Visa announces new change to VAMP rules—Here’s what you need to know

Industry

20 Mar 2025

6 min

Daniel Yaremchuk

Risk Manager, Solidgate

Fraud tracking, VAMP ratio control, and proactive prevention—learn how merchants can use tools like RDR and Solidgate antifraud to maintain compliance.

Visa made a major update to its Visa Acquirer Monitoring Program (). Starting April 1, 2025, TC40 fraud alerts resolved through Rapid Dispute Resolution (RDR) will now count towards the VAMP ratio. In other words, RDR alerts won’t deflect TC40 anymore. This change means that fraudulent chargebacks could impact your VAMP metrics, so staying on top of fraud prevention and dispute management is crucial.

Let’s break down what this update means for you and what you can do to stay within Visa’s VAMP thresholds.

Struggling with VAMP compliance? Download the for clear, actionable steps to stay compliant.

Change to RDR and VAMP ratio

Visa initially stated that and non-fraud disputes resolved with Verifi prevention tools like (RDR), Order Insight, Compelling Evidence 3.0, and alerts from Cardholder Dispute Resolution Network (CDRN) would be excluded from the VAMP calculation.

With the new update, all TC40 fraud alerts resolved with RDR and CDRN will now count towards your VAMP ratio. This means that TC40 alerts that were once excluded are now part of the VAMP calculations, which could impact your risk statistics. This is a pretty big shift, so it’s essential to be aware and proactive in managing your risk metrics moving forward.

But here’s some good news: Non-fraud disputes (TC15) with RDR will still be excluded, so as long as you’re not dealing with fraud-related chargebacks, your VAMP ratio will likely remain within the thresholds.

What this means for merchants

Overall, this update adds more pressure for merchants to actively work on all-around fraud prevention. Visa’s decision to lower the risk threshold for acquirers from by 2026 will likely push acquirers to impose stricter requirements on merchants to ensure they stay compliant.

For example, an acquirer may set a merchant-specific VAMP ratio threshold at 0.5% (instead of Visa’s 0.9% for merchants) to create a buffer, ensuring their overall portfolio stays below Visa’s 0.3% cap. This means that even if your ratio is comfortably under Visa’s 0.9% threshold, you could still face penalties if your acquirer holds you to a stricter limit.

Merchants with higher dispute volumes or those in industries prone to higher levels of fraud and chargebacks might find it challenging. The need to manage multiple VAMP ratio limits across different acquirers could become a reality for many, adding pressure to keep fraud and disputes in check at all times.

The inclusion of TC40 in the VAMP ratio can make it more difficult for merchants to stay within the limits set by their , so proactive fraud management must become top of mind to avoid penalties.

Maintain healthy VAMP ratio

1. Monitor your VAMP ratio

The first step is to regularly monitor your fraud and dispute metrics. If your VAMP ratio rises above Visa’s , you could face penalties or even lose your ability to process payments with Visa. Staying proactive and ensuring fraud doesn’t go unnoticed is key.

