How to use credit card authorization holds to prevent chargebacks and fraud

Payments 101

23 Apr 2025

8 min

Daniel Yaremchuk

Risk Manager, Solidgate

Safer payments, fewer disputes, and stronger trust—that’s the value of credit card authorization holds. Merchants can reduce fraud, boost approval rates, and stay compliant.

Credit card authorization holds are one of the most effective—and overlooked—payment flow optimization tools to protect your business from chargebacks and payment disputes. When a merchant places an authorization hold on a credit card, they're essentially reserving funds before the transaction is settled, creating a pre-authorization that helps secure payments.

An authorization hold on credit card accounts serves as a safety mechanism that protects both buyers and sellers. When used strategically, these holds combine the best of both worlds: security for the business and a smoother experience for customers.

Simply put, you're taking control of your payments by securing funds upfront before fulfilling the order. This means fewer risks, more certainty, and a significant reduction in fraud. At Solidgate, we've been testing credit card authorization holds with various delayed settlement intervals across different business models. The results speak for themselves:

- Up to 20% reduction in VAMP rate

- Fewer friendly fraud cases

- Broader access to

- Better control of when and how funds are settled

- Room to design payment processes tailored to your business

- No refund fees if the authorization was canceled

- Better customer experience due to instant refunds

In this article, we'll show you how to leverage credit card authorization holds and delayed settlement to protect your revenue, stay compliant, and scale your business without the risk.

