Payment optimization: Strategies, KPIs, and tools for 2026

Payments 101

10 Apr 2026

13 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Most payment teams know their auth rates could be higher. We walk through a step-by-step payment optimization strategy – the levers that move the needle and the infrastructure to make it happen.

For a business processing $1 billion in annual transactions, a 1% increase in authorization rates equals $10 million in recovered revenue – no new customers, no extra ad spend, no pricing changes. Just fewer failed payments.

A found that subscription providers lose an average of 9% of annual revenue to failed payments – most of it involuntary. forecasts that merchant losses from online payment fraud will exceed $362 billion globally between 2023 and 2028.

The math is clear: you can put more money in the bank by optimizing your payments than by launching another acquisition campaign.

This guide condenses what we've learned building payment infrastructure for hundreds of digital businesses at Solidgate – covering what payment optimization includes, how to build a payment strategy, which KPIs to track, and where AI is changing the game.

TL;DR

- Payment optimization covers four areas that follow the transaction lifecycle: conversion (checkout experience, local payment methods), authorization (smart routing, local acquiring, adaptive 3DS, network tokenization), cost (least-cost routing, reconciliation, fraud reduction), and revenue recovery (smart retries, credential updates, dunning).

- Most payment teams already know what to optimize. The gap is infrastructure: single-provider dependency, inconsistent data across PSPs, and engineering bottlenecks that delay every change. A unified orchestration layer closes all three.

- AI adds the most value at specific decision points – fraud scoring before the transaction, smart retries and routing during it, and dispute automation after.

- This guide walks through each area, the blockers that stall progress, how Solidgate addresses them, and which KPIs to track.

What is payment optimization?

Payment optimization is the process of improving every step in the transaction lifecycle – from checkout through authorization, settlement, and recovery – to increase the percentage of successful payments while reducing cost and fraud.

Payment process optimization ranges from small changes like reordering payment methods at checkout or adjusting 3DS thresholds to structural upgrades like adding acquirers, setting up dynamic routing, or implementing network tokenization.

What you prioritize will depend on your business model and where you process.

Core areas of payment optimization

Payment optimization strategies map to four outcomes that follow the transaction lifecycle: earn the transaction, get it approved, pay less for it, and recover it when it fails.

Optimizing for conversion

Before a payment can succeed, a customer has to attempt it. Conversion optimization is everything that happens before the "pay" button gets pressed.

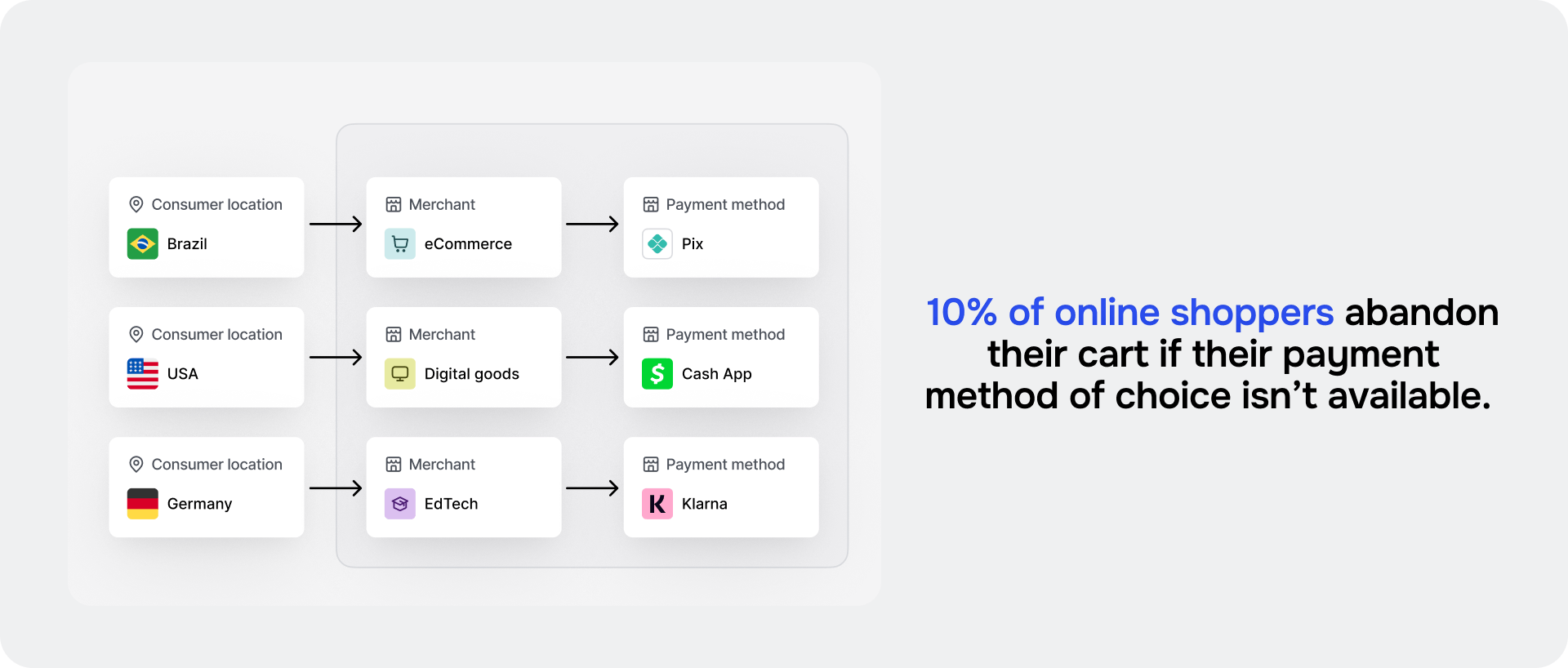

The most direct lever to raise conversion rates and boost customer trust is payment method optimization. A found that, in 2026, the average online shopping cart abandonment rate was 70.22%, with 10% citing a lack of preferred payment methods as the reason.

