Imagine a grocery store checkout. Out of 10 customers paying with cards, it is unlikely that any payment will fail if their accounts are funded.

Buying online is a different story. Online payments are declined much more often for various reasons: the card has expired, or one of the parties in the payment ecosystem detected fraudulent activity. And the effect is much more damaging.

When a $100 monthly subscription payment failed, it might seem like just one lost transaction. But the true cost is much higher. That customer wasn’t planning to cancel. They were happy with the service and ready to stick around for another 12 months. But one payment failure silently ended the relationship, cutting off a steady stream of revenue.

$100 per month × 12 months = $1,200 in lost revenue. All because of one payment that failed.

As a team that has developed a global payment infrastructure, even with our advancements, we find achieving a 100% payment success rate challenging. Factors like product type, industry, or quality of your traffic all affect how many online payments will get through.

The good news is that it’s well within your control to drastically reduce payment failed instances and save more revenue. In this guide, we’ll lean into years of experience optimizing payment performance for online businesses to explain why online payments fail and arm you with solutions to prevent these failures.

Table of Contents

Understanding the difference between payment failure and decline

Payment failure and payment decline/credit card decline are used interchangeably in the payment world, but there is a slight difference. Understanding which one you got is key to solving the problem when an online payment fails.

A payment failure is a broader term that covers all unsuccessful transactions, including declines, as well as issues caused by technical glitches, connectivity problems, or errors in processing.

On the other hand, a payment decline is a specific type of failed payment where the card issuer rejects (declines) the transaction because of insufficient funds, expired cards, or fraud prevention measures.

Long-term consequences of failed payments

When a payment fails, it isn’t just a hiccup—it’s a costly problem for online businesses. The impact of payment failure extends beyond the immediate loss of revenue or the frustration it causes your customers; its impact ripples further, affecting your bottom line, operational efficiency, and customer loyalty.

Take involuntary churn as an example: our client data shows that 1 in 3 users cancel their subscriptions because of payment or billing frustrations. This means customers aren’t leaving because they don’t love your product—they’re leaving because their payment couldn’t go through.

Beyond churn, reasons for payment failure also drive up operational complexity. For every failed payment, your team may need to manually intervene, chase customers for updated details, or handle customer support inquiries—all of which cost time and money.

The takeaway is clear: payment failures don’t just hurt in the moment—they create a domino effect that impacts revenue, loyalty, and operational efficiency.

Two types of payment declines: Soft vs. Hard

All credit card declines fall under one of two categories: soft vs hard decline. The category of declines determines whether you should retry the payment or not when an online payment fails.

Soft decline indicates an issue with a transaction that might be fixable. Maybe the customer’s card doesn’t have enough funds at the moment, or the issuer flagged the transaction as potentially fraudulent, or something as simple as a technical hiccup or a spotty connection. Sometimes, adding extra details—like confirming the payment is legitimate—can save the payment.

On the other hand, a hard decline is a full stop, which means the payment can’t move forward, no matter how many times you retry. Think of situations where a card has expired, the account is frozen, or the payment details don’t check out. In these cases, it’s better to ask the customer to use a different card or payment method.

