Many subscription businesses have a hole in their revenue funnel: off-the-charts fraud and chargeback levels. When you’ve invested so much in your core product, marketing, and sales techniques, this aspect of your business can seem like a nuisance—until it starts affecting your payment machine.

Around 2-3%—that’s the average rate of payment fraud in subscription services. In some cases, this number climbs to 4%—a staggering four times higher than the 0.9% threshold set by the card schemes. Of course, those numbers will vary depending on your industry and target markets, but the trend is there.

In 86% of cases, this is “friendly fraud,” when legitimate users forget to unsubscribe, fail to recognize the transaction or misunderstand the terms and conditions when signing up and requesting a chargeback. The remaining 14% involve intentional fraudulent payments that escape detection.

Having worked with hundreds of subscription companies, we know that very few have fraud teams that employ basic fraud management tools like Visa Compelling Evidence 3.0, 3D Secure 2.0, or fraud screening. Even fewer adhere to Visa and Mastercard scheme requirements for subscription merchants in their communication.

In the end, they pay a high price: low payment acceptance rates, growing chargeback rates, high transaction fees, fines, and even bans from card networks and payment systems. We’ve created this guide to explain why fraud is such a problem for your revenue and growth and give you actionable tips to change that.

Check if your derisk strategies meet industry standards — download our PDF Subscription Fraud and Chargeback Defense Checklist.

Table of Contents

How high subscription fraud & chargebacks rates cripple your payments

The level of fraud and chargebacks directly impacts your payment acceptance rate and processing cost. For subscription services, acceptable rates must always fall below 1% of total transactions. Anything higher leads to credit card schemes flagging you as a “high-risk business,” hurting your bottom line in multiple ways.

Placement into card monitoring programs

Visa and Mastercard monitor the number of chargebacks (disputes) your business incurs each month. If you go over the limit they consider acceptable, they place you in a monitoring program.

If it happens, you might end up paying monthly penalties and extra fees until you bring your dispute numbers back down to an acceptable level. How much? It depends on three things:

- The type of program

- How long you remain in the program

- How severely you exceed the thresholds

More on how much in fines you might end up paying in each case is in our Monitoring programs article.

Increased “Do not honor” and “Suspected Fraud” declines

Card-not-present transactions are inherently riskier, leading to higher decline rates—for every $1 in fraudulent online payments, $25 of genuine online payments are falsely declined.

Businesses flagged by Visa and Mastercard monitoring programs face even higher rates of “Do Not Honor” and “Suspected Fraud” declines. For subscription renewals, where both the cardholder and the card are not present, and the cardholder isn’t incentivized to retry the payment immediately, this always means an increase in involuntary churn and feasible annual recurring revenue losses.

1.5 to 3 times higher transaction fees

Being labeled as high-risk doesn’t just hurt acceptance rates—it also increases your costs. Card schemes, acquirers, and payment processors pass their financial risks onto merchants through higher transaction fees. Managing high-risk accounts is resource-intensive, requiring more fraud prevention measures, compliance reviews, and administrative oversight.

The exact fees depend on your industry, geography, transaction volume, and processor risk profile. On average, processing costs can rise 1.5 to 3 times higher, reaching between 4% and 10% per transaction.

The transactional fees will vary depending on your industry, location, transactional volume, and risk profile of the specific payment processor. On average, transaction processing can be 1.5 to 3 times more expensive, with fees falling between 4% and 10%.

Chargeback fees that reach up to $100 per dispute

Let’s say you run a subscription-based business charging $50 a month. With 10,000 subscribers, you’re pulling in $500,000 monthly.

Now, imagine being flagged as high-risk and placed in a chargeback monitoring program. Depending on your situation, chargeback fees range from $25 to $100. For this scenario, we’ll use $75 per chargeback.

Let’s assume your chargeback rate is 2.5%, which means 250 out of 10,000 transactions turn into chargebacks each month:

- You’re refunding 250 customers their $50 subscription, which costs you $12,500 right away.

- Then, you’re hit with the $75 chargeback fee for each of those 250 chargebacks, adding another $18,750 in fees.

In one month, you’re losing $31,250—just from chargebacks. That’s over $375,000 per year.

Account limitations or blocks on payment service providers

Major APMs like PayPal or Stripe don’t like high-risk merchants. Even businesses with fraud metrics under 1% but operating in high-risk industries face scrutiny when opening merchant accounts. This task will be an uphill battle for merchants whose risk metrics seriously exceed the 1-2% threshold—unless they can demonstrate their ability to fix those ratios first.

