Alternative payment methods: A complete 2026 guide

Payments 101

Updated 26 Jun 2026

13 min

Andrii Stoikov

Head of Support, Integration, Billing Operations, Solidgate

This guide maps which alternative payment methods dominate in which markets – and how to add them without a separate engineering sprint per country.

In most of the world's fastest-growing e-commerce markets, the majority of online transactions never touch a traditional card network. By 2028, alternative payment methods are projected to account for 58% of global e-commerce ().

APMs are no longer the alternative. When a Brazilian customer can't pay with PIX, a Dutch shopper finds no iDEAL, an Indian user expects UPI – they don't call support. They leave.

For any merchant with global ambitions, the right APMs open markets and determine whether you convert them.

This guide covers what APMs are, how each type works, which ones dominate in which markets, and how to add them without rebuilding your checkout from scratch.

TL;DR

- APMs are any non-cash, non-traditional card payment – digital wallets, real-time bank transfers, BNPL, direct debit, mobile money networks, and more.

- The right APMs vary sharply by region.

- Adding APMs increases checkout conversion, reduces card decline rates, and opens markets that card-only checkout can't reach.

- A single orchestration integration connects multiple APMs, handles localization, and keeps reconciliation in one place.

What are alternative payment methods?

Alternative payment methods (APMs) are any payment mechanism that operates outside traditional international card networks (Visa, Mastercard, and Amex). They span a wide range: from digital wallets and instant bank transfers to cash-based vouchers like Boleto and OXXO, which let consumers pay online using physical cash at retail locations.

What unites them isn't the technology – it's that they're built around how consumers in specific markets actually want to pay.

Types of alternative payment methods

Digital wallets

store payment credentials – cards, bank accounts, or prepaid balances – and let users pay without entering card details at checkout. Unlike mobile wallets, digital wallets hold an actual balance or maintain a direct connection to a bank account or funding source. The wallet relationship sits with the provider, not the card network.

For subscription businesses and e-commerce, digital wallets improve checkout conversion by eliminating manual card entry. They also support recurring payments, making them useful beyond one-time transactions.

In markets like China, India, Brazil, and Nigeria, digital wallets transfers account for around 30% of global point-of-sale volume, according to .

Examples: PayPal, Alipay, WeChat Pay, CashApp, Mercado Pago

Typical use case: Markets where wallet ecosystems dominate (China, LATAM), subscription sign-up flows, peer-to-peer transfers that flow into merchant purchases

Mobile wallets

Mobile wallets – sometimes called pass-through wallets – store a tokenized version of an existing card or bank account and authenticate payment via device biometrics. The card network still processes the transaction; the wallet just removes the friction of entering card details.

Examples: Apple Pay, Google Pay, Samsung Pay

Typical use case: Mobile checkout, in-app purchases, one-click upsells where reducing steps drives conversion

Direct debit

Direct debit lets a merchant pull payments from a customer's bank account on a recurring schedule, with prior authorization. It's the foundation of the subscription economy in Europe and Australia – used by gyms, utilities, SaaS platforms, and streaming services billing monthly or annually.

For subscription businesses, the structural advantage of direct debit is durability: once a customer sets up a mandate, it runs until they cancel. No card expiry, no token management, no failed renewals from a card replacement.

Direct debit has trade-offs, though. Mandates can be disputed, and settlement takes one to three business days – there's no real-time confirmation that a payment cleared.

Examples: SEPA Direct Debit (Europe), BACS Direct Debit (UK), BECS Direct Debit (Australia)

Typical use case: Subscription billing, recurring utility payments, instalment plans

Open banking / Pay by bank

Open banking-powered transfers are the evolution of direct debit. Direct debit is a pull mechanism – the merchant requests the funds. Open banking is a push payment: the customer authorizes a transfer from their own bank account in real time.

This architectural difference fixes the core weaknesses of direct debit. Settlement is instant rather than delayed by one to three days. Authorization happens at the bank level, not through a signed mandate. There's no disputed charge to reverse after the fact.