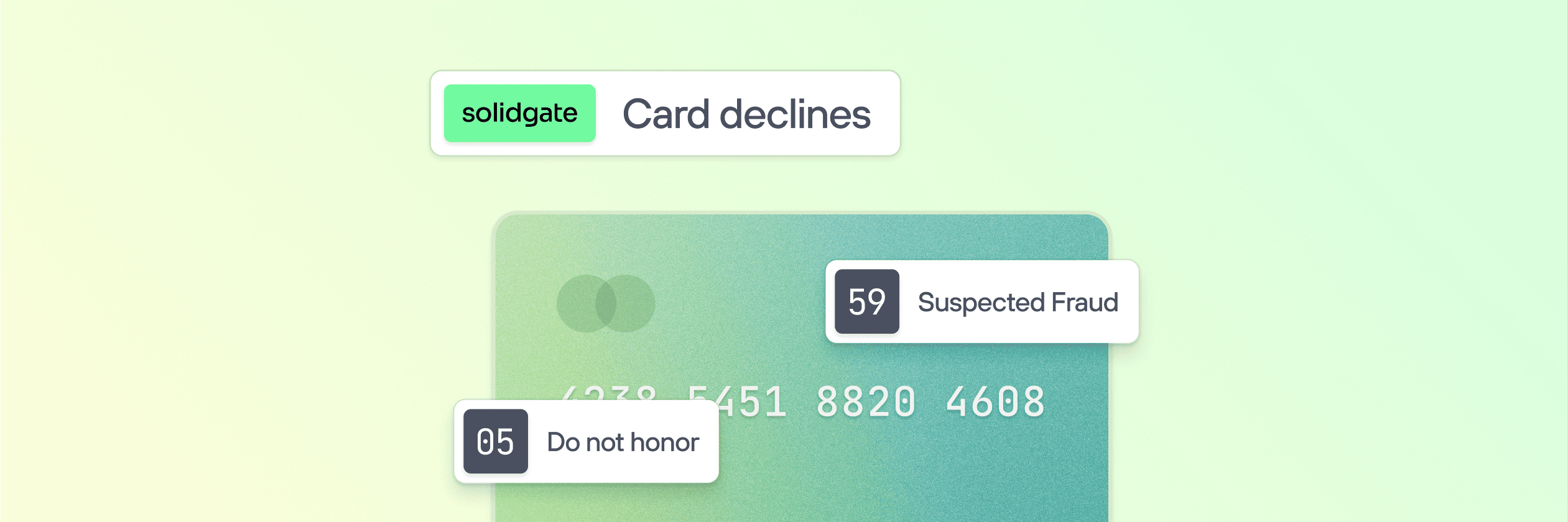

Most common credit card decline codes

These are the error codes you are most likely to see on your transactions dashboard or API responses:

- Code 05 – Do not honor: The issuing bank has chosen not to approve the transaction, but the reason is unclear. This response often signals that the cardholder should contact their bank to verify or resolve potential issues.

- Code 14 – Incorrect card number: This error pops up when the card number entered doesn’t match the actual details on file with the issuer, often due to a simple typo.

- Code 41 – Lost card, pick up: The card has been flagged as lost by the cardholder, so all transactions are automatically blocked.

- Code 43 – Stolen card, pick up: The cardholder has reported the card as stolen, which triggers an immediate denial of any transactions.

- Code 51 – Insufficient funds: There’s not enough money in the account to complete the purchase.

- Code 54 – Expired card: The card is past its expiration date, making it invalid for any transactions.

- Code 63 – Wrong CVC: The three-digit security code on the back of the card (or four digits on the front for American Express) doesn’t match what the issuer has on file.

- Code 65 – Credit limit exceeded: The cardholder has hit their spending cap for the billing cycle. They’ll need to pay down their balance or use a different payment method to move forward.

Key reasons for payment failures & and how to fix them

Understanding why online payments fail allows you to address the core issues. The most common payment failures can be broadly classified into the following three categories:

- Issuer-related

- Technology-related

- Customer-related

Let’s see what they are and how to work with them.

Issuer-Related Declines

These declines are tied to decisions made by the cardholder’s bank. This category often presents the greatest opportunity for revenue recovery when payment failed.

Card is blocked / Internet spending limits

Many digital-only banks offer customizable internet spending limits, which can lead to payment declines with the reason code 3.01 Card is blocked. For example, a user might successfully make several purchases online, but their payment for a mobile app subscription fails. In this case, this occurs because their card has reached the preset limit.

Solution: Instant notifications

Set up instant notifications that encourage customers to contact their bank’s support to remove the limit and suggest trying to make the payment again. Many banks have dynamic rules based on a scoring system, and repeated attempts can increase the likelihood of successful transactions when an online payment failed.

Local card brands

In some countries, many cards are local card brands that can only process payments through local banks. For example, in Brazil, over 60% of cards are ELO, HiperCard, and AURA. European, American, and even Moldovan banks know nothing about these card brands and cannot process them, leading to payment failure.

Solution: APMs, geo-focused checkout UX

If you target regions where local card brands dominate over international ones, not offering customers locally preferred APMs can seriously damage your conversions when payments fail.

To illustrate, in regions like Poland or Brazil, over half of the population prefers paying online with local APMs like BLIK and PIX. Local customers expect to see these APMs at the checkout.

If the option isn’t there, they might either abandon the checkout or try paying with their local card brand, which is incompatible with your acquiring bank. Tailoring your checkout page to the target region helps you save conversions, secure sales, and increase loyalty in the target region.

Unverified customer

It’s quite common for authentication checks to mistakenly block genuine payments. In regions like Europe, the introduction of Strong Customer Authentication (SCA) has tightened the screws on compliance, pushing merchants to take a more cautious stance on customer verification. The result: more declines of genuine transactions and higher payment failure rates.

Solution: 3DS 2.0, 3RI authentication

The newest 3D Secure 2.0 (3DS2) uses data like the customer’s device, location, and buying patterns to verify transactions without unnecessary steps.

