How to reduce payment processing costs: 8 proven strategies

Payments 101

Updated 27 Jul 2026

9 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Here's what actually moves your effective processing rate – and what doesn't.

Processing fees grow with volume. The fee line on your P&L scales with every new market you enter and every cross-border transaction your current setup isn't optimized for.

Most merchants know their effective processing rate. Fewer know which part of it is fixed and which part they're overpaying on. That distinction determines what's worth acting on.

This guide covers the 8 ways to reduce payment processing costs and how to prioritize them based on your current setup.

TL;DR

- Payment processing fees come from three places – card networks (interchange, assessment, and cross-border fees), your processor (markup, gateway, chargeback fees), and how your stack is configured (interchange downgrades, excess retry costs). Each has a different lever.

- Intelligent routing sends each transaction through the lowest-cost path. Combined with payment cascading, it recovers both cost and approval rate across your acquirer setup.

- Local acquiring removes cross-border fees. Correct MCC and authorization data prevents interchange downgrades that happen automatically when data is incomplete.

- Smart retries, fraud prevention, and network tokenization each cut a different avoidable cost – failed renewals, chargeback fees, and stale credentials respectively.

- Prioritization depends on your setup: a single-market, single-acquirer merchant starts differently than one running multiple acquirers across borders.

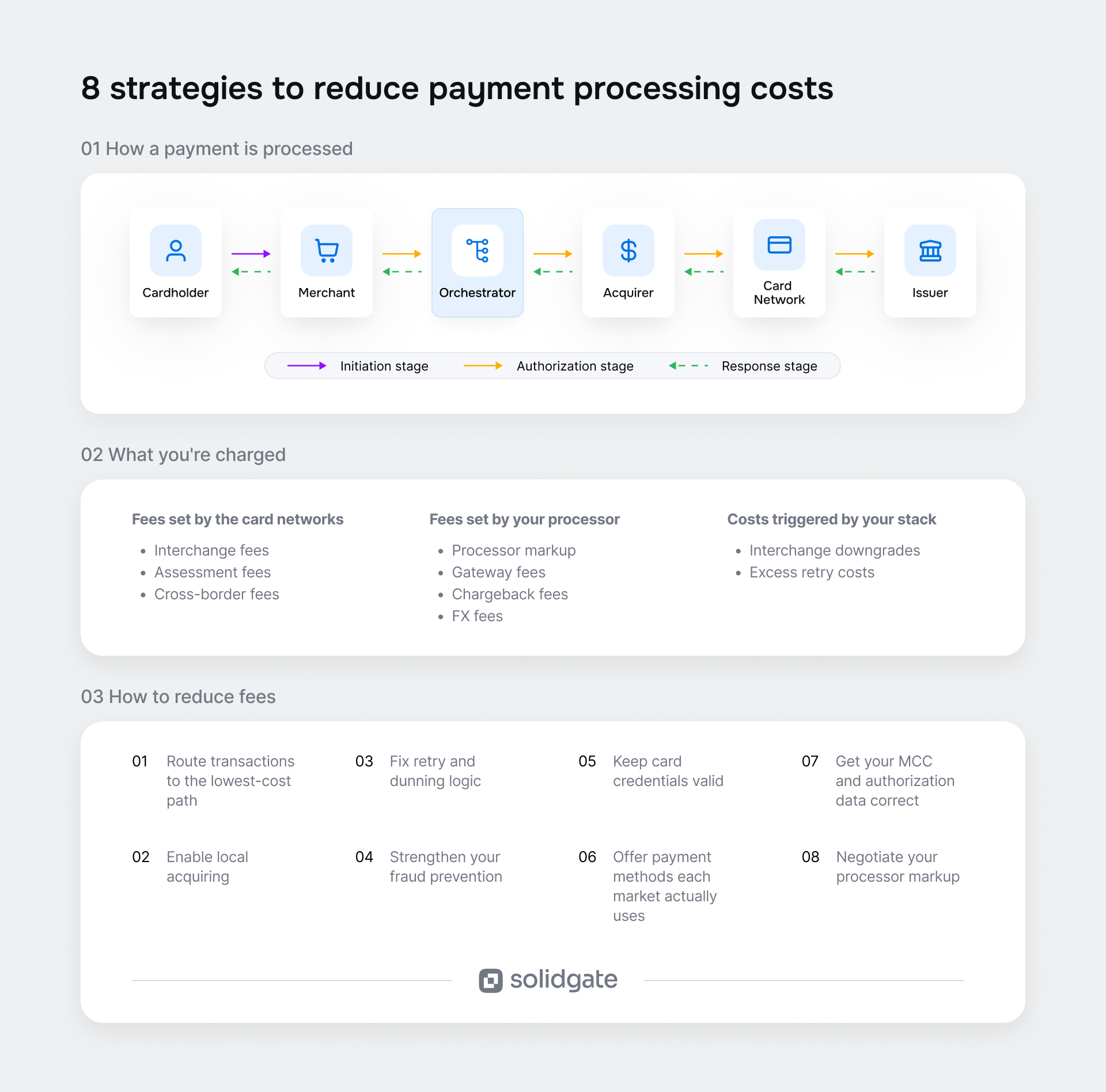

What makes up your payment processing costs

Every time a card transaction goes through, multiple parties take a cut. The total you see as your effective rate is the sum of several distinct fees – some fixed by the card networks, some set by your processor, some triggered by how your stack is configured. Below are the most common ones, grouped by who controls them.

Fees set by the card networks

These apply the same way regardless of which processor or acquirer you use. You can't negotiate them away, but you can avoid paying more than the minimum by qualifying transactions correctly.

Interchange is a fee paid by your acquiring bank to the card-issuing bank on every transaction, then passed on to you as part of your processing cost. It's the largest single component of what you pay to accept cards.

Visa and Mastercard set interchange rates by:

- Card type

- Merchant category code (MCC)

- Transaction type