If customers' preferred payment options aren't available – PIX in Brazil, iDEAL in the Netherlands, BLIK in Poland, UPI in India – the transaction either fails or never starts. These are the dominant ways people pay in those markets, and offering only international card networks leaves significant conversion on the table.

Smooth checkout experience matters, too:

- Auto-adjusting language and currency

- Pre-populating fields for returning customers

- Validating card data in real time

These are small changes that add up at scale.

Optimizing for authorization

Authorization is where most revenue leaks hide. A customer wants to pay, your checkout worked, but the transaction still can fail:

- An issuing bank declines it

- A fraud filter blocks it

- Your provider has an outage

There are different tools and strategies you can use to address each problem. Key levers include:

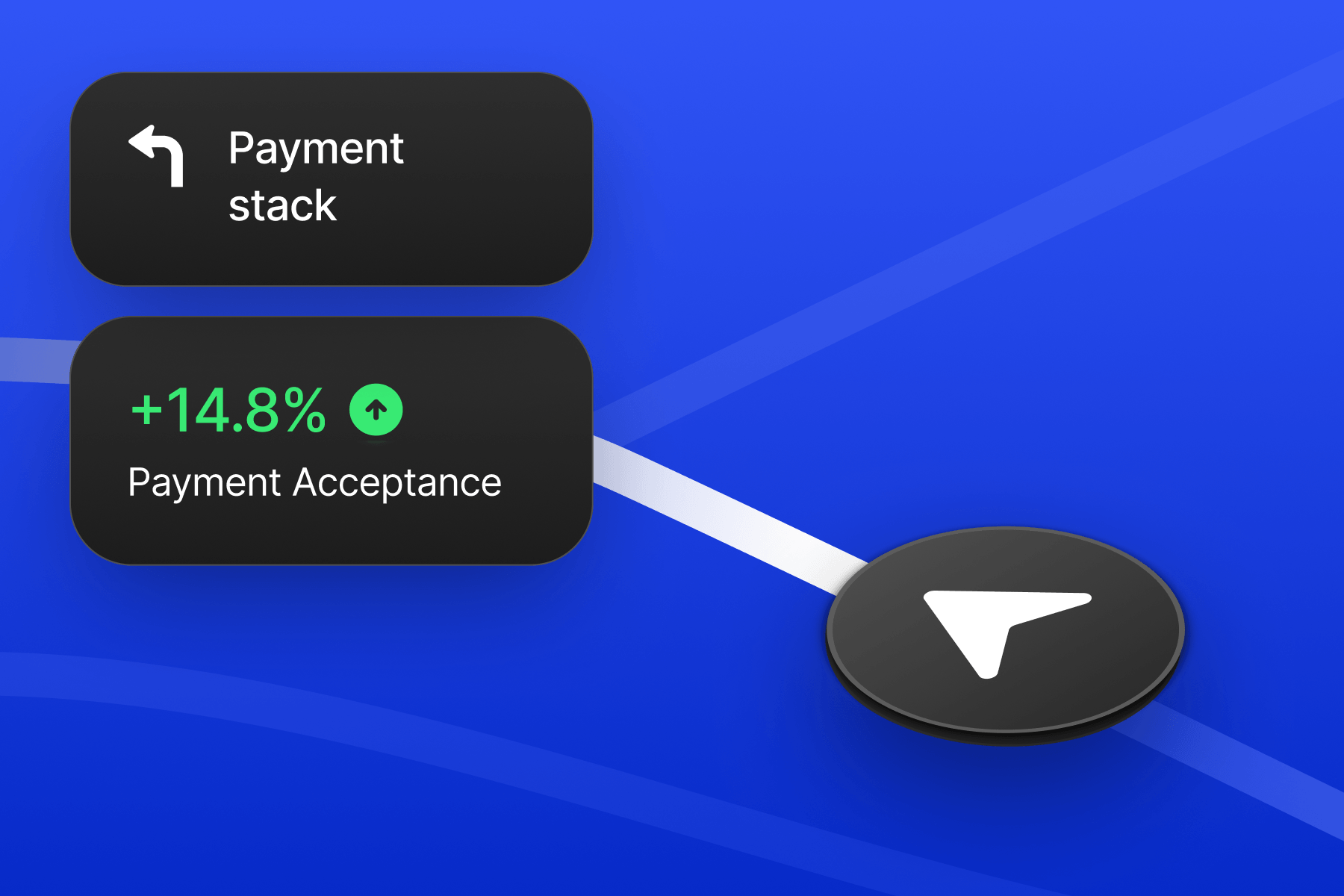

Build redundancy: A business with millions of customers can’t rely on just one provider for an entire region. That’s why it’s important to have a backup processor you can always fall back on.