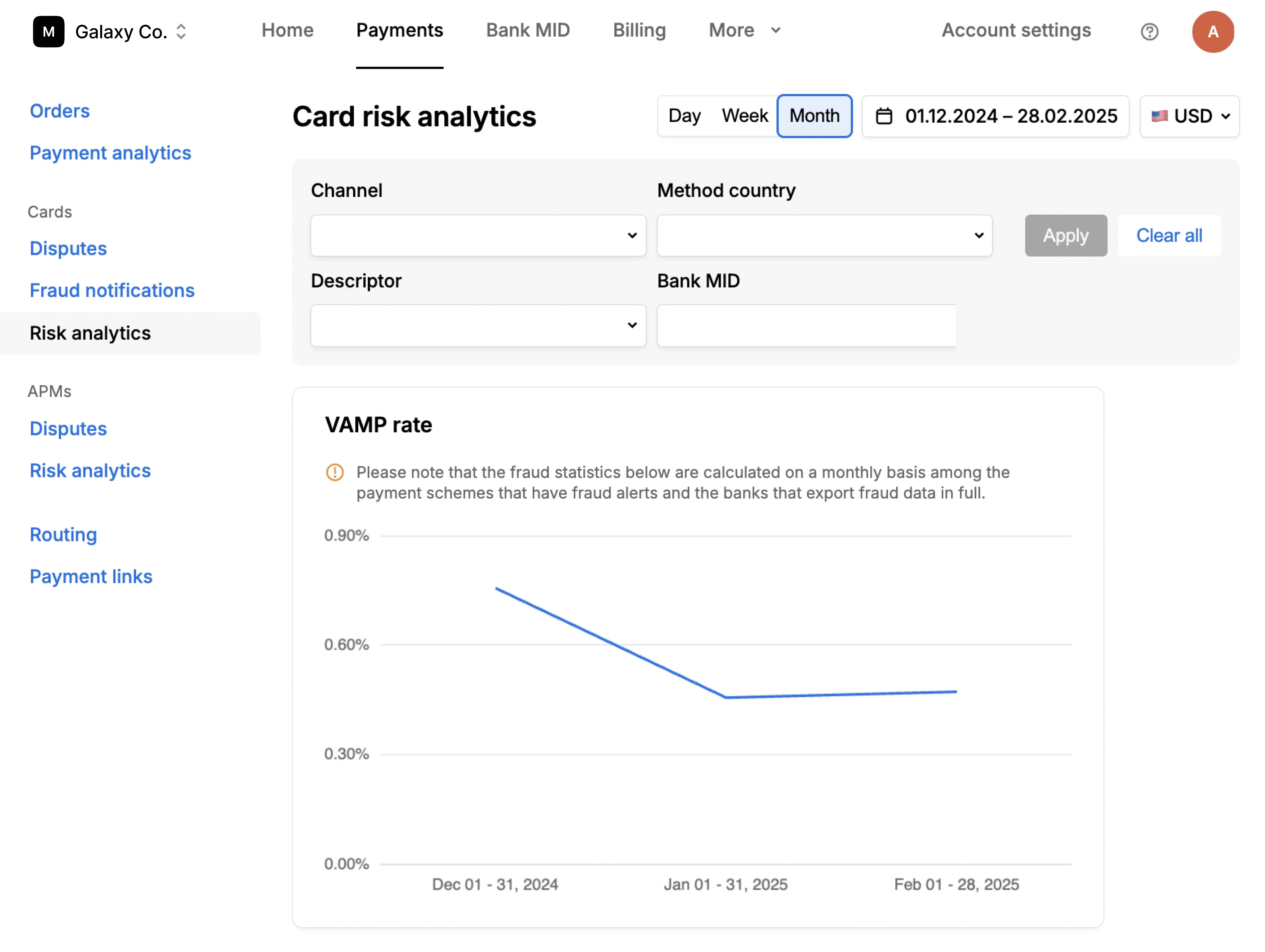

We have already added a VAMP rate chart to the Card Risk Analytics page in HUB to help you gain full visibility into your standing, monitor trends, and adjust your strategies.

difficult for merchants to stay within the

2. Leverage Solidgate’s fraud prevention tools

- RDR: excludes non-fraud chargebacks from the VAMP calculations, meaning fewer disputes count against you.

- Order Insight: helps you prevent first-party misused fraud. This tool gives you the ability to resolve disputes faster and avoid costly fraud-related issues.

- Compelling Evidence 3.0: makes fraud impossible under certain conditions.

- Direct Issuers alerts (CDRN/Ethoca): These direct alerts have a higher chance of resolving not just chargebacks but also fraud quickly, preventing it from counting towards the VAMP ratio. Although CDRN has limited coverage and doesn’t exclude TC40 disputes from the VAMP calculation, it still helps mitigate chargebacks and prevents many TC40 cases from being filed in the first place.

- Solidgate antifraud: solution helps reduce the enumeration count in VAMP by using velocity rules on fingerprint data from ThreatMetrix/LexisNexis. This system enables early threat detection, providing flexible protection without impacting conversion rates, and ensures precise fraud prevention powered by global data.

3. Keep improving your product offering

Offering a good product is one of the key tools for friendly fraud prevention. So, aside from using the right tools, work on fine-tuning your product and customer experience to minimize any potential fraud risk. The better the product and the more accurate its positioning, the fewer disputes you’ll have to deal with.

4. Stick to scheme requirements for subscription merchants

If you’re a subscription-based merchant, you need to stay in line with scheme requirements for subscription merchants. These guidelines provide you with essential directives on fraud prevention and risk management. Some of the key practices include:

- Set clear , cancellation, and subscription policies: Transparent and well-defined terms of service help you avoid payment disputes and give you the upper hand if a dispute arises with card issuers.

- Make your terms of service easy to access: Ensure your full Terms of Service (ToS) are easy to find, whether it’s on the checkout page or through a pop-up that requires customers to agree before completing their order.

- Send clear transaction receipts: After each purchase—whether initial or recurring—send a detailed receipt right away, even if the payment was unsuccessful (include the reason for failure). The receipt should include your business name, location, transaction amount, date, a clear description of the purchased service, the (Visa/Mastercard), the last four digits of the payment card, and subscription terms (length, auto-renewal, and price).

You can find the full requirements in our .