If you already process with these providers, heightened fraud numbers lead to various account limitations, suspensions, or complete termination if your rates are really off and not going down. Reactivating your account might take weeks or months of back-and-forth with the processor’s support, compliance checks, providing additional documents, etc. These mean weeks or months of zero revenue on a specific payment platform, with a potential hold of funds for up to 180 days during disputes.

Find more strategies to lower your fraud risks in PayPal.

Solving high subscription fraud: Full checklist

To lower your fraud and chargeback metrics, focus on three key areas:

- Antifraud & security measures

- Transparent user communication

- Chargeback minimization strategies

Address these, and your fraud rates will drop immediately. The checklist below shows how.

Must have antifraud & security measures

The tools below serve as a gate, detecting subscription fraud of all types from the get-go.

Fraud prevention

- Choose your target markets carefully and pay close attention to your traffic sources—this way, you avoid an influx of fraudulent transactions from high-risk locations.

- If you target locations with a high level of fraud, configure your systems to flag high-risk locations for extra verification.

- Use velocity checks to flag suspicious activity, e.g., repeated transaction attempts within a short period, to avoid unauthorized payments and account takeovers.

- Limit bulk purchases of digital items, control the daily transaction volume per cardholder, and place restrictions on loyalty rewards or memberships to deter abuse.

Fraud detection

- Require CVV code to ensure the customer possesses the card.

- Use the Address Verification System (AVS) to validate the billing address listed in the transaction against the address registered with the issuing bank.

- Use 3D Secure 2.0 or later to authenticate customer identities.

Customer monitoring

- Monitor customer purchase histories for suspicious activity.

- Partner with your payment processor to maintain a list of blocked and approved customers.

Data security and compliance

- Avoid unnecessarily storing payment data.

- Use secure servers, network tokenization, and end-to-end encryption (E2EE).

- Ensure your business adheres to PCI DSS standards.

Transparent user communication & cancellation

Obscure user communication leads to misunderstandings and causes legitimate customers to file for chargebacks at increased rates. To avoid this fate and comply with Visa and Mastercard regulations, you must address every step of customer communication.

Subscription terms

Per the rules of Visa and Mastercard, when a user signs up for your services and visits the checkout page, you must disclose all the information about what the subscription entails in a clear, straightforward, and obvious way. This information includes things like:

- Services rendered

- The amount the customer is going to pay (for example, “You will be billed USD 9.95 per month until you cancel the subscription”)

- Billing frequency

- Cancellation process

If you use a negative option billing model, you must also disclose the terms of free trials, including any initial charges, the length of the trial period, and the price and frequency of the subsequent subscription (for example, You will be billed USD 2.99 today for a 30-day trial. Once the trial ends, you will be billed USD 19.99 each month after that until you cancel.”)