What's a credit card authorization hold

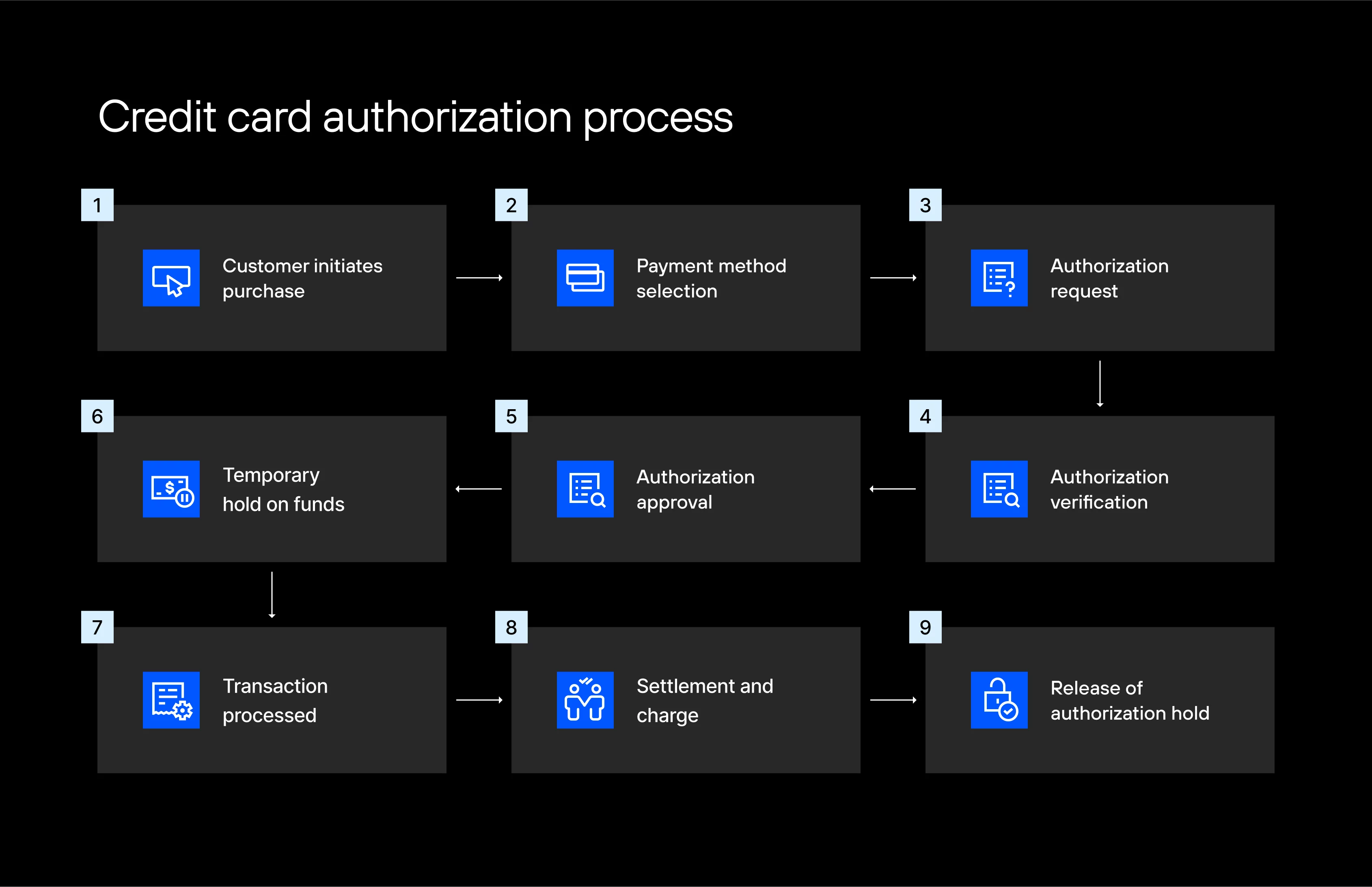

A credit card authorization hold (or "auth hold") is a temporary lock on a customer's credit or debit funds for a specific transaction amount. This type of credit card hold is common across many merchant category codes, from e-commerce to car rentals and hotels. When you initiate a purchase authorization, the approves by reserving those funds on the customer's account, reducing their available credit limit by that amount.

No money moves to you at this stage—it’s simply put on hold. Once you finalize the transaction (by "capturing" the payment), the hold is replaced by an actual charge, and the bank transfers the funds to your account. If you don't capture (or if you cancel the transaction), the hold is released, typically within 2-10 business days, and the funds return to the customer's available balance.

Key characteristics of authorization holds on credit cards that merchants should know:

