Merchant Accounts: Their Role and How to Secure Yours

Payments 101

Updated 16 Jul 2026

8 min

Andrii Stoikov

Head of Support, Integration, Billing Operations, Solidgate

Secure payments, better cash management, and happier customers - learn all about merchant accounts. Reduce risks, accelerate funds, and improve checkout experience.

Merchant accounts have an important role in ensuring the seamless flow of transactions between businesses and customers. This article is intended to provide business experts with in-depth knowledge of merchant accounts. We will define them, underline their important function, and provide specific recommendations for securing and optimizing these financial tools.

TL;DR

- A merchant account is a specialized bank account that holds funds from card and electronic payments before transferring them to your regular business bank account; without one, you're limited to accepting cash.

- It's distinct from a business bank account: a merchant account holds only customer-sale funds in transit, while a business bank account runs day-to-day operations like payroll and rent.

- Getting one means defining your requirements (countries, card brands, currencies, payment types), comparing provider fees (transaction, chargeback, reserve, setup, monthly, early termination), passing a Know Your Customer (KYC) check, and setting up the payment gateway with live credentials. High-risk businesses may face higher fees or reserve terms.

- To avoid closure, watch the thresholds: many financial institutions set the chargeback limit around 1% of total transactions, with a lower fraud threshold. Terms violations, security breaches, processing issues, and inactivity can also end your account, and a closure history makes reopening elsewhere harder.

What is a Merchant Account?

A merchant account is a type of bank account that allows businesses to from customers, principally by debit and credit cards and by other electronic payment methods. When a customer pays for goods or services using a card, the payment is processed through the merchant account, which transfers the funds from the customer’s account to the merchant’s account.

It’s hard to imagine a successful modern business in 2023 without electronic payments. Today, they are a must. If a company does not have a merchant account, it will be restricted to accepting only cash payments. This limitation can affect how the business operates, particularly as the use of cash is drastically decreasing.

Such accounts are typically provided by Acquiring banks or other financial institutions: PSPs and Independent Sales Organizations (ISOs). The merchant account plays a critical role in the transaction flow by providing merchants with a secure and reliable way to accept customer payments.

Merchant Account vs Business Bank Account

A merchant account and a regular business bank account have a significant difference. A traditional business bank account is used for all aspects of business operations, such as paying employees, rent, and website expenses. In contrast, a merchant account is used solely for holding funds from customer sales and transferring them to the main business bank account.

Merchant Account Role in the Typical Transaction Flow

Merchant accounts are essential in the complex process when a customer initiates a credit card transaction. At the beginning of the transaction (the card is tapped, swiped, or inserted at the POS (Point of Sale), or the card information is filled out for online checkout), the payment is sent to the merchant’s credit card processor, who then contacts the issuing bank via the credit .

The issuing bank confirms whether the customer is authorized to make the payment and has enough funds or credit to cover the cost of the transaction, and if so, approves a funds transfer to that amount. The funds are then deposited into the merchant account, which is owned by the merchant’s credit card processor and acts as a temporary holding place for the funds. Only after the funds are deposited into the merchant account can they be transferred to the merchant’s actual business bank account.

How to Get a Merchant Account?

Determine Your Business Requirements

The first step is to determine your business requirements, such as your target countries, , card brands (VISA, Mastercard, AMEX, Discover, Diners, UnionPay), and currencies you want to accept. Consider the payment types you wish to get according to the business model (one-time, subscription, and ).

Choose a Merchant Account Provider

When choosing a financial institution to open a with, it’s essential to consider their fees, transaction rates, customer support, and other features to ensure they meet the needs of your business.

The fees can vary depending on the financial institution, the type of account, and the services offered. Here are some of the most common fees associated with merchant accounts:

- Transaction fees: Transaction fees are charged for each transaction processed through your account. This fee is typically a percentage of the transaction amount, called a discount rate, plus a fixed amount per transaction. Also, there can be a specific fixed fee for successful and declined transactions (captured and void transactions) and for refunded transactions accordingly.

- Chargeback fees: This fee is charged every time the merchant receives a chargeback from a customer.

- Reserve: Some financial institutions may require a reserve in the merchant account as a security deposit. This fee is typically a percentage of the transaction volume and can be held for a set period.

- Setup fees: Some financial institutions may charge a one-time setup fee to establish a merchant account.

- Monthly fees: Monthly fees may be charged to maintain the account. These fees can vary depending on the financial institution and the type of account.

- Early termination fees: Some merchant account providers may charge a fee if you terminate the account before the end of the contract term.

It’s important to carefully review any agreement’s fee structure and terms before signing up. Additionally, it’s a good idea to compare the fees and features of multiple providers to find the best fit for your business. If this seems overly complicated, you’re not alone.

Fill Out an Application and Provide All Required Documents

Once the provider is chosen, you must fill out an application. This typically requires you to provide information about your business, including incorporation documents, business registration, business owner/director IDs, tax identification numbers, bank statements, and processing history.

Undergo a KYC Check

Acquirers and PSPs consider a variety of criteria, such as the length of time the company has been established, history of bankruptcy, past credit issues, and any previous merchant accounts. Merchant vendors might also analyze if your business is susceptible to credit card fraud. If a business is deemed high risk, the vendor might initially set higher transaction fees or apply special Reserve terms to offset that risk.

Get the Approval And Live Credentials

Live credentials for merchant accounts are private and should only be known by the merchant who owns the account and their authorized personnel. Merchant accounts typically require login credentials such as a username and password, which give access to the merchant admin panel with all necessary settings. For the US account, it can also be a VAR sheet that contains all the required inputs to set up the payment gateway.

Set Up the Payment Gateway

Once your merchant account is approved, you will need to set up a payment gateway using live credentials provided by the Acquirer to process payments.

