What is an Issuing bank – Definition and explanation

Payments 101

Updated 20 Jan 2026

8 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Issuing banks authorize and settle card transactions, impacting payment success, fraud prevention, and conversion rates for businesses.

Whether you’re a newcomer to the world of finance or seeking to deepen your understanding, this article will provide you with a clear and insightful overview of the crucial functions and significance of issuing banks. We’ll delve into their core responsibilities, explore their impact on diverse financial activities, and shed light on how they contribute to the seamless functioning of our modern economic system.

Issuing bank definition

An issuing bank, also known as an issuer, is a financial institution that issues credit or debit cards to consumers or businesses. The issuing bank plays a critical role in the process of authorizing and settling transactions made using the card.

When a customer uses their card to make a purchase, the issuing bank authorizes the transaction by verifying the cardholder’s account details and ensuring that they have sufficient funds available to cover the purchase. If the transaction is approved, the issuing bank then transfers the funds to the merchant’s account and records the purchase on the cardholder’s account.

In addition to issuing credit and debit cards, an issuing bank may also offer other banking services, such as loans, savings accounts, and other financial products. Many issuing banks partner with payment processors and card networks, such as Visa and Mastercard, to provide their cardholders with broader acceptance and global accessibility.

Overall, issuing banks play a crucial role in the global financial system by enabling consumers and businesses to make purchases and access funds conveniently and securely.

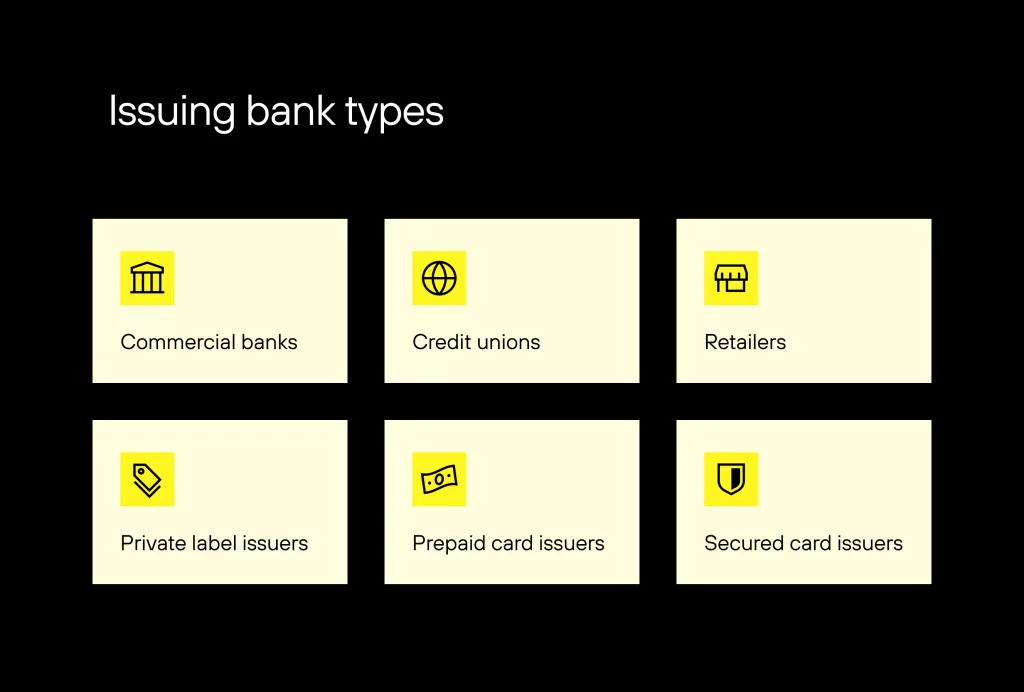

Issuing bank types

There are various types of issuing banks that are known, depending on their specific business model and the types of cards they issue. Here are some of the most common types of issuing banks:

- Commercial banks: These are traditional banks that provide a range of financial services, including credit and debit card issuance.

- Credit unions: These are not-for-profit financial institutions that are owned by their members and provide a range of financial services, including credit and debit card issuance.

- Retailers: Some large retailers issue their own credit cards to customers, which can be used exclusively at their stores or at partner stores.

- Private label issuers: Private label issuers specialize in creating and managing branded credit cards for businesses, such as airlines and hotel chains.

- Prepaid card issuers: Prepaid card issuers issue cards that are preloaded with funds and can be used for purchases, ATM withdrawals, and other transactions.

- Secured card issuers: These issuers provide credit cards that require a security deposit to be placed on the card, which is then used as collateral in case the cardholder fails to make payments.

In general, the types of issuing banks can vary widely depending on the specific services they provide and the markets they operate in.

How issuing banks impact conversion rate

The issuing bank can have a significant impact on the conversion rate of digital businesses, particularly those that rely on online payments. Here are some ways in which issuing banks can impact conversion rates:

- Payment processing: The issuing bank plays a critical role in the payment processing chain by authorizing and settling transactions made with credit and debit cards. If the issuing bank’s payment processing systems are slow or unreliable, this can lead to declines in transactions and lower conversion rates.

- Fraud prevention: Issuing banks are responsible for preventing fraud and ensuring that only legitimate transactions are processed. If an issuing bank’s fraud prevention systems are too strict, this can result in legitimate transactions being declined, leading to lost sales and lower conversion rates. Conversely, if the fraud prevention systems are too lax, this can result in more fraudulent transactions being processed, leading to chargebacks and reputational damage.

- User experience: The user experience of a digital business can be greatly impacted by the issuing bank. If the process for entering and processing payment information is confusing or unreliable, this can lead to cart abandonment and lower conversion rates.