A merchant based in Germany sells €500 worth of software subscriptions online. A customer pays with an EU-issued consumer credit card – interchange is capped at 0.30%, so the merchant pays €1.50. The same purchase from a customer with a non-EU-issued credit card runs at 1.50% under – €7.50 on the same transaction.

For a full breakdown of how interchange tiers work and what qualifies for each, see our guide to.

Assessment fees (also called scheme fees) are charges paid directly to the card network – Visa or Mastercard – for use of their payment rails. They're separate from interchange, fixed, and non-negotiable. Visa and Mastercard publish their assessment fee schedules independently from interchange rates.

Cross-border fees apply when your acquiring bank and the card-issuing bank are in different countries. Both Visa and Mastercard charge these on top of standard interchange and assessment fees. They apply even when no currency conversion is involved – the fee triggers from the country mismatch alone.

Fees set by the processors

These vary by provider and are the part of your cost stack that's open to negotiation or replacement.

Processor markup is what your payment processor charges for handling the transaction. It's the only component set independently by your processor, which makes it the only line item you can negotiate directly.

Gateway fees cover the transmission of payment data between parties. They're sometimes bundled into the processor markup, sometimes charged separately per transaction.

Chargeback fees are charged per dispute, regardless of whether the dispute is won or lost. Rates vary widely by processor.

FX fees apply when a transaction involves currency conversion. This is separate from cross-border fees – it's an additional charge specifically for converting one currency to another.

Costs triggered by how your stack is configured

These aren't separate fee categories – they're higher rates or additional charges that appear because of how transactions are processed.

Interchange downgrades are the most common hidden cost. When a transaction fails to meet qualification requirements – missing Address Verification Service (AVS) data, missing Card Verification Value (CVV), incorrect MCC, or late settlement – it automatically moves to a higher interchange tier. No fraud involved, no negotiation possible. The difference between a qualifying rate and a Non-Qualified rate on a single transaction can be more than 1.5 percentage points.

Excess retry costs apply when a merchant exceeds the card networks' retry limits on declined transactions. Both Visa and Mastercard cap the number of retry attempts within a given time window. Exceeding that cap wastes attempts and can attract network scrutiny.

For a full walkthrough of how a transaction moves from authorization to settlement, see.