Traditional bank transfers (SEPA credit transfer, SWIFT) remain common for high-value or B2B transactions, where the payer is known and delayed settlement is acceptable. Open banking transfers – enabled by frameworks like PSD2 in Europe – are built for consumer e-commerce, where instant confirmation matters.

For merchants, both approaches share the same cost advantage: no interchange fees, no card network markup.

Examples: iDEAL (Netherlands), Przelewy24 (Poland), SEPA transfers (Europe), Wero (Germany, France, Belgium), Bizum (Spain), Open Banking (UK and EU)

Typical use case: High-value purchases, markets with low card penetration, merchants optimizing for processing cost

Buy now, pay later (BNPL)

(BNPL) lets customers split a purchase into installments – either interest-free over a short period or with financing over a longer term. The merchant receives the full payment upfront from the BNPL provider; the provider collects from the consumer.

increases average order value and conversion, particularly for higher-priced goods and consumers who are credit-constrained. Regulatory scrutiny has increased in several markets, but adoption continues to grow, especially among younger demographics in Europe, the US, and Australia.

Examples: Klarna, Affirm, PayPal Pay Later

Typical use case: Fashion, electronics, home goods – any category where price is a checkout barrier

Real-time payments

Real-time payment networks are government-built rails that move money between bank accounts in seconds, 24/7, via mobile apps using QR codes, phone numbers, or account IDs. In their home markets, these aren't alternatives to the dominant payment method – they are the dominant payment method.

UPI accounts for 85% of India's digital payments and nearly 49% of global real-time payment volume (). Brazil's PIX 93% of Brazil's adult population – over 170 million consumers – including 60 million who don't own a credit card.

Examples: PIX (Brazil), UPI (India), PayNow (Singapore), PromptPay (Thailand)

Typical use case: Merchants entering high-growth markets where card penetration is low. Growing in subscription contexts as real-time networks expand recurring payment support.

Prepaid cards and vouchers

Prepaid cards are loaded with a fixed amount and used like debit cards – without requiring a bank account. Prepaid vouchers generate a code redeemable at checkout, sold at retail locations. Both serve unbanked and underbanked populations, and remain popular for gift purchases.

Their structural advantage: no fraud risk beyond the loaded amount, no chargebacks, and no banking friction for the consumer.

Examples: Paysafecard (Europe), OXXO (Mexico), Boleto Bancário (Brazil), Neosurf

Typical use case: Digital goods, markets with low bank account penetration, gift-giving

Carrier billing

Carrier billing lets customers charge purchases to their mobile phone bill or deduct from prepaid credit – no card or bank account required. Authentication is automatic through the mobile network, making it low-friction for low-value digital purchases.

It's particularly relevant in markets where traditional financial infrastructure is limited, and among demographics (typically younger users) who don't hold credit cards.

Examples: Boku – operating across major telecoms including Vodafone, Tele2, and regional operators globally

Typical use case: Digital content subscriptions, app purchases in emerging markets

Cryptocurrency payments

Crypto payments let customers pay using decentralized digital currencies. Acceptance remains niche for most e-commerce merchants – volatility and settlement complexity are real constraints. Stablecoin payments (pegged to fiat currencies like the US dollar) are growing in B2B and cross-border contexts where traditional settlement is slow or expensive.

Examples: Bitcoin, Ethereum, USDC (stablecoin)

Typical use case: Cross-border B2B transactions, digital goods platforms, and merchants catering to crypto-native audiences

Core insight: With so many options available, most customers have settled on a preferred way to pay – and a checkout that doesn't offer it tends to lose the sale before it starts.

History of alternative payment methods

APMs trace back to the mid-1990s, when the internet first made remote payment possible at scale. PayPal launched in 1998 as one of the first alternative ; Alipay followed in 2003, building the digital payments infrastructure that would underpin China's e-commerce growth for the next two decades. The 2010s brought mobile wallets – Apple Pay in 2014, Google Pay in 2015 – and the BNPL wave driven by Klarna and Afterpay.

