UBO disclosure: Tips and tricks on how to easily pass the KYC procedure

Industry

Updated 5 Aug 2026

7 min

Kateryna Labai

Senior Compliance Officer, Solidgate

UBO identification ensures transparency, mitigates risks, and meets regulatory requirements, thereby helping to prevent financial crimes and ensuring compliance across various industries.

Anti-money laundering (AML) and counter-terrorist financing (CTF) have become the main priorities for competent authorities in the financial sector since the publication of the and the Paradise Papers, an unprecedented data leak related to offshore and shell companies. Consequently, new requirements based on transparency were implemented by regulatory bodies worldwide.

In this context, establishing a company’s ultimate beneficial owner (UBO) has become one of the most essential and efficient instruments for mitigating risks associated with ML and TF. The reasoning behind that is simple – to stop criminals from hiding their illicit activities and dirty money behind secret company structures. So, to cut a long story short, let’s look at the key definitions for UBO, UBO filing requirements, and UBO in KYC processes.

TL;DR

- A UBO (Ultimate Beneficial Owner) is the natural person who ultimately owns or controls a company and enjoys the benefits of ownership, even if they aren't the formal owner or director – and a UBO must always be a person, never a company.

- Under the EU's 4th Anti-Money Laundering Directive (4AMLD), a UBO is anyone who owns or controls more than 25% of a company's shares, voting rights, or ownership interest; if none can be identified, the senior managing official (CEO, CFO, etc.) is treated as the UBO.

- UBO identification is required for financial institutions, corporations, non-profits, and trusts to support anti-money laundering (AML) and counter-terrorist financing (CTF) goals; the 5th Directive (5AMLD) extended this to virtual currency platforms and tightened due diligence on high-risk countries and PEPs (politically exposed persons).

- To pass KYC (Know Your Customer) onboarding, provide a signed ownership-structure chart, valid UBO ID documents, proof of address (utility bills no older than 3 months), and the UBO's tax number – and keep all data accurate and matching national registers.

What Is an Ultimate Beneficial Owner (UBO)?

An Ultimate Beneficial Owner () is the person who ultimately owns or controls a company or legal entity. They are the individuals who enjoy the benefits of ownership, even if they are not listed as the formal owners or directors.

In the European Union (EU), the concept of UBO became more prominent with the introduction of the Fourth Anti-Money Laundering Directive (AMLD4). AMLD4, adopted in 2015, aimed to strengthen measures against money laundering and terrorist financing.

Under AMLD4, which came into effect in 2017, EU member states were required to establish registers of UBOs for corporate and legal entities operating within their jurisdictions. The purpose was to enhance transparency and combat financial crimes by ensuring that the individuals behind these entities were identified.

AMLD4 requires companies to provide information about their UBOs, including details such as their name, date of birth, nationality, and the extent of their ownership or control. The registers collect and store this information and make it accessible to relevant authorities and obligated entities like financial institutions.

The implementation of UBO registers varied across EU member states, with some opting for a centralized register and others maintaining separate registers. The objective is to create a comprehensive and accurate record of UBOs, enabling improved due diligence, risk assessment, and identification of potential money laundering or illicit activities.

Which organizations are required to identify UBO?

The requirement to identify Ultimate Beneficial Owners varies depending on the jurisdiction and the specific regulations in place. However, certain organizations that are commonly required to identify UBOs include:

- Financial institutions: Banks, credit unions, insurance companies, and other financial institutions are typically required to identify the Ultimate Beneficial Owners of their customers or clients. UBO in banking is used to prevent money laundering, fraud, and other financial crimes.

- Corporations and companies: Many jurisdictions require corporations and companies to disclose their Ultimate Beneficial Owners. This is aimed at promoting transparency, combating corruption, and preventing illicit activities, such as tax evasion and money laundering.

- Non-profit organizations: Some countries may require non-profit organizations to disclose their Ultimate Beneficial Owners. This is done to prevent misuse of funds, ensure proper governance, and maintain transparency in the operations of such organizations.

- Trusts and trustee companies: Trusts and trustee companies may be obligated to identify the Ultimate Beneficial Owners involved in trust structures. This is to prevent the misuse of trusts for illicit purposes, including money laundering and asset concealment.

It’s important to note that the specific UBO filing requirements can vary significantly by jurisdiction and the nature of the organization. It is advisable to consult the relevant laws, regulations, and guidelines applicable in your jurisdiction to determine the exact obligations for identifying UBOs.

What is a UBO, according to legal acts

FATF

According to Recommendation 25 of FATF, a beneficial owner is a natural person who owns or controls a legal person or arrangement and/or the natural person on whose behalf a transaction is being conducted.