At Solidgate, for example, payment cascading – using acquirer fallbacks and dynamic routing to recover failed payments – helps drive an average 14.8% increase in acceptance.

Increase issuer trust: This requires work on a few fronts simultaneously.

First, work with local partners. Expanding your acquiring relationships is one of the most direct ways to reduce . Local issuers approve domestic transactions at significantly higher rates than cross-border ones — our benchmarks show an average 17.9% lift from local acquiring alone.

Second, use network tokens and adaptive authentication. Network tokens replace raw card numbers with scheme-issued credentials that issuers trust more.

Adaptive 3DS and Strong Customer Authentication (SCA) exemptions add friction only when the risk profile warrants it. It preserves a clean experience for low-risk transactions while boosting issuer confidence on flagged ones.

Optimizing for cost

Cost optimization is always on the payments teams’ agenda, which includes optimizing the economics of each transaction, including interchange fees, processing costs, and operational overhead.

A few strategies that target cost optimization include:

- Least-cost routing: Directing payments to the provider with the lowest fees that still meets your authorization rate threshold. Over time, this logic reduces blended interchange and processing costs without sacrificing performance.

- Improving internal operations: This typically includes automated reconciliation that affects cost, though less visibly. Centralizing reporting across acquirers and payment providers cuts hours of manual work and surfaces discrepancies faster.

- Reducing fraud and chargebacks: High dispute rates carry direct costs – chargeback fees, scheme fines, and elevated processing rates from card networks. Strong fraud prevention and clear billing descriptors reduce disputes at the source, protecting both margin and your standing with acquirers.

Optimizing for revenue recovery

For subscription and recurring-revenue businesses, the transaction lifecycle doesn't end at the first authorization. Cards expire, funds run short temporarily, issuers flag renewals – each of these triggers involuntary churn, which accounts for up to in some verticals.

The recovery toolkit includes smart retries timed to issuer behavior, automatic credential updates when cards are reissued, and dunning sequences that give customers every opportunity to stay before a subscription cancels.

Key takeaway: These four areas – conversion, authorization, cost, and recovery – follow the transaction lifecycle and reinforce each other.

Why payment optimization stalls at scale

From thousands of conversations we had with payment leads, it’s clear that most payment teams don't lack ideas for what to optimize. The biggest blocker is the lack of infrastructure to act on them. As a business scales, three structural problems tend to surface.

Single-provider dependency

Many businesses start with one PSP and build their around it. Then, authorization rates plateau in certain corridors, routing options are limited to what the provider offers, and negotiating leverage is low when all your volume flows through one partner.

Adding a second or third acquirer helps, but only if your infrastructure can actually orchestrate across them.

Inconsistent data across providers

Each payment service provider (PSP) has its own decline codes, reporting formats, and settlement timelines. Data sits in separate provider dashboards, your team reconciles manually, and decline rates come back without enough context to act on.

For most businesses, the starting point is the same: no unified view across these dimensions. The goal is baseline visibility, so you can measure what actually changes when you start to optimize payment performance.

Engineering bottlenecks

Adding a new payment method, adjusting payment flow rules, implementing network tokenization, and testing a retry strategy – each of these requires a dev cycle. For most mid-market businesses, the payment team doesn't have dedicated developers. They compete for sprint capacity with product features, and optimization work gets deprioritized.

More and more businesses are navigating this by shifting to a modular, composable approach: a unified infrastructure layer that helps them optimize payment infrastructure from one place – connecting the rails underneath.

KPIs for payment performance optimization

The table below covers the core metrics every payment team should track and how they relate to specific actions.

| KPI | What it tells you | How to act on it |

| Authorization rate | Transaction success, segmented by provider, region, and card type | Identify decline clusters; adjust routing or retry logic |

| Payment method success rate | How each method performs across your customer base | Prioritize methods with higher approval rates in specific markets |

| Blended transaction cost | Processing cost per transaction across providers | Route transactions toward lower-cost providers that meet your auth rate threshold |

| Chargeback ratio | Dispute rate by reason code | Target fraud tooling or descriptor clarity at the root cause |

| Failed payment recovery rate | Share of declined subscription payments recovered | Review retry timing, dunning sequences, and card updater coverage |

| False positive rate | Legitimate transactions blocked by fraud filters | Recalibrate fraud thresholds if good customers are getting declined |

| Network token adoption rate | Percentage of stored credentials using VTS/MDES tokens | Push token migration for recurring payments to improve retention |

Key takeaway: Track these KPIs segmented, not blended. A 90% blended authorization rate can mask a 70% rate in your fastest-growing market – and that's where the revenue upside lives.