Core insight: Payment processing costs are a stack of distinct fees from different parties, each with a different lever. The card networks fix interchange, assessment, and cross-border fees. Your processor sets the markup. Everything else is a function of how your stack is configured – and that's where most of the controllable cost sits.

8 ways to reduce payment processing costs

Route transactions to the lowest-cost path

By default, most merchants route every transaction through one acquirer – whichever was set up first. That means every transaction goes down the same path regardless of whether it's the cheapest option for that card type, currency, or geography.

changes that. When a merchant connects to multiple acquirers, each transaction is evaluated before it's sent – which acquirer charges less for this card type, this market, this transaction value – and routed accordingly. A transaction that would have gone down a more expensive default path gets sent through the cheaper one instead.

Cascading works alongside smart routing: when a transaction fails at the first acquirer, it retries through a backup automatically. Payment cascades alone contribute +14.8% to lifetime value (LTV) across Solidgate merchants.

Enable local acquiring to cut cross-border and FX costs

on local rails eliminates the cross-border fees that stack on top of interchange when your acquiring bank and the card-issuing bank sit in different countries. The transaction processes as domestic.

This applies even when no currency conversion is involved. Cross-border fees trigger from the acquirer-issuer country mismatch alone, not from the currency difference. For a merchant processing significant volume across multiple markets, that's a direct reduction on every transaction in those markets.

Local acquiring also improves approval rates. Local issuers treat transactions from a domestic acquirer with less default risk than foreign-looking ones, which reduces soft declines on every billing cycle. Across Solidgate merchants, local acquiring contributes +17.9% LTV.

Fix retry and dunning logic

A soft decline is a temporary payment failure – a card has insufficient funds at the moment of charge, the issuer's system is down, or a velocity check trips on a renewal pattern. The transaction can succeed if retried under different conditions.

The problem is timing. Retrying immediately after a soft decline, or on a fixed schedule regardless of decline reason, wastes the attempt. Card networks cap how many retries a merchant gets within a given window, so a wasted attempt is a lost one.

Smart retry logic that reads the decline reason and adjusts the next attempt accordingly recovers a higher rate of failed renewals. can reduce wrong-time retry attempts by 42.1%.

For subscription businesses, with built-in retry intelligence handles the timing decision on every renewal without manual configuration.

Strengthen your fraud prevention

When a fraudulent transaction gets through, the merchant loses the goods or service delivered and pays a chargeback fee on top – regardless of whether the dispute is won. Dispute and fraud ratios that climb above network thresholds push a merchant into a worse risk category with their acquirer, affecting pricing on every future transaction.

To improve your , start with enabling 3D Secure (3DS) authentication. It shifts chargeback liability to the card issuer when the cardholder is authenticated, removing that cost from the merchant entirely. Add pre-authorization risk scoring to block high-risk transactions before they're submitted. And review chargeback sources and fraud patterns regularly to keep your rules calibrated as fraud tactics change.

Keep card credentials valid with network tokenization

Without tokenization, a reissued card can end up as a failed renewal.

Network tokenization replaces a raw card number with a token – issued by Visa or Mastercard and automatically updated when the underlying card is reissued. The renewal processes without interruption, with no action needed from the merchant or the cardholder.

Across Solidgate merchants, network tokenization delivers up to +15% acceptance rate improvement compared to non-tokenized transactions.

If you're running a multi-provider stack, storing tokens in a PCI-compliant adds portability on top. The token lives independently of any single payment service provider (PSP) – so it can be routed across providers without asking customers to re-enter their card details.

Solidgate merchants see 27% fewer failed payments from keeping tokens updated this way.

Offer payment methods each market actually uses

shows that 10% of shoppers abandon checkout because their preferred payment method isn't available.

let you match acceptance to what shoppers in each market already use, reaching customers who prefer local payment methods and reducing card-processing cost where local alternatives are cheaper.

Many APMs settle at lower transaction cost than card acceptance in their home markets, since they run on local rails designed for domestic volume rather than international card network infrastructure.

Get your MCC and authorization data correct

An incorrect MCC or incomplete authorization data triggers an automatic interchange downgrade – the transaction moves to a higher-cost tier with no fraud involved and no negotiation possible.