CTA

The US Corporate Transparency Act (CTA) defines a beneficial owner as an individual who, directly or indirectly, through any contract, arrangement, understanding, relationship, or otherwise, exercises substantial control over the entity, or owns or controls not less than 25% of the ownership interests of the entity.

4AMLD

The 4th Anti-Money Laundering Directive (4AMLD) follows this approach and also clarifies the definition of the corporate entity’s UBO:

- UBO is a natural person who ultimately owns or controls the company through direct or indirect ownership of more than 25% of the shares, voting rights, or ownership interest, or through control via other means.

- If no one is identified as a UBO (having exhausted all possible means and provided there are no grounds for suspicion) or if there’s any doubt that the person identified is the beneficial owner, then the natural person who holds the position of senior managing official (CEO, CFO, COO, Partner, President, Treasurer, etc.) is considered a UBO.

The rules may differ from country to country, but generally, this is the most common approach to UBO meaning.

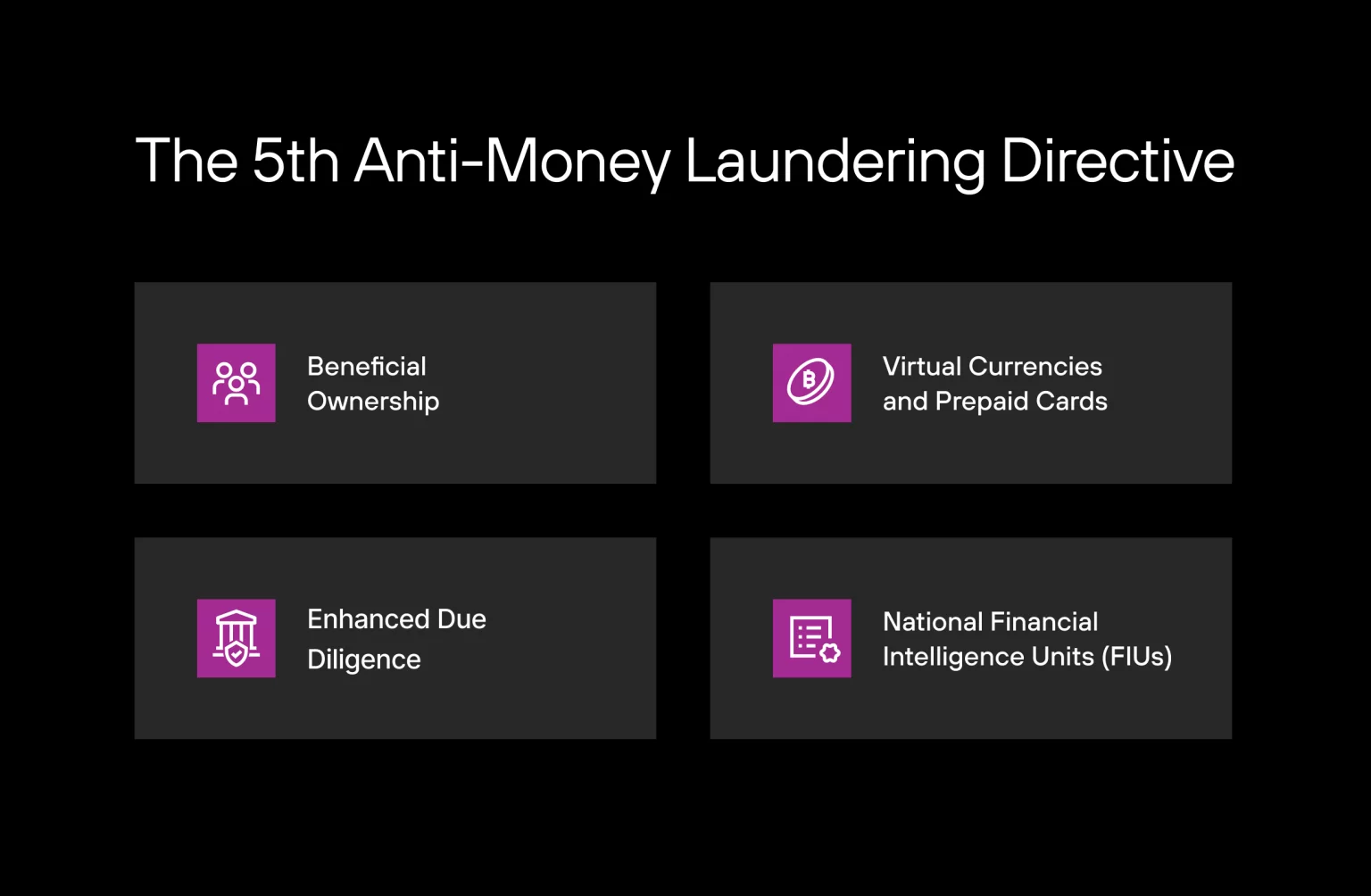

5AMLD

The Fifth Anti-Money Laundering Directive (5AMLD) is a legislative framework introduced by the European Union (EU) to strengthen measures against money laundering, terrorist financing, and illicit activities. Here are the key aspects of 5AMLD:

- Beneficial ownership: 5AMLD places increased emphasis on identifying and verifying beneficial ownership information. It requires member states to establish centralized registers of beneficial owners of corporate and legal entities, including trusts. This helps improve transparency and enables better identification of individuals who ultimately control and benefit from these entities.