How Solidgate helps you with payment optimization

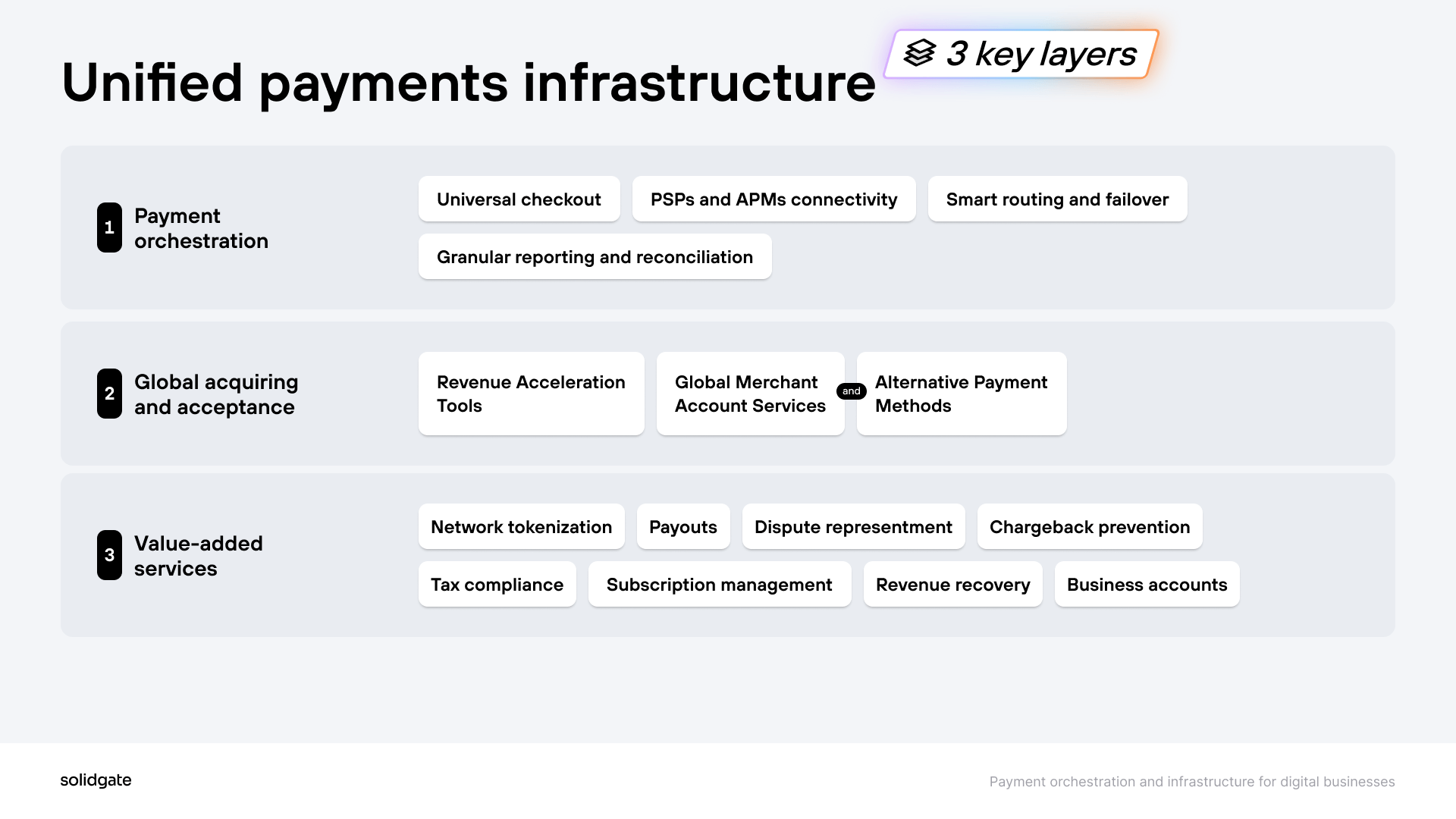

Solidgate is a global payment orchestration and infrastructure platform that gives payments leaders the tools to turn payments from a cost center into a revenue-generating lever.

We strip the payments function of its growing complexity, helping scaling businesses unlock new opportunities and optimize every aspect of payments.

Here is how teams see the fastest ROI from Solidgate.