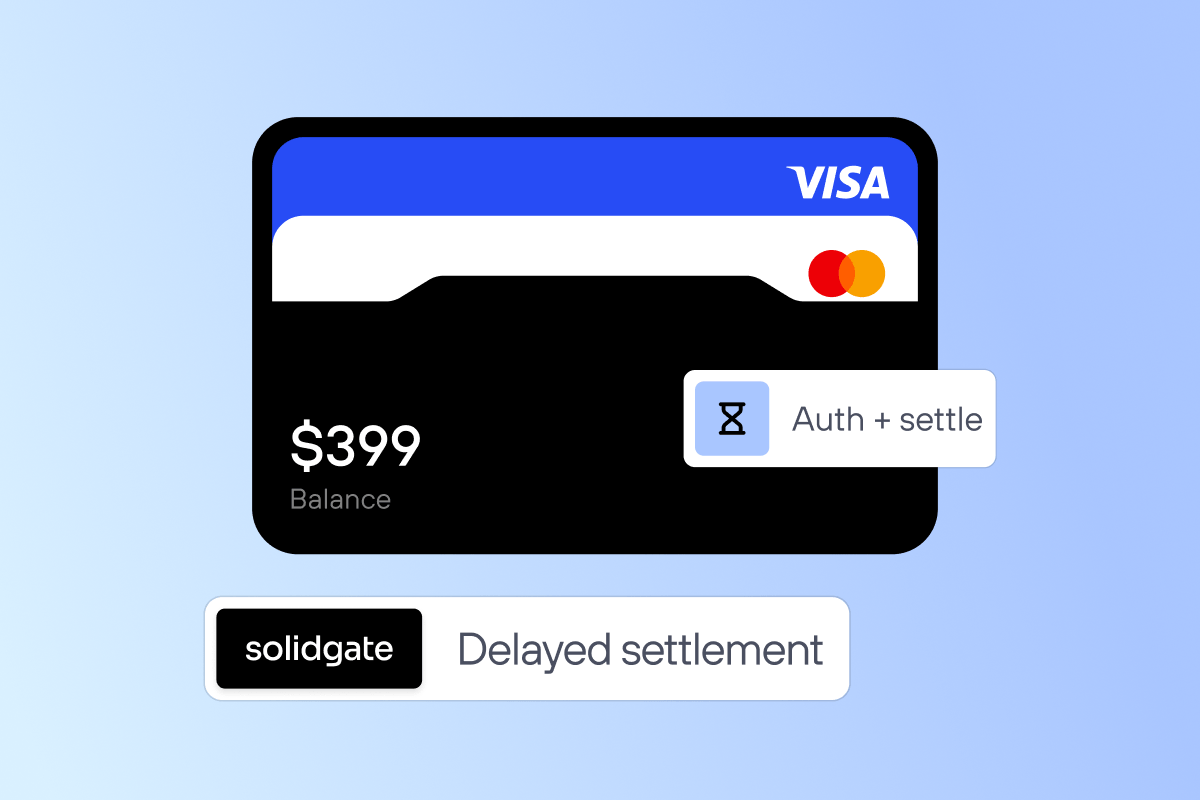

- They are time-limited: The time the transaction remains in an "auth" status / is on hold before the capture is called a settlement interval. The maximum allowable settle interval is 144 hours (6 days); it varies across different payment providers, but we at Solidgate recommend setting it to 120 hours. This gives you enough time to resolve any potential issues before the transaction is settled, while still complying with rules.

- They ensure funds availability: The held amount is locked in for that transaction. The cardholder can't spend it elsewhere or withdraw it. Without a hold, a customer could make a purchase and then empty their account, leaving nothing for you when you go to collect, and you'd get stiffed.

- They are not charges (until captured): Customers might see a "charge" line item on their statement, but it's not an actual deduction yet, which helps prevent disputes. The pre-authorization simply verifies that the customer has the funds to cover the purchase.

Read more on Auth + settle payment flow in our .

Use cases in subscription businesses

Fighting fraud before it happens

Every authorization request is an opportunity to stop fraud in its tracks. When you run a credit card authorization hold, the verifies the card's details (number, expiration, CVV) and checks if the card is reported lost or stolen. If something looks off, the issuer will decline the settlement of the transaction, sparing you from fulfilling a fraudulent order.

For free trials, a common strategy is to perform a $1 or when the user signs up. This small hold verifies the card's validity and ensures it's in good standing, filtering out fraudulent or non-paying users before giving free access.

If the card is declined, you won't receive the free service. If it's approved, you might leave the $1 on hold or void it, and when the trial ends, you charge the subscription fee. This way, the customer's card is already tested, and they're aware of the upcoming charge.

Reducing chargebacks and disputes

Authorization holds on credit cards play a critical role in reducing chargebacks by verifying that funds are available before committing to a transaction, offering a clear trail of authorization that proves the legitimacy of the purchase.

Improving your VAMP ratio

Visa has introduced a new that combines fraud and chargeback monitoring into one metric called the VAMP ratio. This ratio counts all fraud alerts and chargebacks against your total sales count.

With fraud alerts associated with RDR and CDRN now counting towards your VAMP ratio, reducing TC40 alerts has become top of mind for online merchants. That’s where authorization holds with a delayed settle interval can serve as a silver bullet.

Why? When a transaction is in the "auth" status, the bank cannot initiate a chargeback or report fraud (TC40). Instead, the customer is directed to your support team for a refund or dispute resolution. By setting the settle interval to 120 hours, you have time to handle customer complaints or address potential fraud, all without triggering a chargeback.

This helps reduce the risk of fraud claims and improves your VAMP standing, as you avoid the fraud alerts and chargebacks that would typically count against your VAMP ratio. By implementing this strategy, our merchants have seen an average reduction in their VAMP rate of 15-20%.

Get more field-tested product strategies to reduce VAMP in our .

