV impact

Across acceptance improvement, retention, and upsell conversion, network tokenization drives up to +42.5% improvement in customer LTV for subscription businesses. That's not a security outcome. That's a growth outcome.

A smaller PCI DSS footprint and lower compliance costs

(Payment Card Industry Data Security Standard) requirements apply to every system that stores, processes, or transmits cardholder data. The broader the scope, the more complex and costly the audit.

When a business uses network tokenization, raw card data never touches its own infrastructure. What gets stored is a token – a non-sensitive substitute with no mathematical relationship to the original card number. That shift takes most of a merchant's internal systems out of scope for PCI DSS audits entirely, and the compliance burden moves to the tokenization service provider, which is already a Level 1 PCI-certified entity.

In practical terms, this means:

- Shorter self-assessment questionnaires (often qualifying for SAQ-A rather than the multi-week SAQ-D process)

- Fewer systems requiring quarterly vulnerability scans

- Less internal resource time devoted to annual certification cycles

For businesses without dedicated compliance teams, that reduction in scope is time and money saved.

International expansion without added payment complexity

Cross-border card at higher rates than domestic ones. Unfamiliar merchant profiles trigger issuer caution, and inconsistent card data creates processing errors. This has historically made international growth operationally heavier than it needs to be.

Network tokens reduce this friction at the infrastructure level. The issuer doesn't need to evaluate an unfamiliar merchant from scratch. The token and its associated cryptogram establish legitimacy within the payment chain.

Tokenization also simplifies compliance in regulated markets, reducing exposure under GDPR, the Indian tokenization mandate for recurring payments, and similar regional frameworks.

A business processing payments in three markets or thirty benefits from the same authorization lift and compliance simplification, without rebuilding payment infrastructure for each new territory.

A payment stack that works with what comes next

Payment technology keeps changing:

- Biometric authentication

- (where AI systems initiate purchases on behalf of consumers)

- Stablecoin settlement

- IoT-connected payment devices

Network tokenization provides the foundation for these flows. Mastercard's Agent Pay initiative, for example, uses tokenized credentials to allow AI agents to transact securely on behalf of users. The agentic token functions exactly like a standard network token at checkout, so merchants don't need new acceptance infrastructure.

If your token infrastructure is in place today, you're already compatible with the next generation of payment interactions. The investment extends forward.

Core insight: Network tokenization's commercial impact runs across six areas: checkout conversion, authorization rates, customer LTV, PCI DSS compliance scope, cross-border payment reliability, and compatibility with emerging payment technologies.

The business case for adopting network tokenization

These benefits add up to a quantifiable financial case. Three pillars frame it:

Revenue growth

Higher authorization rates translate directly into more revenue per billing cycle. Fewer failed renewals reduce involuntary churn, keeping more subscribers past the billing failure that would otherwise have ended the relationship. Frictionless one-click flows improve upsell and upgrade conversion rates on existing customers.

As a hypothetical: a 2% failed renewal rate on $500k MRR costs roughly $10k per billing cycle – $120k annually – before accounting for the downstream churn those failures trigger.

Cost savings

Network tokenization reduces two categories of operational cost.

First, PCI DSS compliance. When raw card data never enters your systems, the scope of your annual audit narrows significantly. There are fewer systems to certify, simpler assessment questionnaires, and less resource time devoted to annual certification cycles.

Second, failed payment recovery. Fewer declined charges mean fewer dunning cycles, fewer customer service contacts, and less permanently unrecovered revenue.

Risk mitigation

Because raw card data never enters your infrastructure, your exposure in a data breach is categorically lower – there's nothing to steal that carries value.

Tokenization also reduces operational risk. If a PSP shuts down or experiences extended downtime, acquirer-agnostic tokens can be rerouted to alternative acquirers without re-tokenization and without customer impact.

Core insight: The financial case for network tokenization rests on three pillars: revenue growth, operational cost savings, and risk reduction.

How Solidgate implements network tokenization

Most merchants who want network tokenization face the same barrier:

- Getting direct access to Visa and Mastercard's token services

- Standing up PCI-certified vault infrastructure to store and manage tokens

- Writing the integration logic to apply tokens correctly across every payment flow

Together, that's a significant engineering investment before a single authorization rate improvement shows up.

Solidgate – a payment orchestration platform connecting merchants to 100+ global acquirers – removes this barrier by holding direct Visa and Mastercard token service partnerships and managing the full token lifecycle on the merchant's behalf.

