Visa & MC Chargeback and Fraud Monitoring Programs: An Ultimate Guide

Industry

Updated 19 Jun 2026

6 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Monitoring programs from Visa and Mastercard track fraud and chargebacks. Keep metrics under control to avoid fines, protect your reputation, and maintain the ability to accept card payments.

Both Visa and Mastercard have fraud monitoring programs for merchants in place to track chargeback and fraud performance. In this article, you’ll find all the necessary information about different monitoring program types and what to do next if you get placed into one.

Card schemes (Visa, Mastercard) have established monitoring programs that set acceptable thresholds for fraud and disputes to monitor and control merchants’ performance regarding chargebacks and fraudulent transactions. Every scheme network has its own program that determines the acceptable level of fraud and chargebacks.

Visa and Mastercard calculate the thresholds differently. If the outlined thresholds are violated, the scheme networks will place the merchant into their monitoring program. While placed in a program, you may incur fines and additional fees until you normalize fraud and/or chargeback metrics to the appropriate level.

Getting into monitoring programs is not considered to be common and thus should be treated seriously. If a merchant is placed into the monitoring program, immediate action should be taken. A remediation plan with clear action points should be submitted to your acquirer.

Failure to comply with the outlined timelines given for chargeback or/and fraud rate mitigation can result in heavy fines placed by the schemes and the eventual ‘blacklisting’ of the merchant. In case this happens, the merchant’s ability to accept card payments is at risk.

Visa Monitoring Programs

Visa has two monitoring programs:

- Visa Dispute Monitoring Program (VDMP) - for merchants violating the appropriate chargeback level ratio thresholds, and

- Visa Fraud Monitoring Program (VFMP) - for merchants with unacceptable fraud rates

If a merchant is placed in any of the two programs, this should be taken seriously, and corrective measures should be taken asap.

Visa reviews a merchant’s fraud and chargeback metrics on a monthly basis. In case any merchant breaches the set thresholds, Visa will contact the bank to require a remediation plan for the respective merchant.

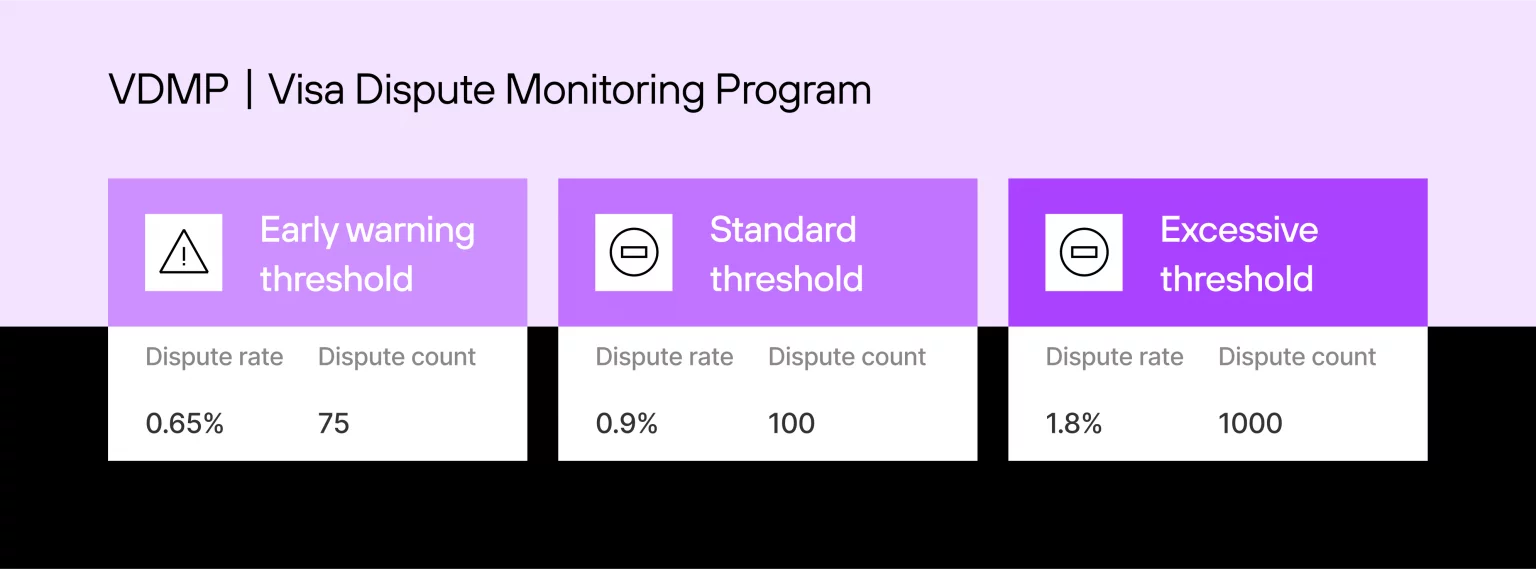

Visa Dispute Monitoring Program (VDMP)