VAMP: A brief overview

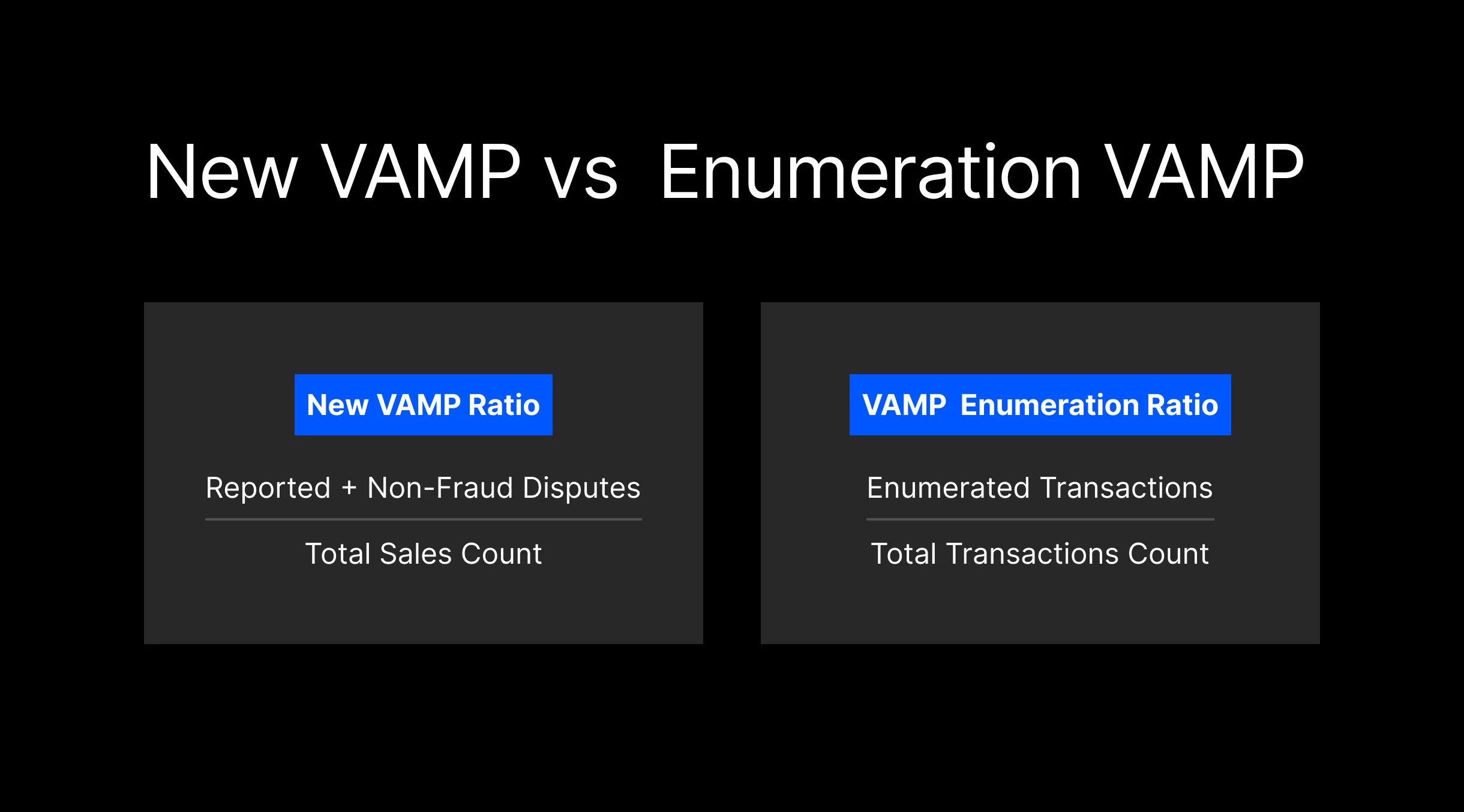

The Visa Acquirer Monitoring Program (VAMP) consolidates the Visa Dispute Monitoring Program (VDMP), the Visa Fraud Monitoring Program (VFMP), and the current Visa Acquirer Monitoring Program (VAMP) into a unified program. The new setup will feature a combined metric VAMP ratio that tracks both fraud and non-fraud disputes together, making it easier for Visa to manage risk across the payment ecosystem.