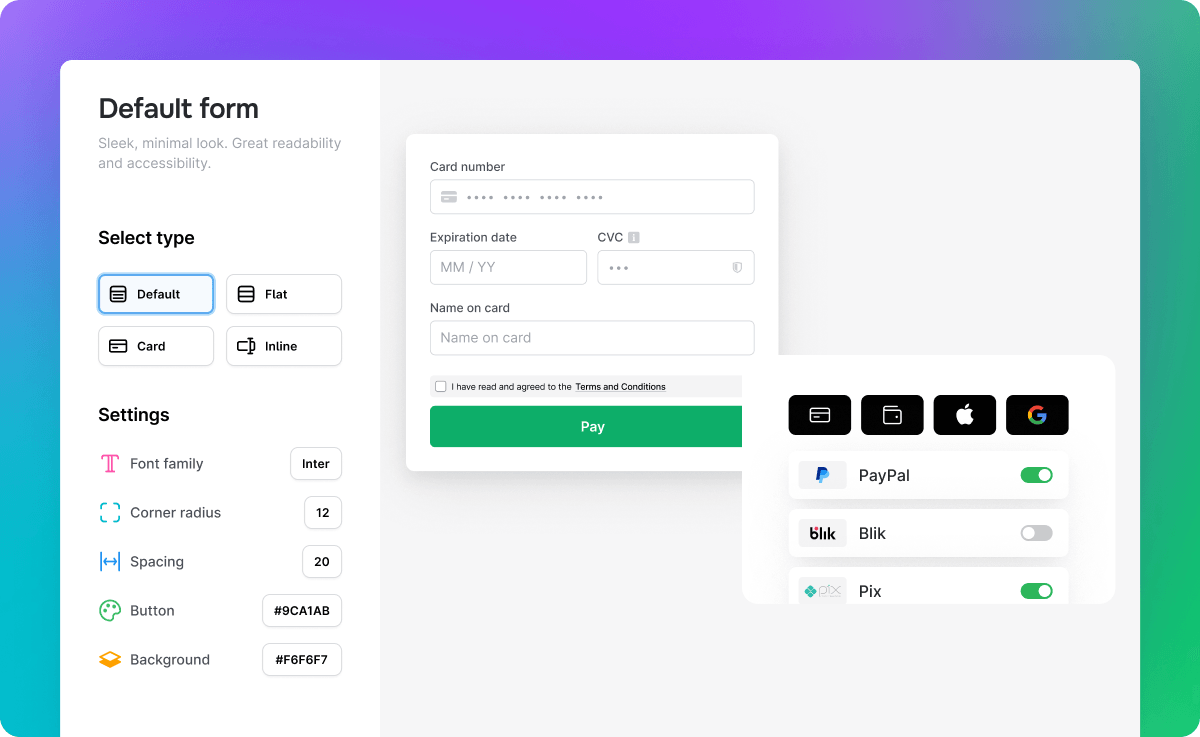

Improving conversion: localized checkout in minutes

Say you want to scale to Portugal and need to add MB WAY to your stack and test various checkout flows. The typical path without orchestration: spend months on integration and maintenance, then hit a wall with customization options on a hosted PSP page.

Solidgate gives you out-of-the-box access to dozens of the most popular local and across 15 markets alongside card networks, Apple Pay, Google Pay, and PayPal. Adding a new method is as simple as switching it on through the admin panel.

You can also build your checkout using customizable that auto-adjust language, currency, and preferred payment methods based on the customer's location.

A shopper in Sweden sees Swish, a customer in Brazil sees PIX, and a buyer in the Netherlands sees iDEAL, without your team configuring each market manually.

For businesses that need to collect payments without a full checkout flow, let you generate shareable, branded payment URLs with no code required.

Improving authorization: self-serve routing, tokenization, acquiring, and fraud prevention

This is where Solidgate does the heaviest lifting, giving you access to every tool you need:

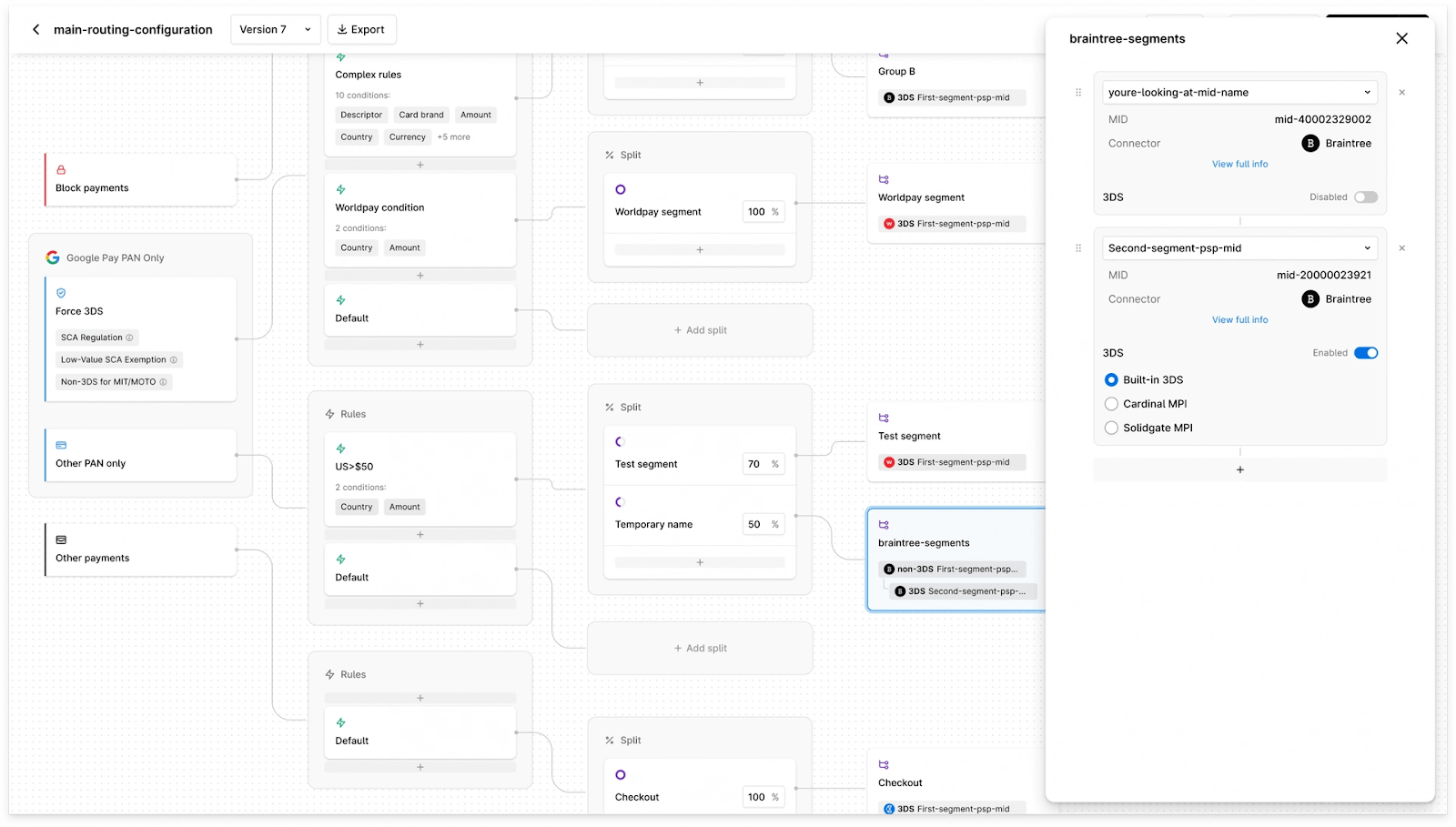

No-code smart routing

Our engine allows you to direct each transaction across to the ones with the highest approval probability, with automatic cascading to fallback providers when the primary path fails.

Your payment team can configure and adjust routing rules directly in the Solidgate Hub – no developers needed. Use pre-built templates, version control, and one-click rollback to A/B test new routing logic, validate results, and scale or revert in minutes.

It puts routing control in the hands of the people who understand the data best: your payment and finance teams.

Card acquiring across 15+ markets

Cross-border transactions fail at higher rates because foreign issuers are less likely to approve them. allows you to start processing payments through the best local acquirers in as little as one day.

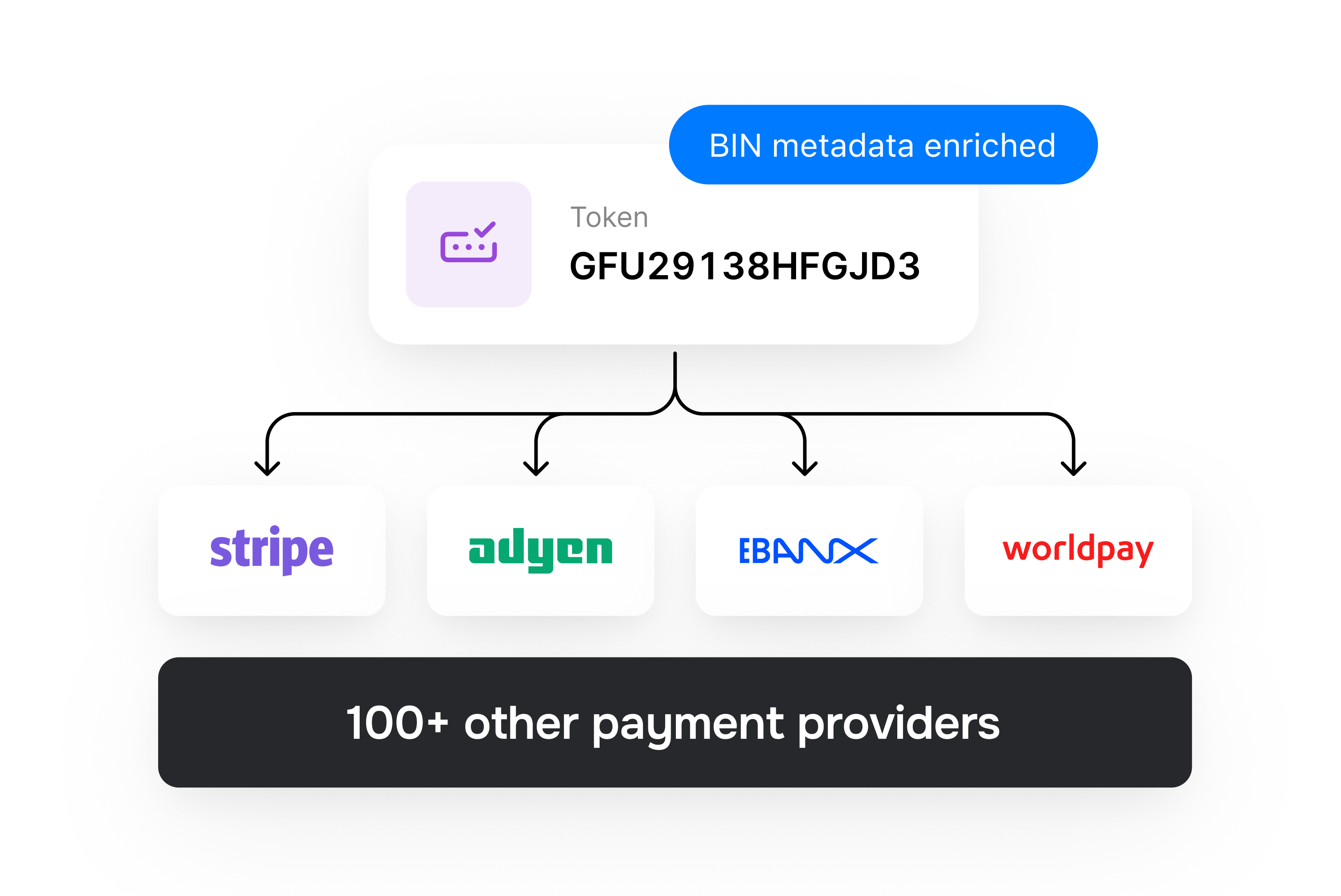

Network tokenization and token vault

Solidgate's stores payment credentials centrally, independent of any single provider. Adding or switching acquirers doesn't mean losing stored cards or triggering re-authorization failures.