VDMP applies to merchants with a high chargeback (dispute) ratio in a particular month. A merchant will be placed into this Visa chargeback program if both of the following chargeback thresholds are violated:

- The total number of chargebacks filed by users against the merchant over a month.

- Dispute the sales transaction count over a period of a month.

There are three stages of the VDMP: Early Warning, Standard, and Excessive.

Please note that merchants identified by Visa as high brand risk MCCs would automatically be placed in a VDMP High-Risk Program in case of the threshold violation. Non-compliance assessments and fees can be applied to such merchants during the program’s first month.

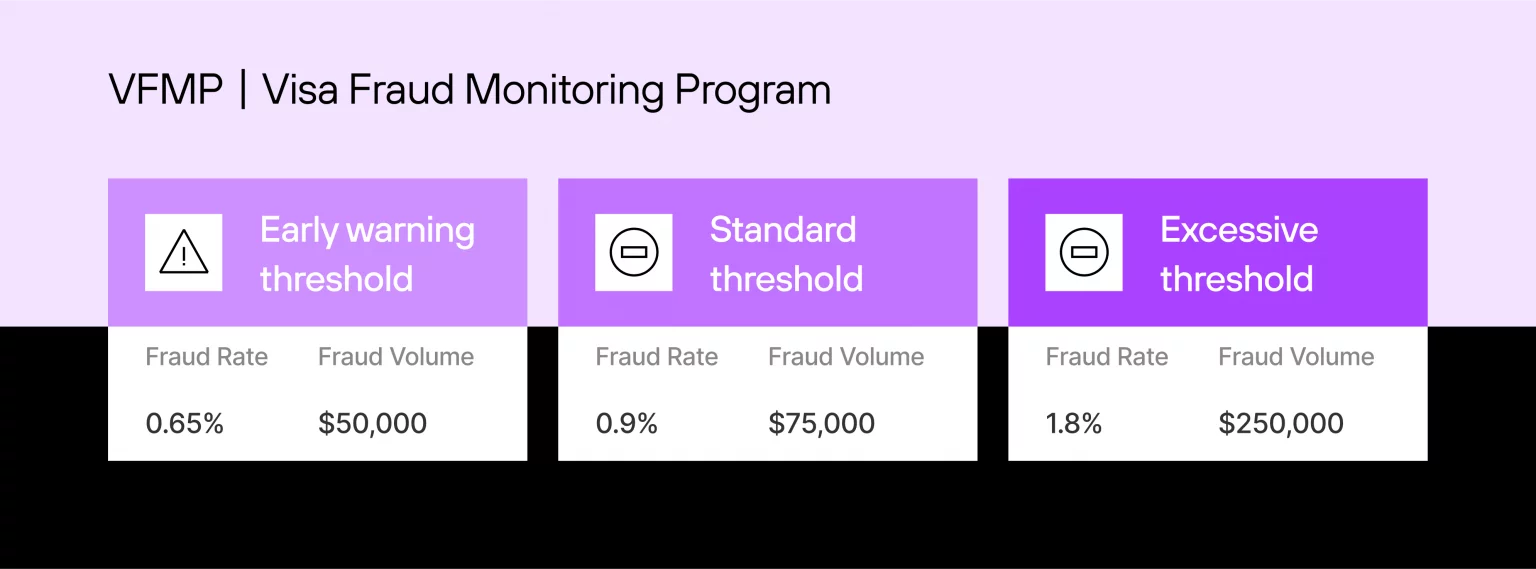

Visa Fraud Monitoring Program (VFMP)

The Visa Fraud Monitoring Program has been created for merchants to get their fraud levels under control. Visa tracks fraud-related chargebacks and TC-40 alerts to identify merchants that may be violating Visa fraud thresholds.