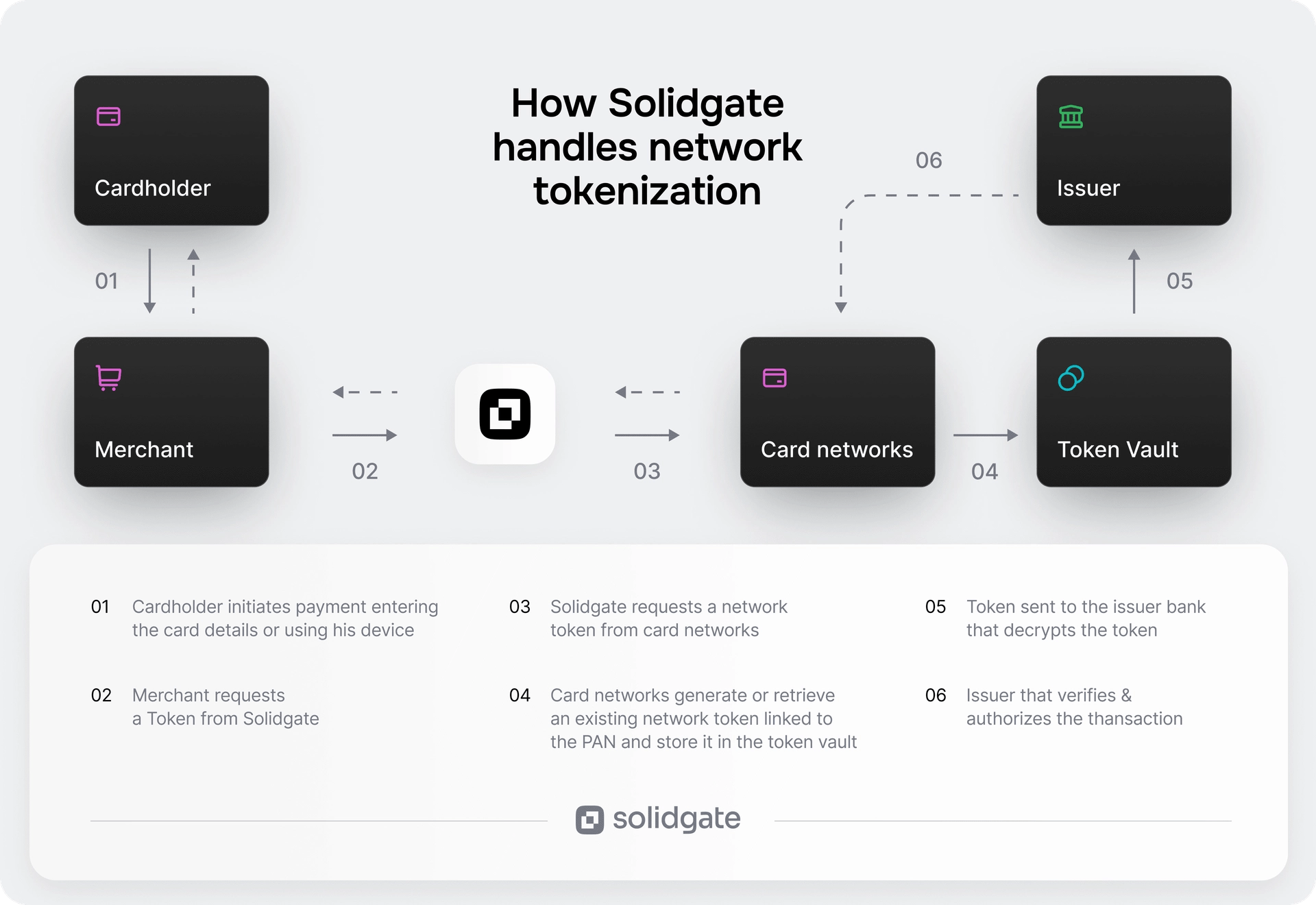

Scheme-issued token provisioning

On a customer's first transaction, Solidgate requests a network token directly from Visa or Mastercard. The card network generates a token tied to that specific card, merchant, and transaction context, then stores it in . From that point forward, the customer's raw primary account number (PAN) never travels through your system again.

Each subsequent charge uses that token, paired with a unique per-transaction cryptogram. Issuers recognize tokens issued by their own card networks and treat them with higher confidence than raw card data passed through a processor. That trust is what drives the +15% acceptance rate improvement across Solidgate's merchant base.

Automatic token lifecycle management

Cards get reissued constantly – through expiry, theft, proactive bank upgrades, or account changes. Each reissuance event is a potential failed renewal in a subscription business.

connects to Visa and Mastercard's card updater services. When a card is reissued, the token refreshes automatically and the next billing attempt fires against valid credentials. Your operations team doesn't touch it, and the customer never knows it happened.