- Card acceptance: The types of cards accepted by a digital business can impact conversion rates, as customers may be more likely to complete a purchase if they can use their preferred payment method. This is often impacted by the issuing bank’s partnerships with payment networks and the types of cards they issue.

In a broader perspective, the can have a significant impact on the conversion rate of digital businesses, and it’s important for businesses to choose the right issuing bank partner and maintain a good relationship with them in order to optimize their conversion rates.

Issuing banks over the world: US and EU

There are several key differences between US and EU issuing banks that can impact the products and services they offer, as well as the regulatory environment in which they operate. Here are a few key differences:

- Regulation: The US and EU have different regulatory environments for financial institutions, with different rules and requirements for issuing banks. For example, the US has the Dodd-Frank Wall Street Reform and Consumer Protection Act, which imposes strict regulations on banks and financial institutions, while the EU has the Payment Services Directive, which sets rules for payment service providers.

- Payment systems: The payment systems used in the US and EU can also vary, with different standards and protocols for payment processing. For example, in the US, the dominant payment networks are Visa and Mastercard, while in the EU, there is a wider range of payment networks and methods, including SEPA (Single Euro Payments Area).

- Card products: The types of card products offered by US and EU issuing banks can also differ. For example, in the US, credit cards are more commonly used for everyday transactions, while in the EU, debit cards are more popular. Additionally, US banks often offer rewards and cashback programs to incentivize credit card usage, while EU banks may focus more on security and fraud prevention.

- Customer data: The handling and protection of customer data is also subject to different regulations in the US and EU. For example, the EU’s General Data Protection Regulation (GDPR) imposes strict requirements on how companies handle and protect customer data, while the US has a patchwork of regulations at the federal and state levels.

While there are many similarities between US and EU issuing banks, the differences in regulation, payment systems, card products, and customer data can impact the way these banks operate and the products and services they offer.

Interesting facts about issuing banks

There are many interesting specifications of issuing banks around the world, but here are a few notable ones:

- National Bank of Cambodia: The National Bank of Cambodia was the first central bank in the world to launch a blockchain-based payment system in 2020. The system, called Project Bakong, allows users to make real-time payments using a mobile app, and is intended to help modernize the country’s financial system and increase financial inclusion.

- JPMorgan Chase: JPMorgan Chase is the largest issuer of credit cards in the United States, with a market share of over 20%. In addition to its consumer credit card business, JPMorgan Chase is also a major of corporate credit cards, and offers a wide range of rewards and cashback programs to its customers.

- ICICI Bank: ICICI Bank, based in India, is one of the first banks in the world to offer “contactless” debit and credit cards, which use near-field communication (NFC) technology to allow users to make payments without swiping or inserting their cards. This technology has become increasingly popular around the world, as it offers a more convenient and secure way to make payments.

- Swedbank: Swedbank, a major bank in Sweden, has been at the forefront of using artificial intelligence (AI) and machine learning to improve its risk management and fraud detection capabilities. The bank uses AI to analyze customer data and identify patterns of suspicious activity, helping to prevent fraud and other financial crimes.

- UnionPay: UnionPay, based in China, is the largest card payment organization in the world, with over 8 billion cards issued. The company operates a global network of payment terminals and ATMs, and has partnerships with banks and merchants in over 170 countries.

These are just a few examples of the many interesting specifications of issuing banks around the world. As the financial industry continues to evolve and innovate, we can expect to see even more exciting developments in the years to come.

Issuing bank and payment processor

Issuing banks and payment processors work together closely to ensure that transactions are processed quickly and securely. Here’s a brief overview of how the two entities interact:

- Authorization: When a customer makes a payment with a credit or debit card, the transaction is first sent to the payment processor for authorization. The payment processor sends the transaction details to the issuing bank, which then approves or declines the transaction based on the available funds, the customer’s creditworthiness, and other factors.

- Settlement: Once a transaction is authorized, the payment processor then facilitates the settlement of funds between the merchant’s bank and the issuing bank. This involves transferring funds from the customer’s account to the merchant’s account, minus any fees charged by the payment processor and the issuing bank.

- Disputes and chargebacks: In the event of a dispute or chargeback, the payment processor and issuing bank will work together to investigate the issue and determine the appropriate course of action. This may involve providing documentation and evidence to support the merchant’s position, or refunding the customer for a disputed transaction.

- Risk management: Payment processors and issuing banks also work together to manage risk, by monitoring transactions for fraud and other suspicious activity. This may involve sharing data and insights about patterns of fraud or chargebacks, as well as implementing new security measures or technologies to prevent fraud and protect customer data.

The relationship between issuing banks and is critical to the functioning of the payments ecosystem, and both entities must work together closely to ensure that transactions are processed quickly, securely, and accurately.

Summary

- An issuing bank is a financial institution that issues credit or debit cards to consumers and businesses.

- The types of issuing banks include credit unions, community banks, national banks, and international banks.

- Issuing banks play a critical role in the digital business ecosystem by impacting the conversion rate of online transactions and helping to prevent fraud and chargebacks.

- There are some differences between US and EU issuing banks, including differences in regulation, consumer protection, and liability for fraudulent transactions.

- Issuing banks and payment processors work closely together to authorize transactions, facilitate settlement, manage disputes and chargebacks, and monitor for fraud and other suspicious activity.

- Some interesting specifications of issuing banks around the world include the National Bank of Cambodia’s blockchain-based payment system, JPMorgan Chase’s large market share in the US credit card market, ICICI Bank’s contactless payment technology, Swedbank’s use of AI for risk management and fraud detection, and UnionPay’s global network of payment terminals and ATMs.