Regulatory frameworks accelerated the next phase. The European Union's opened bank APIs to third-party providers, creating the infrastructure for open banking-powered instant bank transfers. Meanwhile, central banks in Brazil, India, and Singapore launched government-backed real-time payment systems that rapidly displaced card networks as the primary payment method in their markets.

The most significant shift of the past five years has been the emergence of these state-backed networks. PIX, UPI, and PayNow aren't alternatives to card infrastructure – in their home markets, they've replaced it as the default. What "alternative" means is changing.

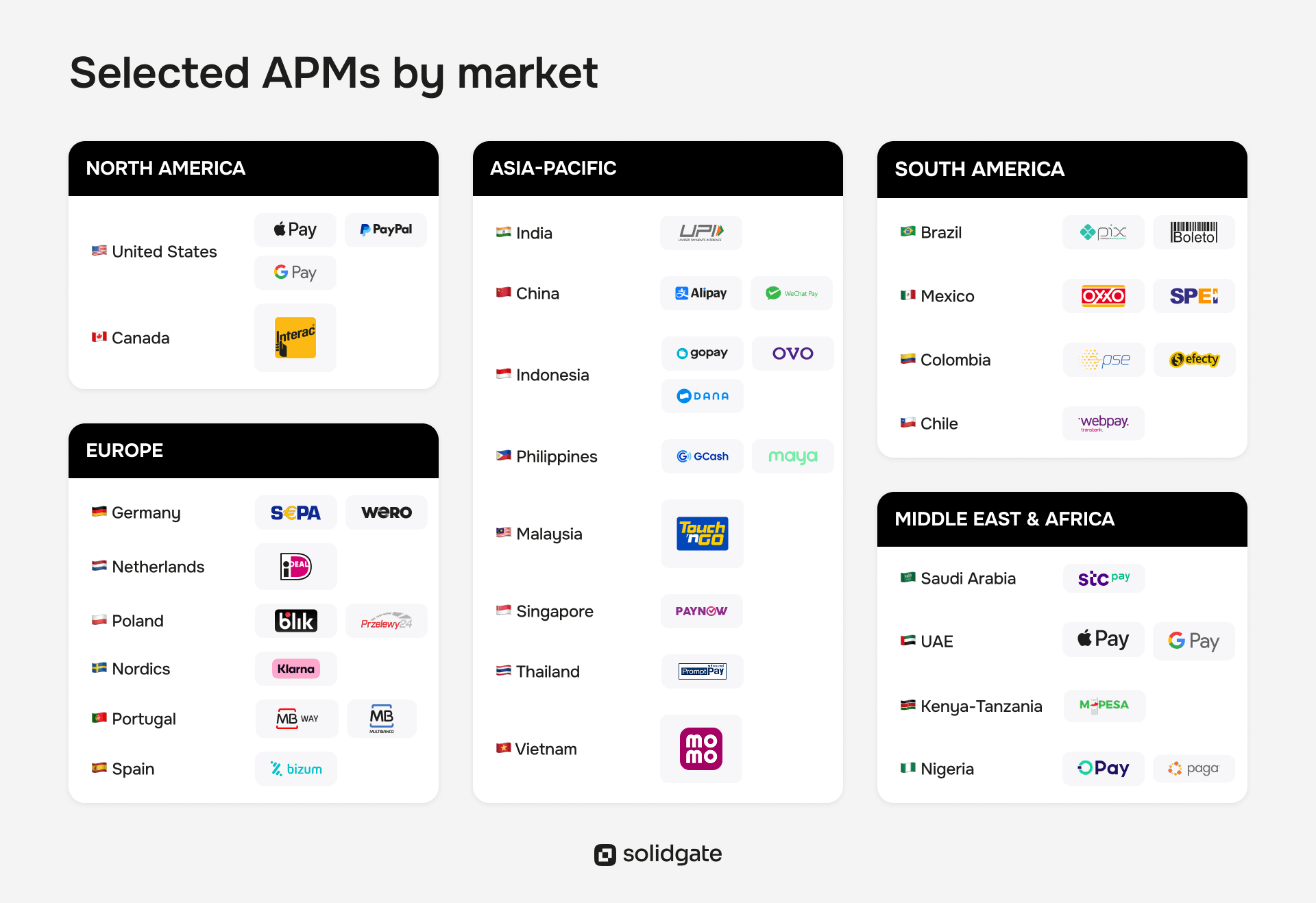

Alternative payment methods by region