Merchants are placed in the VFMP if they exceed the following two criteria:

- Total USD volume of Visa transactions that were fraudulent (Fraud Volume)

- The ratio of fraudulent transactions to the total number of Visa transactions (Fraud Rate).

Unlike VDMP, Visa looks at the total USD amount of fraudulent transactions instead of the actual number of fraudulent transactions in VFMP.

An early warning may be issued to a merchant if the fraud rate exceeds 0,65% and $50,000 in fraud volume. In this case, a merchant should take corrective actions to reduce its fraud rate and avoid being placed into the monitoring program.

If the merchant exceeds the Standard or Excessive fraud thresholds outlined by Visa below, then a mitigation plan with clear corrective actions should be provided to your .

Visa can decide to put a merchant into a High-Risk threshold at any time while the merchant is in the monitoring program, which usually affects merchants with High-Risk MCCs or processing behaviors associated with elevated risk.

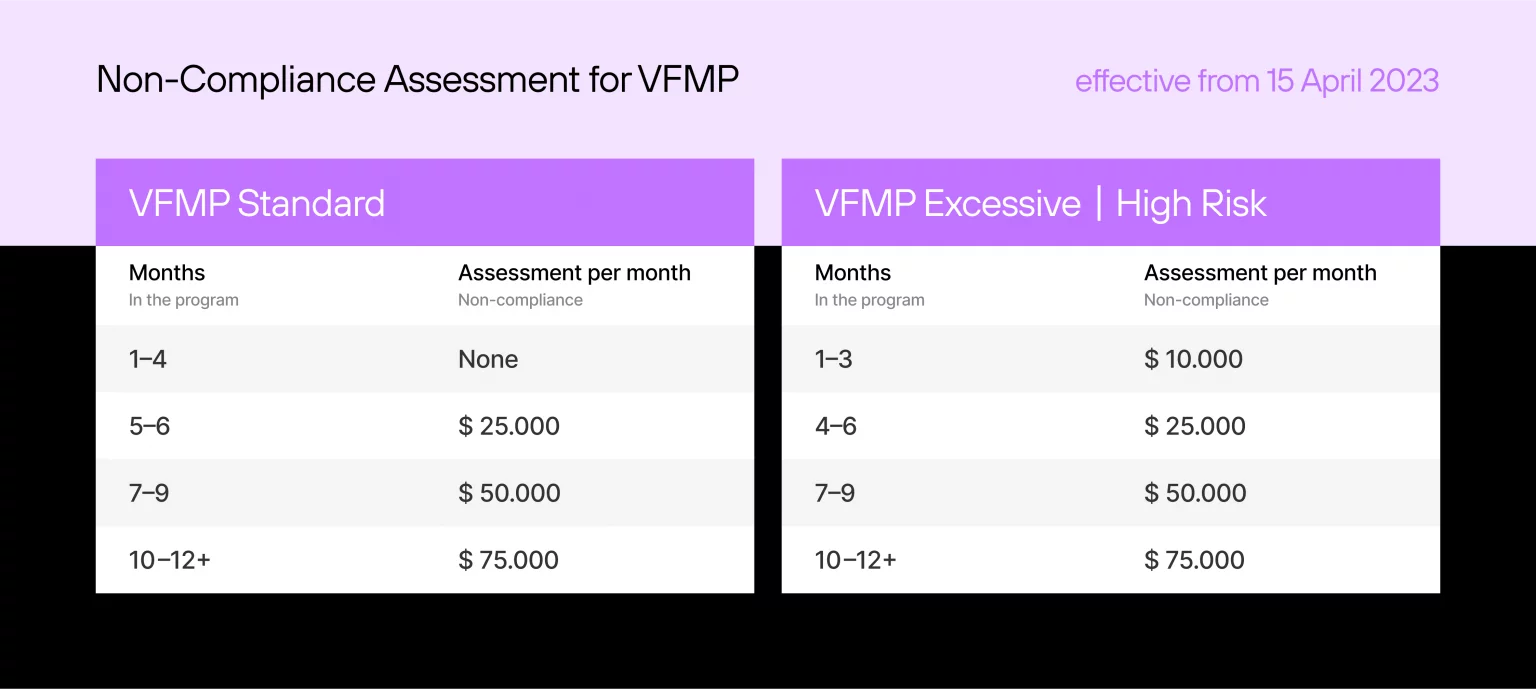

When a merchant is identified as a High-Risk or Excessive threshold, the prescribed enforcement/fines will apply until they exit the monitoring program entirely.