Acquirer-agnostic token routing

PSP-level tokens are locked to the provider that issued them. Add a second acquirer for redundancy, a regional processor with better local authorization rates, or a backup for failover – and you're building a new stored credential base from scratch.

Because Solidgate stores tokens at the orchestration layer, they route to any of the without re-tokenization. If a processor experiences downtime, Solidgate cascades to the next acquirer using the same token. If a PSP exits a market or raises fees, you reroute without touching stored credentials.

The value of this architecture shows most clearly when something breaks. When one of Zeely's tier-2 acquirers shut down, all tokens were already preserved on the Solidgate side. The entire recurring payment tail transferred to new tier-1 acquirers – JPMorgan Chase, Adyen US, Checkout.com US – with near-zero revenue loss.

→ See the full .

One-click flows for renewals and upsells

Once a token is provisioned on the first transaction, every subsequent charge – monthly renewal, annual upgrade, add-on purchase – processes without asking the customer to re-enter anything.

For subscription businesses, this also extends to win-back flows. A lapsed subscriber returning to reactivate encounters no payment friction – the token is still valid, and the charge goes through on confirmation.

Core insight: Solidgate stores network tokens above your acquirers, not inside them. That's what makes them portable across processors, auto-updating on card reissuance, and intact through acquirer disruptions.

Beyond network tokenization

Most of the outcomes covered in this article don't come from tokenization alone. They come from tokenization working alongside smart routing and billing logic in the same platform. Routing decisions run on cleaner, more trusted credentials. Billing logic benefits from tokens that survive card reissuance and travel across acquirers without re-tokenization.

That's what Solidgate is built for. Beyond network tokenization, the platform covers , subscription billing, acquiring, antifraud, and chargeback management – across 100+ acquirers and payment methods, in one integration.

If you want to see how this works for your payment stack, .

Frequently asked questions

Network tokenization is the process by which a card network – Visa, Mastercard, or another scheme – replaces a customer's real card number (primary account number, or PAN) with a unique digital substitute called a network token. That token stands in for the PAN at every stage of the transaction. Because it's issued by the scheme itself, the customer's bank recognizes it natively, without friction.

Gateway tokenization – sometimes called PSP-level tokenization – stores your customer's card data with your payment provider and returns a token that works only within their ecosystem. Network tokenization operates at a different level: the token is issued directly by Visa or Mastercard, works across any processor connected to the card network, and updates automatically when a card is reissued. If you switch or add an acquirer, your stored credentials travel with you.

Visa and Mastercard are the two primary card networks with mature network tokenization programs – Visa Token Service (VTS) and Mastercard Digital Enablement Service (MDES). Both are built on the EMV Payment Tokenisation Specification, which ensures a network token behaves consistently across processors and acquirers globally.

Network tokens don't expire the way raw card numbers do. When the underlying card is reissued – due to expiry, theft, or a proactive bank upgrade – the card network updates the token automatically. The next billing attempt fires against valid credentials with no action required from the merchant or the customer.

Apple Pay and Google Pay use device-specific tokens to secure in-app and contactless payments. These are provisioned for a specific device and payment context. Network tokenization for recurring billing works differently: the token is provisioned at the merchant level, persists across billing cycles, and is designed specifically to handle subscription renewals, upsells, and card-on-file charges – not point-of-sale transactions.

Cross-border card payments fail at higher rates than domestic ones. Unfamiliar merchant profiles trigger issuer caution, and inconsistent card data creates processing errors. Network tokens reduce this friction: the issuer doesn't evaluate an unfamiliar merchant from scratch, because the token and its cryptogram establish legitimacy within the payment chain. Tokenization also reduces compliance exposure under frameworks like GDPR.

Yes, across two categories. First, PCI DSS (Payment Card Industry Data Security Standard) scope narrows when raw card data never enters your systems. Fewer systems require certification, audit questionnaires are shorter, and annual compliance cycles take less internal resource time. Second, fewer declined charges mean fewer dunning cycles, less customer service contact, and less permanently unrecovered revenue.

That depends on your integration path. Building direct connections to Visa Token Service and Mastercard Digital Enablement Service requires scheme partnerships, PCI-certified vault infrastructure, and integration logic across every payment flow – a significant engineering investment. Working through a like Solidgate that already holds those scheme partnerships removes most of that barrier. The token provisioning, lifecycle management, and acquirer-agnostic routing are handled at the platform level, so your team connects once and benefits from day one.