No single APM works everywhere. The method that converts in Poland fails in Mexico, and what's default in India doesn't exist in Germany. Here's the practical breakdown by market.

Disclaimer: This overview reflects a selection of widely-used alternative payment methods and is not intended to be exhaustive. The third-party logos and brand names displayed in this image are the property of their respective owners and are used for informational purposes only. Solidgate is not affiliated with or endorsed by any of the brands depicted unless expressly stated otherwise.

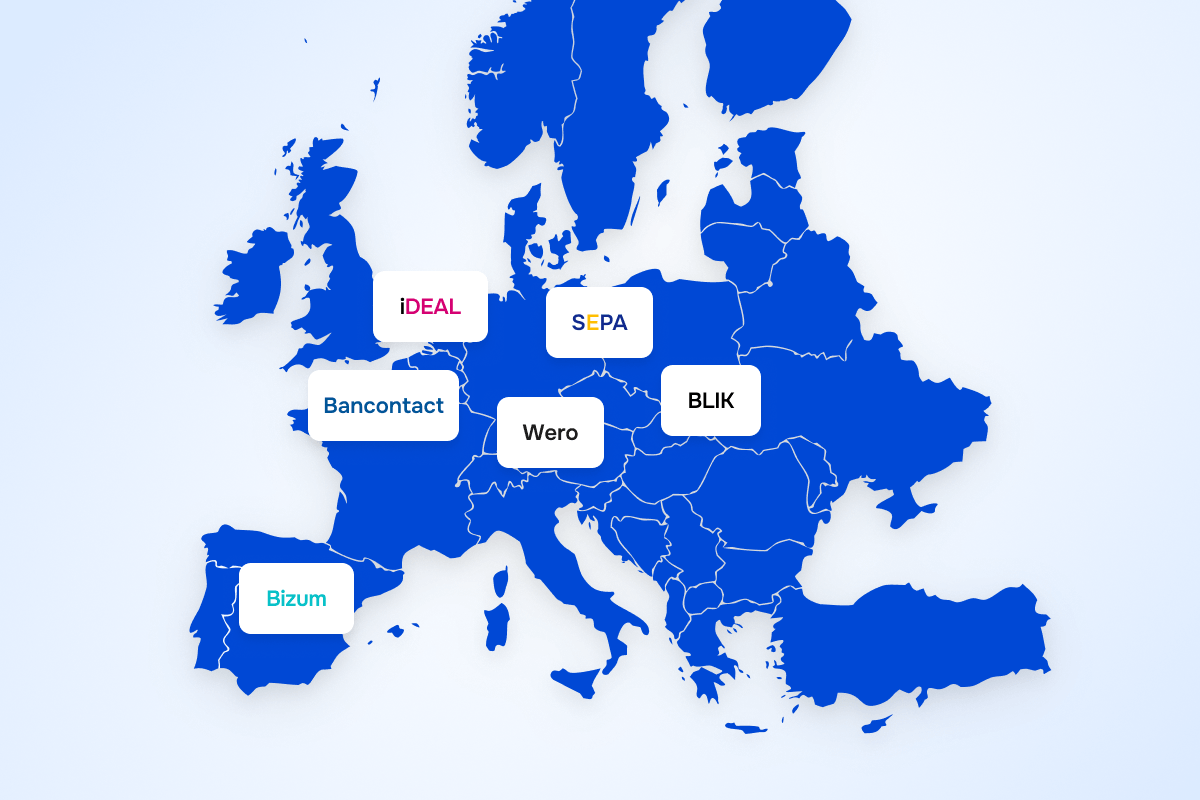

Europe

Europe has the most fragmented APM landscape of any major region. Card usage is high in the UK and France, but domestic alternatives dominate in several large markets.