Even if the merchant’s fraud volume decreases to Standard thresholds at any point while being in the program, the merchant would still be viewed by Visa under the Excessive/High-Risk assessments.

Please note that being placed in the Early Warning is not a violation; hence, no fines are imposed at this stage.

At the Standard level, fines starting at $25,000 may be assessed after four months. At the Excessive/High-Risk level, fines starting at $10,000 may be assessed immediately.

Non-Compliance Assessments for VFMP effective before April 15, 2023

Non-Compliance Assessments for VFMP effective after April 15, 2023

Mastercard Fraud Monitoring Programs

Mastercard has its monitoring program when it comes to chargebacks

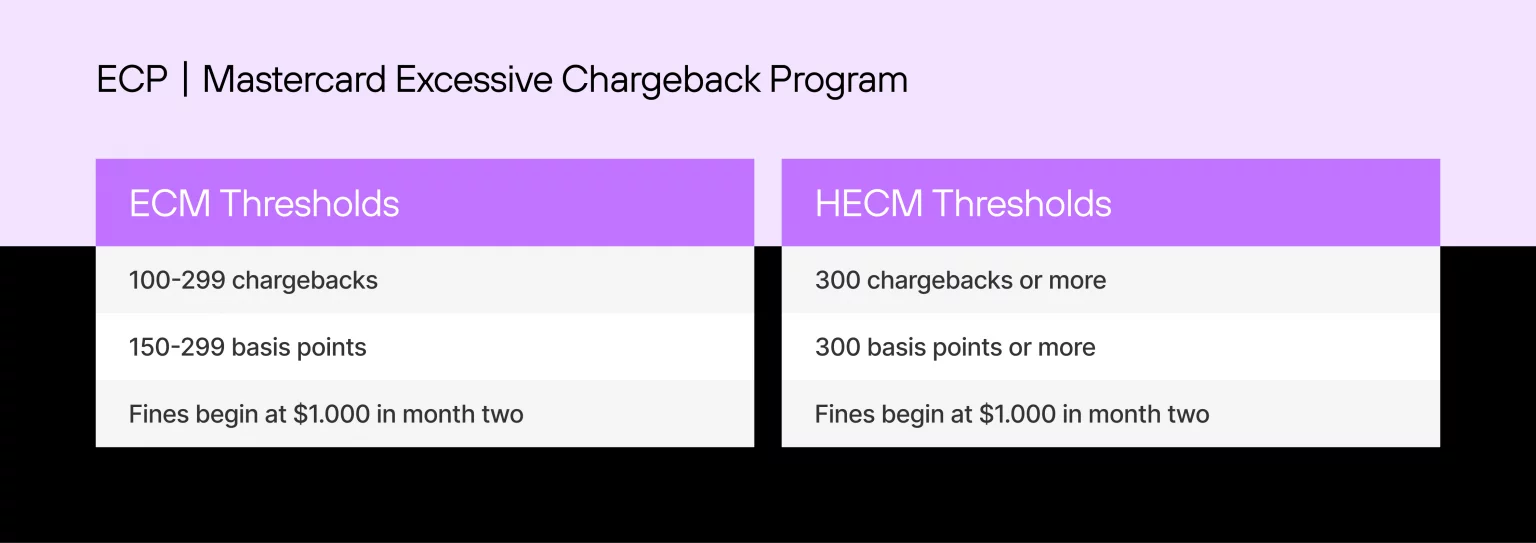

The Excessive Chargeback Program (ECP), which has two levels:

- Excessive Chargeback Merchant (ECM), and

- High Excessive Chargeback Merchant (HECM)

There is also a separate monitoring program for fraud – The Excessive Fraud Merchant (EFM) Compliance Program.

If your exceeds Mastercard’s threshold limits, you will be placed in one of the following programs. In case a merchant exceeds both ECP and EFM thresholds, Mastercard would only put such merchants into the EFM, but not the ECP.