Reduce unrecognized transaction disputes

Even when charges are legitimate, customers sometimes dispute them because they don’t recognize the transaction on their statement (a form of friendly fraud or misunderstanding). Authorization holds can mitigate this.

When a customer sees a charge labeled as “Pending [Your Company]” right after purchase, it’s a clear reminder of what that transaction is. If something is wrong – e.g., a customer sees a pending charge they don’t recall and writes to the email on the statement to verify the purchase– they have a chance to contact you immediately.

Avoiding failed captures and late presentments

Authorization holds help you stay within processing time limits, preventing "administrative" chargebacks. Card network rules require you to settle transactions within a set timeframe after authorization.

If you don't, the issuer may decline the late capture or even raise a dispute for late presentment (Visa reason code 12.1, "Late Presentment"). By using credit card authorization holds properly, you ensure you capture while the authorization is still valid.

For Visa, that's typically within 7 days for most transactions. If you were to authorize and then wait too long (say, two weeks) without any hold, you run the risk that the card is no longer "open to buy"—the account could be closed or funds gone.

In such cases, the issuer can initiate a chargeback when you finally settle, citing that you didn't complete the process in time. An authorization hold on a credit card forces you to either settle within the allowed window or re-authorize, thereby shielding you from late-settlement disputes.

Improving your refund system

When you use credit card authorization holds, you're not just reducing fraud and disputes—you're also improving your refund system. Here's how:

- No refund fees if the transaction is canceled while in auth status

This is a big cost-saver for merchants compared to traditional refunds. With authorization holds, if the transaction is canceled before capture, no refund fee is incurred. - Instant refunds

When a refund is necessary, it's processed instantly—there's no need to wait for the settlement cycle to complete. Your customers get a faster refund and a better customer experience. The hold is released, and funds return to the customer's credit limit immediately.

Solidgate tips for authorization holds

Implementing authorization holds effectively requires some finesse. Here is what we at Solidgate recommend as best practices for our merchants:

Balance risk and UX with settlement intervals

The timing of when you settle transactions can directly impact your cash flow and chargeback risk. Delaying settlement too much could lead to expired authorizations, which might force you to reauthorize or, worse, risk non-payment due to a failed capture.

While 120 hours is the recommended interval, it's important to test and monitor the impact on your specific business model. If you have recurring payments or time-sensitive products, you may need to adjust the interval to balance conversion rates with risk management. Different types of credit card holds may require different settlement schedules, depending on your and business needs.

Solidgate merchant? You can customize your settlement intervals for first and recurring payments in the .

Work with your payment orchestrator to configure authorization alerts

Many modern systems can notify you (or even the customer) when an authorization is about to expire or if an auth was declined for a specific reason. For example, if a recurring billing auth is declined with an "insufficient funds" response, you might trigger an immediate email to the customer to update their payment method.

Track your . If you see a lot of do not honor or fraud declines, that might indicate you need to tighten your fraud screening. Authorization data is rich with insights: use it to refine your fraud rules (e.g., decline transactions that receive soft declines repeatedly) and to time your capture attempts for optimal success. Some issuers may approve a retry at a different time of day, which your processor can help identify.

Related read:

Communicate with customers

Never forget the customer's perspective. It's wise to clearly communicate to your customers when and why you place an authorization hold on their credit card. Placing an authorization hold on credit card accounts requires transparency to maintain trust. In subscription models, remind users before a big charge hits—or at least ensure the descriptor is recognizably yours—so the hold isn't a mystery.

Related read: .

Credit card authorization holds combine the best of both worlds: security for the business and a smoother experience for customers when used correctly. By integrating auth holds into your payment flows, you can dramatically cut down on fraud and chargebacks, keeping your chargeback ratio well below danger zones and your VAMP score squeaky clean.

More importantly, you'll be building a resilient revenue pipeline for your growing business. In an environment where even a fraction of a percent in dispute rate matters, the merchants who master authorization holds will have a serious edge over those who "authorize and pray."