For a full breakdown, see our guide.

Key APMs by country:

- Germany: SEPA bank transfers are the default for higher-value e-commerce. shut down in late 2024 – volume has consolidated toward SEPA and open banking providers. Cards are less dominant in Germany than in most of Western Europe; trust in bank-based transfers runs higher.

- Netherlands: iDEAL accounts for the majority of online transactions. Merchants selling to Dutch consumers must support iDEAL.

- Poland: BLIK covers the majority of Polish e-commerce. Przelewy24 handles most of the remainder.

- Nordics: Klarna dominates in Sweden, Norway, and Finland – as both a BNPL option and a general checkout brand.

- Portugal: MB Way and Multibanco are the dominant methods for domestic transactions.

- Spain: Bizum is growing rapidly as a real-time payment method, particularly among younger consumers.

North America

The US market is heavily card-dominated, but digital wallets are closing the gap fast. They reached 40% of US e-commerce checkouts in 2025 – still below the global average of 56%, but up sharply as younger consumers default to wallet-first payments ().

Apple Pay and Google Pay lead on mobile; PayPal remains the dominant standalone APM for desktop e-commerce, where biometric wallet authentication isn't available.

BNPL adoption is high relative to global averages – Klarna and Affirm both hold meaningful market share, particularly for mid-to-high ticket purchases. CashApp is growing as a payment method among younger demographics.

Canada follows a similar pattern, with Interac Online as the primary domestic bank transfer option.

Latin America

LATAM is one of the most payment-complex regions in the world. Card penetration varies significantly between and within countries, and consumer preference for cash-adjacent methods remains strong outside major urban centers.

- Brazil: PIX is now the de facto default. Launched in November 2020, it's instant, free for consumers, available 24/7, and interoperable across every bank and fintech in Brazil. Boleto Bancário – a printable payment slip redeemable at banks, ATMs, and lottery agents – remains important for cash-preferring consumers. Mercado Pago is the dominant digital wallet.

- Mexico: OXXO vouchers are essential for reaching consumers outside formal banking. OXXO operates over 20,000 stores nationally; for many Mexican consumers, buying an OXXO voucher and redeeming it online is the only viable checkout path. SPEI is the domestic real-time bank transfer network for those with bank accounts.

- Colombia: PSE (bank transfer) and Efecty (cash-based vouchers) are the main alternatives to cards.

- Chile: Webpay dominates online card processing; Sencillito handles cash payments.

Asia-Pacific

APAC has the world's most developed real-time payment infrastructure, with mobile wallets and instant payment networks accounting for the majority of e-commerce volume in most markets.

- India: UPI is the infrastructure. Google Pay India, PhonePe, and Paytm all route through UPI – the underlying rails are government-operated. For any merchant selling in India, UPI support is mandatory.

- China: Alipay and WeChat Pay dominate domestic e-commerce. Foreign merchants need local partnerships or payment aggregators to accept these methods.

- Indonesia: GoPay, OVO, and DANA are the leading e-wallets. Shopee Pay has regional reach across Southeast Asia.

- Philippines: GCash and Maya (formerly PayMaya) lead the market; both support recurring charges.

- Malaysia: Touch 'n Go eWallet is dominant; GrabPay has regional multi-market reach.

- Singapore: PayNow (government-backed real-time transfers) and GrabPay are widely used.

- Thailand: PromptPay is the national real-time transfer system; TrueMoney and LinePay have significant wallet share.

- Vietnam: MoMo is the leading e-wallet.

Middle East and Africa

The Middle East is primarily card-based for formal e-commerce, with strong PayPal usage across the GCC. Saudi Arabia and the UAE have seen rapid digital wallet adoption – STC Pay in Saudi Arabia, and Apple Pay and Google Pay across the Gulf Cooperation Council markets.