Excessive Chargeback Program (ECP)

Merchants are placed into the Excessive Chargeback Merchant (ECM) or High Excessive Chargeback Merchant (ECM) in case they breach both of the following thresholds:

- The total number of Mastercard chargebacks over a period of a month (chargeback count)

- The ratio of chargebacks to the total number of Mastercard transactions (chargeback rate)

Unlike Visa, the chargeback rate for Mastercard (also called ) is calculated as a ratio of chargebacks submitted by cardholders in a given month to the total number of Mastercard transactions in the preceding month, multiplied by 10,000.

For example – (200 chargebacks in December / 5000 Total number of Mastercard transactions in November) x 10,000 = 400 basis points.

For both programs, non-performance assessments (fines) start when a merchant is identified in ECM or HECM for 2 months (consecutive or non-consecutive).

The penalties in Month 2 will start from $1000 and can reach up to $100,000 by Month 19. The merchant remains in the program until chargebacks or basis points fall below program thresholds for 3 consecutive months.

*Issue recovery assessment applies as an additional cost of USD 5 to the chargeback fee for each chargeback over 300 chargebacks.

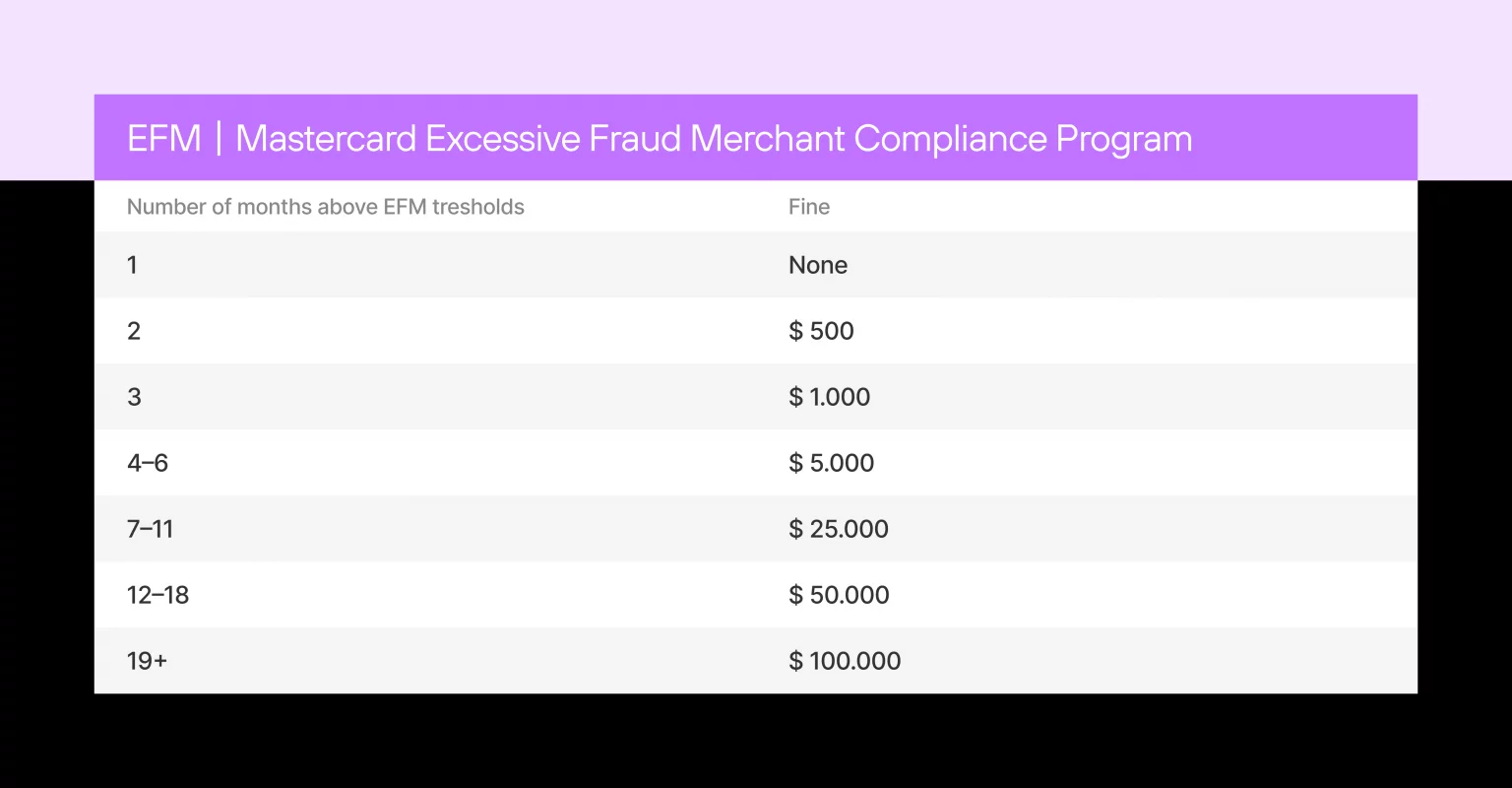

EFM: Mastercard Excessive Fraud Merchant Compliance Program

The EFM program monitors Mastercard fraud-related chargebacks from e-commerce transactions for every merchant.

Only chargebacks with the following reason code – 4837 No Cardholder Authorization would count towards the thresholds outlined by Mastercard.

Typically, chargebacks with such a reason code are filed when the cardholder has indicated that the charge for the transaction was not authorized.

A merchant is identified as an Excessive Fraud Merchant (EFM) in case all four criteria are met or exceeded:

- The merchant has at least 1,000 e-commerce transactions from the previous month in clearing.

- The amount of fraud-related chargebacks is $50,000 or over.

- Merchant has at least 50 basis points in fraud-related chargebacks.

- The merchant is located in a regulated country, and the percentage of the merchant’s clearing volume processed using 3DS is 50% or lower (3DS percentage for non-regulated countries is 10% or lower).

Similarly to ECM, the merchant’s fraud chargeback basis points are calculated using the following formula: (number of fraud-related chargebacks/number of Mastercard e-commerce transactions processed by the merchant in the preceding month) x 10,000.

Non-performance assessments start when a merchant is identified in the EFM for 2 months (consecutive or non-consecutive).

Assessment fees will increase over time if the merchant continues to be identified as EFM by Mastercard. Hence, the merchant must implement a clear performance strategy to reduce fraud.

Fraud Monitoring Programs: Conclusion