For example, if a regular customer makes a usual purchase, 3DS2 can approve it automatically. If something seems off, it asks for extra confirmation like one-time passwords (OTP), fingerprints, or QR codes without making the process too cumbersome.

For recurring payments or card-on-file purchases, we suggest using 3RI or merchant-initiated authentication. 3RI allows merchants to initiate authentication on behalf of their customers, so all the recurring payments can be authenticated in the background without complicating the payment experience. Some PSPs, including Solidgate, support 3RI within the 3D Secure solutions, making it easy to implement secure yet efficient recurring payments.

Technology-related declines: Technical fixes

These declines stem from system issues or payment infrastructure limitations that can disrupt transaction processing and cause online payment failure scenarios.

Cross-border transactions

In cross-border scenarios, where the issuing bank, merchant, and acquiring bank are in different countries, payment processing faces more friction due to exchange rate losses, varied regulations, and fraud rules. Naturally, all these extra factors congest the payment route and make declines much more frequent.

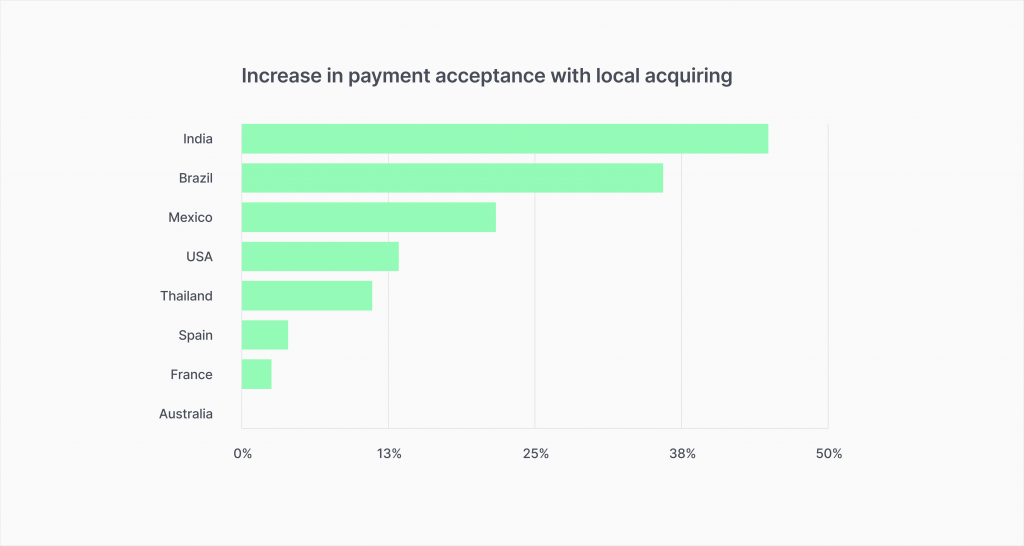

Solution: Local acquiring, intelligent payment routing

Local acquiring—when the issuing bank, merchant, and acquiring bank are located in one country—regularly results in higher payment success rates due to minimal exchange rate losses, lenient fraud prevention rules, and a unified regulatory landscape.

Of course, opening a business bank account in every country you operate in is far from simple. Governments often require businesses to establish legal entities locally, which can be a time-consuming and costly process. For many merchants, the better option is to work with a platform that handles the heavy lifting—compliance, regulations, and all the complexities of cross-border payments to prevent payment failure instances.

A simpler solution is to leverage intelligent payment routing. Our merchants using intelligent routing have reported a 5-10% increase in approval rates. It operates much like optimizing logistics in a complex supply chain.

Traditionally, transactions flow through predefined banking routes based on assigned identifiers, like BINs or network codes. But these routes can hit obstacles, like system incompatibilities, regional regulations, or fraud filters that block the payment, causing payment failure.

Intelligent routing addresses this by finding the optimal path for a transaction. If your payment platform is connected to a broader network of acquiring banks, it can analyze different routes and pick the one most likely to go through. If the first try is declined, it automatically moves to the next best option until the transaction is successful.

Fraud triggers

Card-not-present transactions are inherently riskier than on-site payments and trigger fraud alerts much more often, leading to reasons for payment failure. Issuing banks carry all the risk and so tend to be over-cautious — for every $1 in fraudulent online payments, around $25 of genuine online payments are falsely declined.

If you also operate in a high-risk industry or have been placed into a scheme monitoring program, losing sales due to low payment acceptance becomes your norm.

Solution: Limiting traffic from high-risk locations, antifraud tools

Certain countries and Tier 3 regions may have higher levels of fraud. If statistics indicate that certain countries are responsible for a lot of fraudulent transactions (e.g., some countries in Africa, Latin America, or Southeast Asia), completely blocking—or closely monitoring—traffic from these regions would be a smart move to reduce payment failures.