For example, under , a transaction that fails to meet qualification requirements drops to the Non-Qualified rate of 3.15% + $0.10 – roughly double a qualifying e-commerce rate. The downgrade mechanic works the same way across regions.

Missing AVS data, CVV, or settling outside the required window all trigger the same downgrade. Both are operational fixes – verify your MCC reflects what your business actually does, and ensure authorization data is complete and submitted on time.

Negotiate your processor markup

The processor markup is the only component your processor sets independently, which makes it the only line item open to negotiation.

Negotiation requires comparison data. A merchant running a single processor has no benchmark and no leverage. Visibility into what each route costs per transaction is what gives merchants the data to reduce transaction costs and negotiate from a position of strength.

Core insight: To reduce payment processing fees, route transactions to the lowest-cost path, enable local acquiring, fix retry logic, improve fraud prevention, implement network tokenization, offer local payment methods, correct your MCC and authorization data, and negotiate your processor markup.

Where to start: Prioritizing the 8 levers

The right starting point depends on how your payment stack is set up today.

If you're running a single acquirer in one market, start with the levers that work inside your current setup: 3DS and risk scoring, network tokenization, and smart retries.

If you're already running multiple acquirers, routing, retry optimization, processor negotiation, and MCC alignment across providers become actionable. You have the comparison data to negotiate from and the infrastructure to route around expensive or underperforming paths.

An MCC misalignment was suppressing approval rates across's multi-acquirer setup. Fixing it across all providers delivered a +5–7% approval rate lift across both subscription products.

If you're expanding across markets, local acquiring and alternative payment methods move up the priority list – both address costs that don't exist in a single-market setup.

ran routing, local acquiring, network tokenization, smart retries, and local payment methods through one platform, avoiding the cost and complexity of managing each separately. The result: +3.5% payment conversion and 5% less subscription churn.

Core insight: Payment optimization priority isn't universal – it depends on your current stack maturity (single acquirer, multi-acquirer, or multi-market), and each tier unlocks a different, provable set of levers.

Build a payment stack that keeps costs under control

Payment processing fees come from different places – card networks, your acquirer, your processor – and each has a different lever.

- Payment processing fees are lower with correct MCC and authorization data.

- Cross-border fees disappear with local acquiring.

- Failed renewals reduce with tokenization and smart retries.

- Fraud-related costs drop with better authentication.

- Processor markup comes down with comparison data and negotiation.

The challenge is that most of these levers depend on each other – and managing them across separate vendors adds the cost and complexity they're meant to reduce. A payment orchestration platform can bring them together into one system.

Solidgate connects to 100+ acquirers, providers, and alternative payment methods in one integration – with , smart retries, network tokenization, local acquiring, and fraud prevention built in.

If you want to see what that looks like for your setup, .

Frequently asked questions

Effective rates vary by card type, region, and transaction type. Average payment processing fees for digital businesses processing card-not-present transactions run from approximately 1.33% to 3.15% on consumer credit cards under , and 1.43% to 3.15% under – before assessment fees or processor markup are added. The gap between what you pay and what's possible depends largely on how well your transactions qualify and which cards your customers use.

Interchange and assessment fees are set by Visa and Mastercard and apply the same way regardless of which processor you use. The processor markup is the only component set independently by your processor – and the only line item open to negotiation. Visibility into what multiple processors charge per transaction is what gives merchants leverage.

sends each transaction through the acquirer or path with the lowest payment processing charges for that specific transaction, based on live performance and cost data. This differs from a static default that sends every transaction through the same route regardless of what it costs per card type or market.

Acquiring locally removes the cross-border classification that triggers additional network fees from Visa and Mastercard – the acquiring bank and issuing bank sit in the same country, so the transaction processes as domestic. Local acquiring also tends to improve approval rates, since local issuers treat domestic transactions with less default risk.

Payment orchestration becomes necessary once a merchant needs to route, retry, or negotiate across more than one acquirer. A single-acquirer setup can fix MCC accuracy, authorization data, tokenization, and fraud prevention – but can't act on routing, cascade logic, or processor negotiation without visibility across multiple providers.