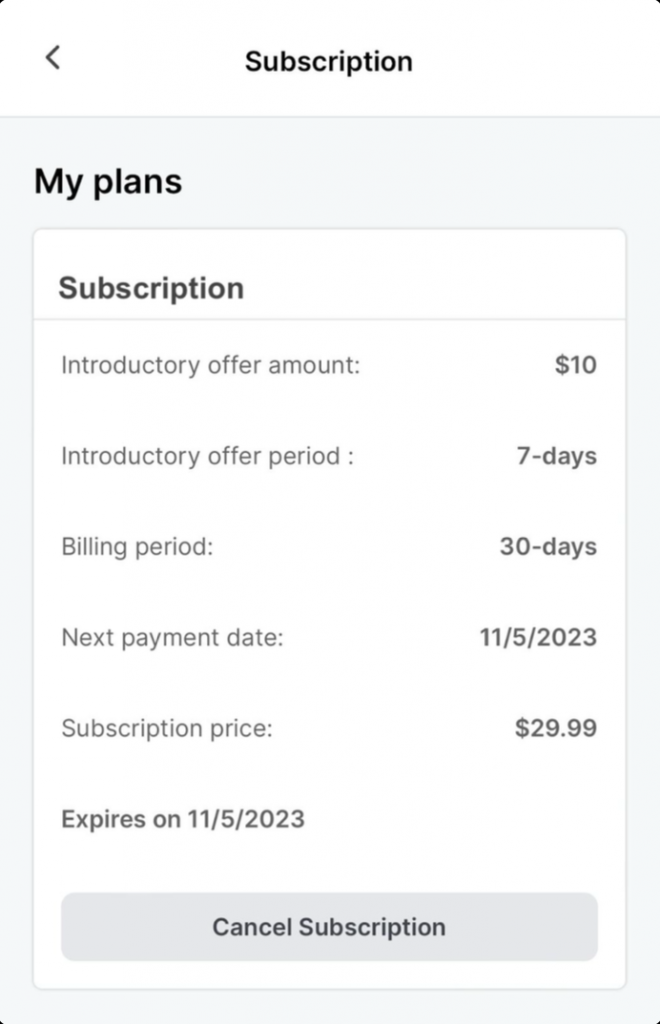

We suggest adding the following disclaimer under the Pay/Accept/Continue/Proceed to checkout button:

![A screenshot of a subscription disclaimer saying: “You are enrolling in a monthly/annual/weekly subscription to [name of the website] service. You agree to be billed [full price of the subscription] per month/week/year until you cancel the subscription. Payments will be charged from the card specified above/below/here. To cancel, please visit our Cancellation Policy+link / write to [support email] / OR You can cancel your subscription in your account/profile settings.”](https://solidgate.com/wp-content/uploads/2025/01/Disclaimer-1024x479.png)

Post-sale communication

Keeping customers in the loop at every step is paramount.

- Send a receipt after the first and each subsequent charge with the following details: your business name, location, transaction amount, date, services purchased, card details, and links to your Cancellation and Refund Policy.

- Make sure your bank statements and emails are clear and include your company name, support email, payment details, and simple instructions to cancel.

- Proactively update order status, flag issues immediately, and make sure customers get what they paid for.

- Keep your billing descriptors customer-friendly by including your domain, business name, or support info. Keep them 5-22 characters and avoid special symbols.

- If you’re using a negative billing option model, you must send notification reminders at least three days and no more than seven days before the free trial period ends.

Cancellation procedure

The merchants must:

- Ensure that canceling the subscription is as easy as subscribing. Your users may cancel via a separate cancellation button on the website, a button in their subscription account on the website, or a support email.

- Inform users of the Cancellation and Refund Policy and collect their acceptance before they get to the checkout page.

- Include information on how to cancel the subscription and receive a refund in each transaction receipt and notification on upcoming charges.

Chargeback prevention

- Sign up for programs like Mastercard Consumer Clarity and Visa Order Insight. These tools give you detailed transaction information in near real-time, cutting down on billing confusion.

- Leverage pre-chargeback alerts such as CDRN and Mastercard’s Ethoca Issuers notices of intended chargebacks, allowing you to deflect the dispute or refund the customer before the chargeback is filed.

- Use automatic dispute resolution, like Visa’s RDR, which uses transaction amounts and other thresholds to quickly resolve disputes without the merchant’s involvement.

- Grant credits and cancellations as soon as the customer asks.

Case in point: How Zeely, a SaaS company, lowered its fraud rate by 3X

Fraud and chargebacks aren’t just an annoying cost of doing business; they’re a silent anchor dragging down growth. For Zeely, an AI-powered platform helping businesses sell online, this anchor nearly stopped them in their tracks.

Zeely’s challenges were textbook for subscription businesses. Their fraud and chargeback rates had climbed to 3%, three times higher than what Visa and Mastercard tolerate. This wasn’t just a compliance issue—it was a growth killer: payment acceptance rates were dropping, transactions were being declined frequently, and PayPal was no longer an option. Plus, they relied on a single acquiring bank, and every payment decline hit twice as hard.

With an integrated approach to fraud prevention and dispute management, Solidgate quickly turned things around. By leveraging Solidgate’s chargeback management & antifraud tools, Zeely’s fraud rates dropped from 3% to 1%, with over 95% of disputes flagged and prevented before they became a problem. For the first time, Zeely could accept PayPal payments—a game-changer for their audience.

Solidgate also extended the authorization period, catching early chargebacks before they settled. This simple adjustment gave Zeely’s customers more time to resolve issues directly with the merchant, cutting disputes at the source.

As a result, Zeely’s payment acceptance rate jumped by 15%, recurring payments stabilized, and they had the freedom to scale globally without fraud dragging them down.

High fraud isn’t just a nuisance—it’s bottom-line killers

If you plan to scale globally without bleeding money, taking a proactive and comprehensive approach to lowering your risk metrics is non-negotiable. The sooner you get on board with this idea, the sooner you’ll see the results.