But blocking traffic alone isn’t enough. Fraud prevention works best when supported by antifraud tools:

- Fraud screening tools like machine learning algorithms and detailed analytics help identify suspicious activity;

- Behavioral analytics can identify suspicious user behavior;

- Compiling “black” lists of fraudulent transaction elements (e.g., names, email and IP addresses, device IDs, customer identification numbers, and telephone numbers) allows blocking customers who pose a threat;

- Setting customized risk rules helps tailor transaction review thresholds to the specifics of your business, focusing on the number and value of approvals.

Customer-Related Declines: Practical Solutions

These declines are directly related to the customer or their payment method and represent common reasons why payment failed.

Insufficient funds

This reason is straightforward: the customer lacks available funds to transfer. Since sending them money to pay you defeats the purpose, let’s see how you can incentivize them to try one more time when an online payment failed.

Solution: Notifications, alternative payment options (APMs), scheduled retries

Instant communication is key. Right after receiving a decline, send a friendly email, SMS, or in-app notification suggesting that the customer use a different card, add funds to the current one, or use a different payment method altogether. This will catch them in the buying mode, incentivizing them to retry the transaction.

Enabling customers to switch to another payment method is critical in this case: Buy Now Pay Later (BNPL), digital wallets like PayPal, or local payment methods offer customers various options to retry the payment when they’ve experienced a payment failure.

Scheduling automatic retries is another great solution. You can schedule retries specifically for insufficient funds for a time when your customer is most likely to have enough money to cover the payment (at the start or the end of the month, for example).

Canceled or expired card

If you operate under a recurring business model, declines due to expired cards become a recurring problem and a top reason for payment failure. Users have an average of 3-4 active subscriptions and rarely pay attention to updating their cards, leaving the handling of their payments to the merchants. This leads to billing problems, potentially decreasing subscription lifetime value (LTV).

Solution: Network tokenization, account updater

The VTS/MDES Tokenization technology, integral to wallets like Apple Pay and Google Pay, removes the need for you to remind users to update their card details. It does so by replacing a card’s primary account number (PAN) with a secure, unique token that is specific to the merchant, device, or use case. If the card details (like the expiration date or PAN) change, the network automatically updates the token to reflect the new details.

Account Updater is another must-have for subscription businesses. It automatically updates subscription payment details when a card is reissued or expires, ensuring uninterrupted billing and preventing online payment failures.

Incorrect payment information

Sometimes, your customers enter payment details that don’t match what their bank has on file, causing payment failures. Mistakes in the billing address are the most common. When the address doesn’t match the bank’s records, the issuing bank flags the issue and lets you know.

From there, it’s your call to either approve the transaction or play it safe and decline. In many cases, you might choose to go ahead with the payment, especially if the mismatch is minor, like a formatting issue, or the customer seems low-risk.

Solution: Address Verification Service (AVS)

To avoid unnecessary declines or fraud, you can use Address Verification Service (AVS). AVS is a tool from major card networks like Mastercard, Visa, Discover, and American Express that helps you verify your customer’s billing address during card-not-present transactions. Keep in mind, though, that AVS works only in certain regions like the US, Canada, and the UK.

Here’s how it works: AVS compares the numeric parts of the address your customer entered (like the street number or zip code) with the address their bank has on file. The bank then sends you a response code that shows how well the addresses match:

- Full Match: Everything matches perfectly.

- Partial Match: Some parts match, like the zip code, but not others.

- No Match: The address doesn’t align with the bank’s data.

- Unavailable: The bank doesn’t have address info, or the card is international and doesn’t support AVS checks.

You can use these results to decide your next move: approve the payment, block it, or ask for more verification to prevent payment failure issues.

Note: While AVS is a great tool, it’s not foolproof. Not every mismatch is fraud, and not every match guarantees safety. For best results, combine AVS with other fraud prevention strategies, such as 3D Secure or behavioral analytics.

Final thoughts

Payment failures are an inevitable part of the online payment ecosystem, but they’re far from unfixable. Every failed transaction is an opportunity to optimize your payment infrastructure and improve customer experience. Success begins with understanding the root causes of why online payments fail through analyzing your decline data and identifying patterns.

- Work closely with issuing banks to address declines;

- Implement advanced tools like intelligent routing and fraud prevention systems;

- Offer solutions like alternative payment methods, network tokenization, and account updater.

With strategic planning and the right technology, you can transform payment failures from a revenue drain into an opportunity for business growth.