As a recap, merchants must keep their fraud levels under appropriate levels for several reasons:

- Financial losses: Fraudulent transactions can result in significant financial losses for merchants, as they may be required to cover the cost of the fraudulent transactions. If a merchant’s fraud level exceeds a certain threshold, they may be subject to higher chargeback fees or penalties from the card or scheme.

- Reputation: A high fraud level can damage a merchant’s reputation and lead to a loss of customer trust. Consumers are more likely to do business with merchants that have a good reputation for security and trustworthiness.

- Risk of termination: If a merchant’s fraud level is consistently high, they may risk losing the ability to accept card payments from a particular card scheme. This can be a significant blow to a merchant’s business, as they may lose a large portion of their customer base.

Frequently asked questions

The Visa Fraud Monitoring Program (VFMP) aims to track and manage fraud-related chargebacks for merchants. Merchants who exceed Visa's fraud thresholds, such as a high fraud volume or fraud rate, may be placed in the program and required to provide a remediation plan to reduce fraud levels and avoid penalties.

The Visa Dispute Monitoring Program (VDMP) is for merchants with a high chargeback ratio. Merchants who exceed Visa's chargeback thresholds in a given month are placed in VDMP and must take corrective action. The program has three stages: Early Warning, Standard, and Excessive, with escalating fines for merchants who do not reduce chargeback rates.

Merchants placed in Visa or Mastercard’s monitoring programs may face fines, additional fees, and the risk of losing the ability to accept card payments if they do not reduce chargeback or fraud rates within the prescribed timeframe. These programs are serious and require immediate attention and remediation.

To avoid being placed in a monitoring program, merchants should closely monitor their fraud and chargeback metrics, implement fraud prevention tools, and respond quickly to chargebacks and disputes. Regularly analyzing transaction data and setting up automated chargeback management systems can help mitigate the risk of exceeding Visa or Mastercard’s thresholds.

Common causes of chargebacks and fraud in e-commerce include unauthorized transactions, customer disputes, and fraudulent transactions. To reduce these issues, merchants should verify customer information, use secure payment gateways, and implement fraud detection tools like 3D Secure (3DS) to protect against unauthorized charges.

Yes! Merchants can exit the monitoring programs by reducing their chargeback or fraud rates below the prescribed thresholds. This process typically takes a few months of consistent improvement. Merchants must work closely with their acquiring bank to submit a remediation plan and ensure compliance with Visa or Mastercard’s guidelines.