Africa presents a structurally different profile. Mobile money infrastructure – led by M-Pesa in Kenya and Tanzania – enables payments for large populations with limited access to bank accounts.

Nigeria is a significant e-commerce market where OPay and Paga are key mobile money operators. Cross-border payments in Africa remain complex, with high costs and limited interoperability across national systems.

Core insight: Every market you want to enter has a dominant local payment method – and entering without it means converting a fraction of your addressable customers.

Benefits of alternative payment methods

Higher checkout conversion

The average cart abandonment rate across global e-commerce sits around 70%, per . A meaningful share of that abandonment is payment-driven – the customer reached the checkout, found their preferred method missing, and left. In cross-border checkout, cart abandonment can average even higher because unfamiliar card flows add friction on top of an already unfamiliar experience.

Adding the right APMs reduces that drop-off at the source. For example, MEGOGO, a streaming platform serving subscribers across Eastern Europe, discovered Polish customers were abandoning checkout because BLIK wasn't available.

After adding BLIK with localized routing for Polish issuers through Solidgate, payment conversion increased by 3.5% and subscription churn dropped 5%.

→ Read the full

Beyond method availability, builds an additional trust signal – customers who see a familiar payment mark are more likely to complete the purchase.

Broader addressable market

Card-only checkout excludes a structurally large share of consumers in high-growth markets. In , 60 million adults don't own a credit card – but 170 million use PIX. In Nigeria, mobile money reaches populations that have never held a bank account. In Mexico, OXXO vouchers are the only viable checkout path for a significant share of the population outside major cities.

For merchants with global ambitions, offering the right alternative payment options improves conversion among existing customers and opens revenue from consumers that card infrastructure can't reach at all.

Lower declines and better authorization rates

Card declines are a persistent drag on , particularly for cross-border transactions where the issuing bank treats the merchant as foreign. Local payment methods – especially bank-transfer-based APMs and real-time networks – carry structurally lower decline rates, because the payment rails are built for domestic volume and the issuer knows the merchant context.

For subscription businesses, soft declines account for 70–90% of all recurring payment failures – and most are recoverable. Adding direct debit or wallet-based recurring options alongside card billing creates a structural fallback when cards fail, reducing involuntary churn without adding friction to the customer experience.

Stronger security and fraud protection

Many alternative payment methods carry lower fraud risk than card payments by design. Digital wallets tokenize card credentials – the merchant never sees the raw card number, reducing exposure to data breaches.

Bank transfers via open banking are push payments – the customer initiates the transfer, so there's no card number to steal or replicate, and no unrecognized charge to dispute. Real-time networks like PIX and UPI authenticate at the bank level, reducing exposure. Prepaid methods cap risk at the loaded balance.

For subscription businesses, the fraud problem is mostly not fraud at all. Up to 75% of subscription chargebacks stem from legitimate customers disputing valid charges – forgotten trials, unrecognized billing descriptors, or inaccessible cancellations (). Open banking transfers, real-time networks, and direct debit eliminate that category of dispute entirely. The customer explicitly initiated the payment, so there's nothing to claim as unrecognized.

Core insight: The right APMs determine which markets you can enter, which customers you can reach, and how much each transaction costs to process.

How to add alternative payment methods to your business

Here's how to add APMs without creating a fragmented stack.

Prioritize by market, not by integration ease

Start where your conversion gap is largest. For Brazil, that's PIX. For Poland, BLIK. For the Netherlands, iDEAL.

That’s exactly what Tickets Travel Network, a European travel platform, did when expanding into LATAM, MENA, and Southeast Asia. Instead of adding what was quickest to integrate, they identified the dominant local method per market – Bizum for Spain, UPI for India – and built their expansion sequence around those gaps.

→ See the full

Check recurring support before committing

Not every APM supports recurring charges – and many that do have limitations on retry logic, mandate management, or cancellation flows. A wallet that handles one-time payments won't keep a subscription alive through a failed renewal.