Merchants must also be aware of a new metric called the VAMP enumeration ratio. It tracks transactions where fraudsters test different combinations of card details like numbers, CVV codes, and expiration dates. A high VAMP enumeration ratio can indicate a higher risk of fraud, suggesting that criminals are actively trying to exploit the payment system.

| Note: If you process payments with Solidgate, there’s no need to worry about enumerated transactions. Solidgate Antifraud automatically blocks all enumeration attempts. |

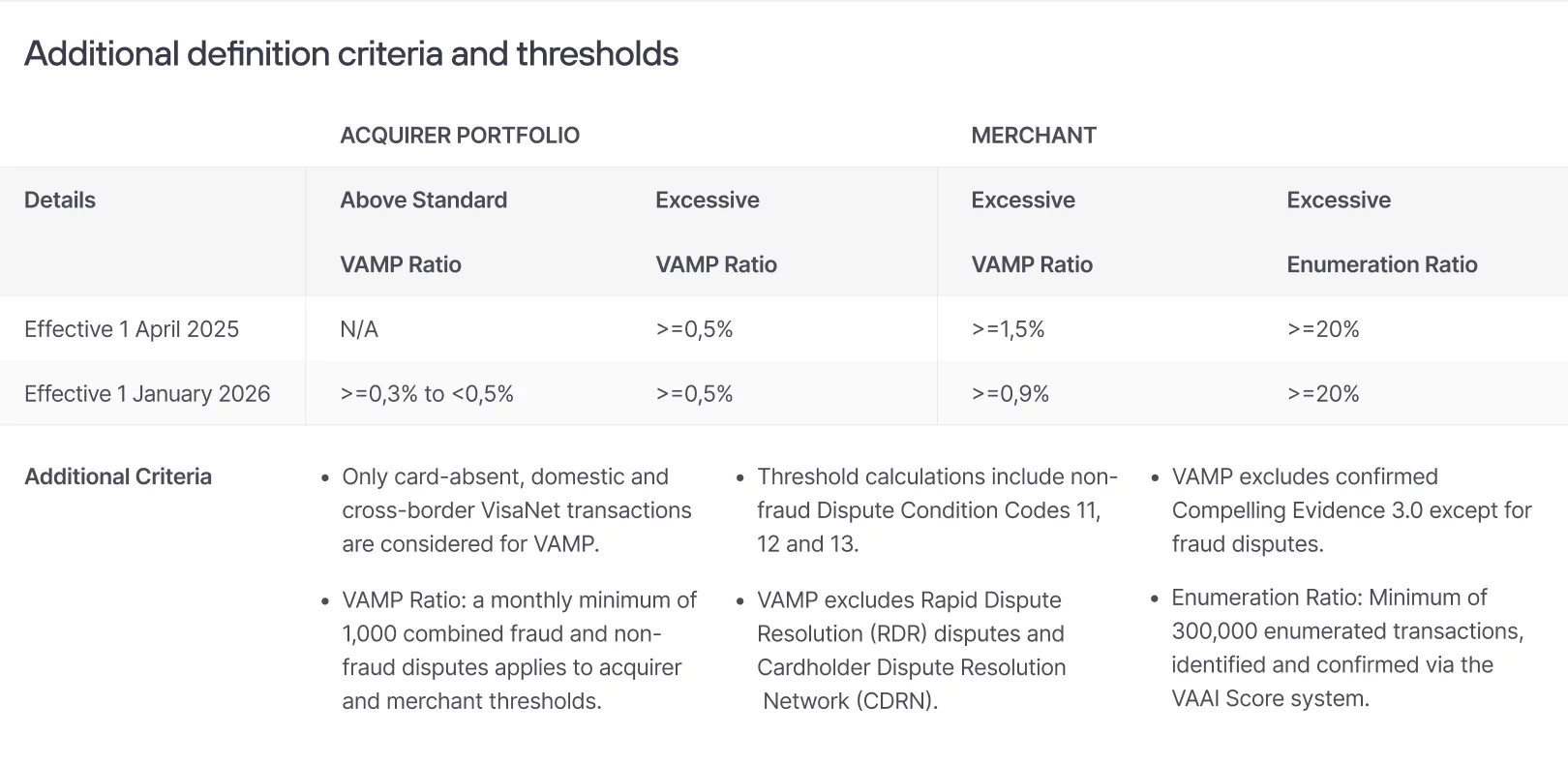

The Visa monitoring thresholds will change in two phases: April 1, 2025, and January 1, 2026. Below are the updated thresholds for the EU and Northern America:

If you exceed the set thresholds for the first time within a 12-month rolling period, you’ll receive a 3-month grace period to adjust your practices without facing penalties. During this time, you’ll be required to remediate, but no enforcement fees will be imposed. However, starting from the 4th month, enforcement fees will apply to each dispute (both fraud-related and non-fraud) if thresholds continue to be exceeded. This grace period is granted only once per 12-month rolling period.

A VAMP case will be closed once the acquirer or merchant brings their performance back within the specified limits.

For more information on VAMP, check our and .

Bottom line

The inclusion of TC40 fraud disputes means merchants now need to be even more proactive about monitoring their fraud activity and adopting robust fraud prevention measures. By improving your product, adhering to scheme requirements for subscription businesses, and using tools like RDR, Order Insight, and Compelling Evidence 3.0, you’ll have a much easier time staying within Visa’s VAMP thresholds.