Start Accepting Payments

After the payment gateway is set up, you can start accepting customer payments using credit and debit cards. It’s important to note that opening a merchant account can be complex and time-consuming. Ensure you work with a reputable provider with a proven track record of reliability and trustworthiness when processing your customers’ payments and managing sensitive financial information.

How to Prevent Your Merchant Account From Closure?

Merchants must realize that setting up a merchant account doesn’t mean they’re entitled to the service. They must follow the rules outlined in their agreement with the payment processor or acquiring bank. By knowing why their account may be terminated, merchants can take the necessary steps to keep their accounts in good standing and prevent any interruptions to their payment processing activities.

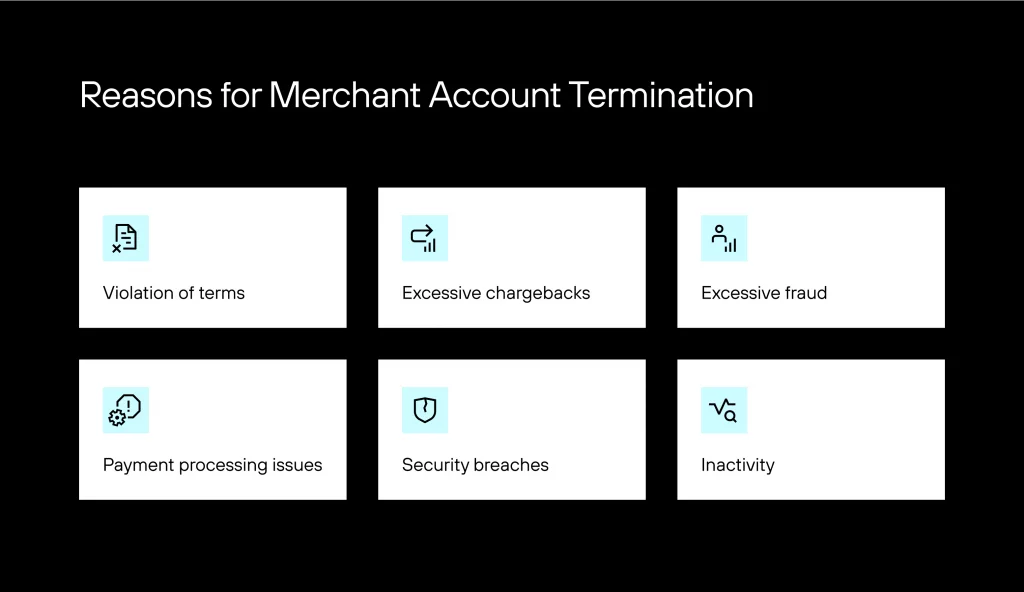

Merchant account closures can occur for a variety of reasons.

Violation of Terms

If a merchant violates the terms of the agreement with their payment processor or acquiring bank, their merchant account can be closed. This can happen if the merchant engages in fraudulent or illegal activities or violates industry regulations.

Excessive Chargebacks

Chargebacks occur when customers dispute a transaction, and the funds are returned to the customer. If a merchant receives , their payment processor or bank may close their account. This can happen if customers are disputing transactions due to poor customer service, product quality issues, or other problems. Many financial institutions set the chargeback threshold at around 1% of total transactions.

Excessive Fraud

Financial institutions may set the threshold lower than the chargeback threshold since fraudulent transactions can result in chargebacks and additional financial losses. The specific fraud threshold can vary depending on the industry, the type of transactions being processed, and other factors.

Payment Processing Issues

Financial institutions may close the merchant account if a merchant’s is not functioning correctly or in compliance with industry standards.

Security Breaches

Merchants are responsible for safeguarding sensitive customer data, such as credit card numbers and personal information. The financial institution may close the merchant account if a security breach occurs and customer data is compromised.

Inactivity

If a merchant’s account remains inactive (dormant) for an extended period, their payment processor or bank may close it. This can happen if the merchant stops using the account for processing payments or if they go out of business.

Merchants must maintain good business practices and comply with their agreement with the financial institution to avoid the risk of account closure. If a merchant does have their account closed, it can be challenging to open a new account with another financial institution, as a history of account closures can be viewed negatively.

Merchants must maintain good business practices and comply with their agreement with the financial institution to avoid the risk of account closure. If a merchant does have their account closed, it can be challenging to open a new account with another financial institution, as a history of account closures can be viewed negatively.

Conclusions

This is how the merchant account allows you to accept credit and debit card payments and enable online payments, which have become essential to everyday business operations!

Online payment processing provides customers with a convenient and secure payment option, which can help increase sales and remove geographical boundaries. From the merchant's perspective, it improves cash flow; hence, businesses can receive funds from sales faster.

Moreover, eCommerce merchant accounts can be secured with fraud detection and chargeback prevention tools. It can help reduce the risk of fraudulent transactions.

Accepting credit and debit card payments can improve the customer experience. Having a merchant account can help businesses build credibility with customers, as it shows that they are legitimate and professional businesses.

Frequently asked questions

It is a specialized bank account that enables businesses to accept credit and debit card payments. It serves as an intermediary between your business, the customer, and the payment processor. Essentially, it’s your gateway to receiving electronic payments from customers.

They are integral in addressing chargebacks. When a customer disputes a transaction, the funds are temporarily taken from your account while the issue is investigated. If you can provide evidence that the transaction was legitimate, the funds will be returned to you. However, if not, the funds may be permanently debited from your account. It’s crucial to understand the chargeback process and take proactive steps to prevent them.

To reduce chargebacks and protect your account, consider implementing strong fraud prevention measures, maintaining clear billing descriptors, offering exceptional customer service, keeping detailed transaction records, and staying informed about industry regulations and best practices. These actions will help ensure the security of your Merchant Account.