On top of the vault, network tokenization via VTS and MDES replaces raw card numbers with issuer-generated tokens that carry stronger security signals.

Issuers approve tokenized transactions at higher rates – we see an up to 4.4% boost in approval rate. Network tokens also survive card reissues automatically, delivering 7.5% higher retention for subscription businesses by keeping billing continuity intact.

Authentication strategy optimization

3DS and SCA aren't just compliance checkboxes. Applied well, they lift authorization rates by increasing issuer confidence; applied bluntly, they kill conversion.

Solidgate gives you control over when and how authentication is triggered: force 3DS on high-risk transactions, apply SCA exemptions on low-value or low-risk payments, and use frictionless 3DS2 flows where issuer and cardholder data support it.

The routing engine handles this logic per transaction, so you're not choosing between security and conversion, but rather calibrating the balance per corridor.

Check to see how we helped streaming service MEGOGO optimize its 3DS authentication flows and boost payment conversion by 3,5%.

Antifraud that doesn't over-block

Every legitimate transaction your fraud filters block is revenue lost. Solidgate's uses ML-based scoring to evaluate device fingerprints, behavioral signals, and transaction context in real time. This allows for blocking fraudulent transactions that rule-based systems miss, while blocking fewer legitimate customers.

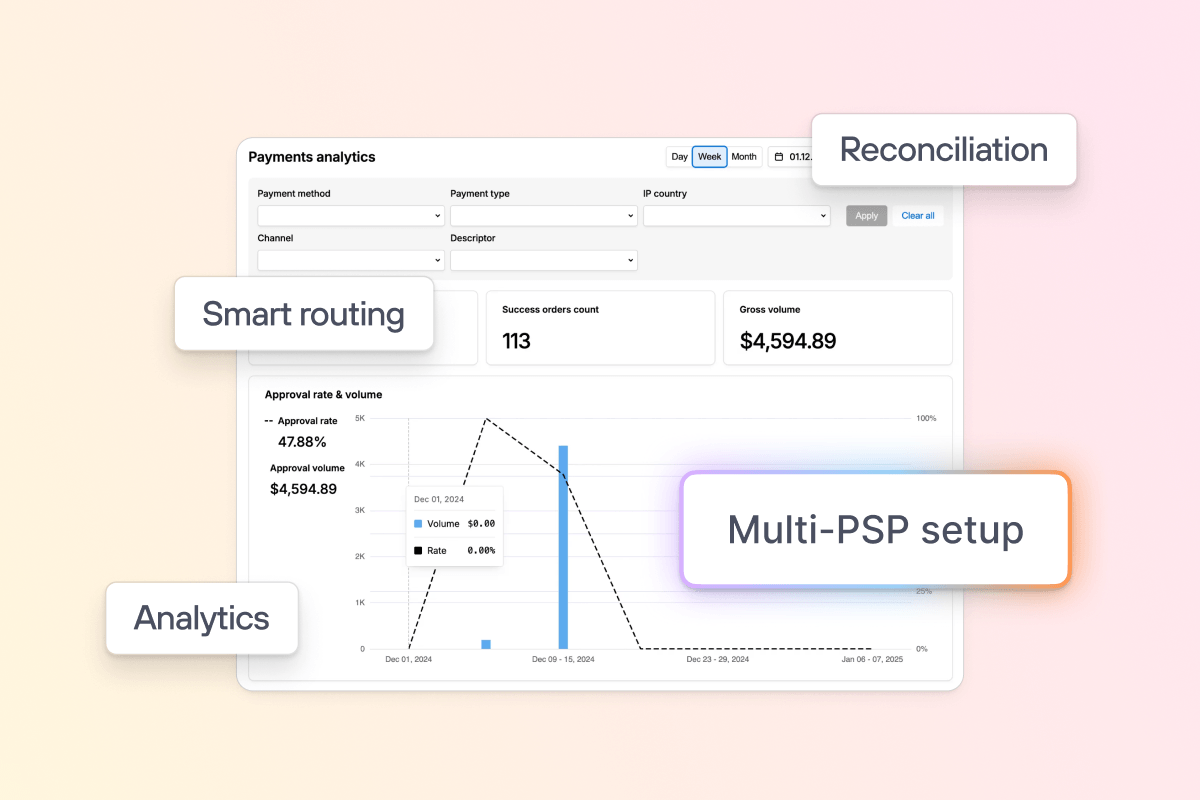

Improving cost: least-cost routing and centralized reconciliation

A common scenario: you're processing through three acquirers, but all your European volume defaults to one, because the routing was set up at launch and nobody's revisited it.