- Virtual currencies and prepaid cards: The directive expands the scope of regulated entities to include virtual currency exchange platforms and custodian wallet providers. It aims to prevent the misuse of virtual currencies for money laundering and terrorist financing. Additionally, stricter regulations apply to anonymous prepaid cards to mitigate their potential misuse.

- Enhanced due diligence: 5AMLD introduces stricter customer due diligence measures. It requires obligated entities, such as banks and financial institutions, to conduct enhanced due diligence on high-risk third countries and politically exposed persons (PEPs).

- National Financial Intelligence Units (FIUs): The directive emphasizes the cooperation and exchange of information between EU member states’ national FIUs. It strengthens their ability to detect and combat money laundering and terrorist financing by enhancing the speed of information sharing.

The implementation of 5AMLD varies among EU member states, as they are responsible for incorporating the directive into their national laws. The directive is part of the EU’s ongoing efforts to combat financial crimes, increase transparency, and protect the integrity of the European financial system.

How to file UBO: Actionable guide

All financial institutions are required to verify the identities of UBOs who have directly or indirectly a certain amount of equity interest in their clients to understand, assess, and mitigate their risks.

Banking onboarding step by step

The classical procedure of banking onboarding includes these steps:

- the company’s up-to-date information (the exact specifications depend on the jurisdiction and the level of AML/CTF standards)

- Establishing an ownership chain

- Identification and verification of UBOs

- Final AML/CTF/ () checks (for example, sanctions/politically exposed person/adverse media screenings)

UBO compliance expert tips

We’ve prepared some tips to make your due diligence disclosure of UBOs run fast and smoothly:

- Be cooperative and provide the required documents showing the percentage of shares and their owners: certificate of shareholders/shareholder registry/UBO declaration, etc.

- Prepare an Organizational corporate structure chart (ownership structure), signed by an authorized signatory (usually a director), if the company has multiple layers of ownership. Please note that financial institutions can request corporate documents from all entities involved in ownership tiers.

- Provide identity documents of UBOs (for European banks – passports/identity cards, for American – passport/driving license/identity cards). Make sure that identity documents are valid, all information can be seen, and the scan copies are not blurry or covered in any way.

- UBO’s residential address should also be confirmed by providing utility bills/rental agreements/bank statements, etc. Generally, the utility bills should go back no further than 3 months.

- Provide UBO’s tax number and be ready to confirm UBO’s source of funds (in some cases, publicly available information is enough, but sometimes confidential information can be requested if the individual poses a greater risk for some reasons).

- Note that all information on the UBOs must be adequate, accurate, and up to date, corresponding to the national registers, as all financial institutions verify collected data in independent official sources.

UBO in KYC: Why it matters

Identifying UBOs during KYC ensures transparency, mitigates risks of money laundering, and fulfills regulatory obligations. Financial institutions use UBO in KYC to:

- Understand ownership and control structures

- Detect hidden risks or suspicious activities

- Comply with UBO disclosure requirements mandated by law

Summing up

Lifting the corporate veil is essential for long-term and reliable relationships with your banks, as the financial sector pursues maximum transparency nowadays. That’s why enabling your banking partners to respond appropriately to the challenges of the comprehensive regulatory sphere is a must. The compliance team is always here to assist you in meeting all UBO filing requirements and many other legal aspects of your online business.

Frequently asked questions

UBO compliance means adhering to laws requiring disclosure and verification of ultimate beneficial owners to prevent financial crimes.

Companies, financial institutions, trusts, and other regulated entities must disclose UBOs based on jurisdictional laws.

Generally, an ultimate beneficial owner must be a natural person, not a company. However, companies can be intermediate owners within ownership chains. The natural person who ultimately controls or benefits from the company must be identified as the UBO.

No, the UBO must be a natural person. Companies may be part of ownership chains but are not considered UBOs themselves.

Valid ID, proof of address, shareholder registries, ownership charts, and declarations are commonly required.

Typically, UBO data must be updated annually or upon significant ownership changes, depending on local regulations.

Non-compliance can lead to fines, legal penalties, blocked transactions, and reputational damage.