Solidgate flags recurring capability per method across its full APM catalogue and applies smart retry logic that lifts first retry conversion rates by 30%.

Integrate once, not per method

Every APM integrated directly means a separate build, separate maintenance, and separate reconciliation format. That overhead compounds with every market you add. A – like Solidgate's – connects cards, APMs, and recurring billing through one integration, allowing you to activate new methods through configuration, not code.

Plan reconciliation before go-live

Different APMs settle on different timelines and in different currencies. Each processor uses different data structures – reconciling them manually is where finance ops teams lose hours.

centralizes settlement reporting across all connected APMs and in one dashboard, with like-for-like settlements that avoid fractured payouts and FX exposure across jurisdictions.

Core insight: Getting APMs right means choosing by market and then building a stack that handles recurring support, integration overhead, and reconciliation without compounding with every market you add.

Your APM stack is your market access strategy

Every market you want to enter has a dominant local payment method. Get it live before your competitors do – and get it live without a new engineering sprint per market.

Solidgate is a that connects through a single integration, with smart routing, centralized reconciliation, and recurring support documented per method.

to map which methods would move the needle for your expansion.

From one region to global travel coverage

How Tickets Travel Network expanded to LATAM, MENA & SEA with Solidgate

Frequently asked questions

Alternative payment methods (APMs) are any payment mechanism outside cash and traditional card networks – Visa, Mastercard, Amex, and similar international schemes. They include digital wallets (PayPal, Alipay), mobile wallets (Apple Pay, Google Pay), real-time payment networks (PIX, UPI), bank transfers and open banking (iDEAL, SEPA), BNPL (Klarna, Affirm), direct debit, prepaid cards and vouchers, carrier billing, and cryptocurrency payments.

APMs increase checkout conversion by matching customers with their preferred payment method. They reduce card decline rates – particularly in cross-border contexts – lower fraud exposure through push payments and bank-level authentication, and expand the addressable market to consumers card infrastructure can't reach. For subscription businesses, APMs like direct debit and wallet-based recurring payments reduce involuntary churn caused by card expiry and failed retries.

APM acceptance depends on the method and market. For instance, digital wallets (PayPal, Alipay) dominate in China and LATAM, and mobile wallets (Apple Pay, Google Pay) are broadly accepted across most major markets. Real-time networks like PIX and UPI have become the default in Brazil and India rather than alternatives. Overall, APM coverage is increasing as more merchants recognize the conversion impact of local method support.

By transaction volume, the most significant APMs globally are: PayPal, Alipay and WeChat Pay (China), UPI (India), PIX (Brazil), iDEAL (Netherlands), BLIK (Poland), SEPA Direct Debit (Europe), Klarna (BNPL, global), and Apple Pay and Google Pay (mobile wallets, global).

The fastest-growing APMs are government-backed real-time payment networks. PIX and UPI continue expanding in volume and use case coverage. Singapore's PayNow, Thailand's PromptPay, and African mobile money systems – OPay and Paga in Nigeria – are growing rapidly. In Europe, Wero – the pan-European A2A wallet launched by 16 major banks in 2024 – is replacing Giropay, iDEAL, and Paylib across Germany, France, Belgium, and the Netherlands. Open banking-powered instant bank transfers are also expanding as a lower-cost card alternative across the EU and UK.

E-commerce and digital goods are the largest users of APMs by transaction volume. Subscription businesses – SaaS, streaming, fitness apps, edtech – rely on direct debit and digital wallets for recurring billing. Travel businesses use BNPL to reduce the sticker shock of high-value bookings. Financial services and cross-border remittance platforms increasingly use real-time networks and mobile money.

Hundreds of APMs operate globally, ranging from major international platforms to highly localized domestic systems. Solidgate supports over 100 APMs across markets, and the number continues to grow.

Alternative methods of payment matter because card penetration is uneven globally and checkout conversion depends directly on whether customers find their preferred method. Businesses that match their checkout to local expectations consistently outperform those that rely on card-only setups.