Meanwhile, your second acquirer offers lower on domestic transactions in two of your top markets. You suspect you're overpaying, but proving it requires pulling reports from three dashboards and reconciling them in a spreadsheet.

Solidgate's solves both sides. You can set rules that direct transactions to the most cost-efficient acquirer that still meets your authorization threshold. Adjust the logic in the Hub, measure the cost reduction, and iterate without touching code.

On the operations side, Solidgate centralizes across all your payment providers into a single reporting layer. Payment costs and acquirer fees are fully visible via API and the Hub admin panel, so your finance team gets one source of truth instead of four.

Revenue recovery: smart retries, billing continuity, and dunning

For subscription merchants, Solidgate's recovery stack targets every major cause of involuntary churn. Our re-attempt charges based on issuer behavior and cardholder time zones, recovering payments that a fixed schedule would miss.

and network tokenization automatically keep credentials current, so a reissued card doesn't become a lost subscriber.

In-built handles the full billing lifecycle: trials, custom billing frequencies, tiered pricing, upgrades, and coupons. Dunning sequences include dynamic discounting during retries and smart cancellation logic that pauses subscriptions on hard declines rather than canceling them outright.

The result is fewer unnecessary cancellations and more revenue retained.

AI in payment optimization

AI in payments delivers the most value at decision points where speed and pattern recognition exceed what a human team can do. In practice, AI applies at specific points across the payment lifecycle rather than as a single monolithic system.

Before the transaction

Payment infrastructure integration: AI is now changing how businesses integrate payment infrastructure in the first place.

For example, Solidgate recently released AI Skills for Payment Integration – structured documentation and code examples optimized for LLM tools like Claude, ChatGPT, and Cursor. A developer drops a skill file into their AI coding assistant and gets a working integration in minutes instead of hours spent reading API docs.

It's a small example of how AI reduces operational overhead beyond the transaction itself.

Fraud scoring and risk decisioning: ML models evaluate device fingerprints, behavioral patterns, velocity checks, and transaction context simultaneously. It catches fraud patterns that static rule sets miss while producing fewer false positives.

During the transaction

ML-driven routing: Some orchestration platforms are beginning to apply ML to routing decisions. It predicts which provider will deliver the highest approval probability for each transaction based on historical patterns.

Smart retries: Instead of retrying failed payments on a fixed schedule, ML identifies the best retry window based on issuer behavior, decline reason codes, and cardholder time zones.

After the transaction

Dispute representment and operational automation: AI drafts chargeback responses by assembling transaction evidence, matching it to reason codes, and generating structured representment cases. It also handles tasks like invoice and evidence translation for cross-border compliance.

These aren't flashy use cases, but they save payment and finance teams hours of manual work per week.

Payment performance as a revenue discipline

Payment performance optimization increases captured revenue, reduces customer frustration, cuts fraud losses, and builds the infrastructure foundation your business needs to grow globally or expand into new billing models.

Most payment teams we talk to already know what they should be doing:

- Adding local acquiring and AMPs

- Optimizing 3DS and SCA

- Routing smarter

- Retrying at the right time

- Tokenizing stored credentials

The biggest gap is the infrastructure. When your data lives across four provider dashboards, your tokens are locked to a single processor, and every routing change or APM integration requires a dev ticket, the optimization work stalls regardless of how good your strategy is.

Solidgate's payment infrastructure is built for exactly this – one platform that wires together orchestration, acquiring, fraud prevention, and subscription management so your team can focus on outcomes instead of plumbing.

Want to benchmark your current payment setup? to map your setup and identify where performance gains are available.

Frequently asked questions

Payment optimization is the practice of improving every step in the transaction lifecycle – from checkout through authorization, settlement, and recovery – to increase the share of successful transactions while reducing cost and fraud. It covers routing, payment method coverage, fraud calibration, tokenization, and retry strategies.

Payment optimization strategies directly protect revenue that's already flowing through your business. Without it, failed transactions, unnecessary payment declines, and high processing costs silently erode margin. For subscription businesses, even a small improvement in authorization rates reduces involuntary churn and strengthens monthly recurring revenue (MRR) without additional acquisition spend.

Start by auditing your current authorization rates, decline patterns, and processing costs segmented by provider and region. Then add an orchestration layer that enables dynamic routing, centralized tokenization, and multi-provider failover. Track KPIs weekly, calibrate fraud thresholds to reduce false positives, and test routing changes through A/B experiments before scaling them.

The highest-impact moves are smart routing (directing each transaction to the best-performing provider), local acquiring (processing domestically to lift approval rates), network tokenization (improving issuer trust and billing continuity), and smart retry logic (recovering failed payments at the right moment). Combined, these tactics regularly deliver double-digit percentage gains in recovered revenue.

The most common mistake is treating payments as a fixed cost rather than a performance variable – relying on one provider with no dynamic routing, no retry logic, and no benchmarking. A close second is miscalibrating fraud filters: thresholds too tight block good customers; too loose and fraud eats your margin. Many teams also skip data segmentation, so a blended authorization rate masks significant variance by region, card type, or issuer.