Visa Rapid Dispute Resolution (RDR) and Chargeback Prevention

Industry

28 Aug 2023

9 min

Andrii Romanyshyn

Head of Chargeback Prevention, Solidgate

Discover how Visa Rapid Dispute Resolution (RDR) can help your business reduce chargebacks and improve refund management, especially when approaching Visa chargeback thresholds.

If you are dealing with a legitimate refund claim, Rapid Dispute Resolution prevention engines can be helpful to your business, especially if your company is approaching the Visa chargeback threshold.

With Visa Rapid Dispute Resolution, merchants will have a powerful solution to reduce valid . We will further discuss the specifications of an RDR tool and the benefits to a company that acquires it.

What is Rapid Dispute Resolution?

Rapid Dispute Resolution (RDR) is a new tool for merchants offered by Verifi (a Visa solution) that operates at the pre-dispute stage. The difference between RDR and CDRN is that Visa Rapid Dispute Resolution automates decision-making, with no action required from the seller beyond defining the initial rules.

According to internal data, Visa expects a 66% increase in digital payments, especially in card-not-present transactions. An RDR decision engine is here to automate dispute resolution.

In fact, RDR is present in a pre-dispute stage because it is not officially a chargeback. With Rapid Dispute Resolution, sellers can decide whether to credit the client to avoid a chargeback. It is a way to manage Visa disputes by showing customers that merchants wish to solve them quickly.

Therefore, in addition to reducing the number of conflicts, an RDR-resolved transaction will not negatively affect the sellers’ chargeback ratio and, consequently, reduce the number of disputes.

How can merchants use RDR?

A seller can take advantage of Visa Rapid Dispute Resolution to defend their business from chargebacks. But first, it is essential to identify whether you are facing criminal fraud or a merchant error. If this is the case, you should use RDR because it would be hard to reverse this situation in the seller’s favor. It is wiser to refund and avoid a chargeback.

Although, if you believe you are the target of , you can fight it through . Remember that your chargeback rate can be low if you refund every dispute, but you might find yourself with too many friendly fraudsters on your back, which can have financial repercussions.

A seller can reduce chargebacks by acting before they are filed. Using the previously defined parameters, the decision engine can determine whether to issue a refund to the customer. The Rapid Dispute Resolution Visa can then automatically issue the refund. No chargeback will be filed if the merchant accepts liability.

But how can sellers customize these parameters to their company’s needs? The first step is to analyze previous chargebacks and identify any patterns. And then focus on the parameters, such as transaction amount, chargeback reason code, and the client’s bank identification number. For example, an organization can establish that disputes under $40 will always be refunded because they do not justify the time and .

It is also important to remember that sellers should regularly review the rules to confirm they generate the desired outcomes. Sellers should consider the reasons for the disputes, the number of times a merchant accepts liability, the number of disputes that result in chargebacks, and how many were followed by representment and had a positive outcome, among other factors.

You can improve Rapid Dispute Resolution efficiency by analyzing data to ensure it is not refunding friendly fraudsters. Keep track of the refund rate, and if there are too many refunds and the risk of a chargeback is low, it is time to revise your rules. It will help ensure compliance with Visa chargeback limits. Be aware that Visa has a 0.9% chargeback rate and a monthly threshold of 100 chargebacks.

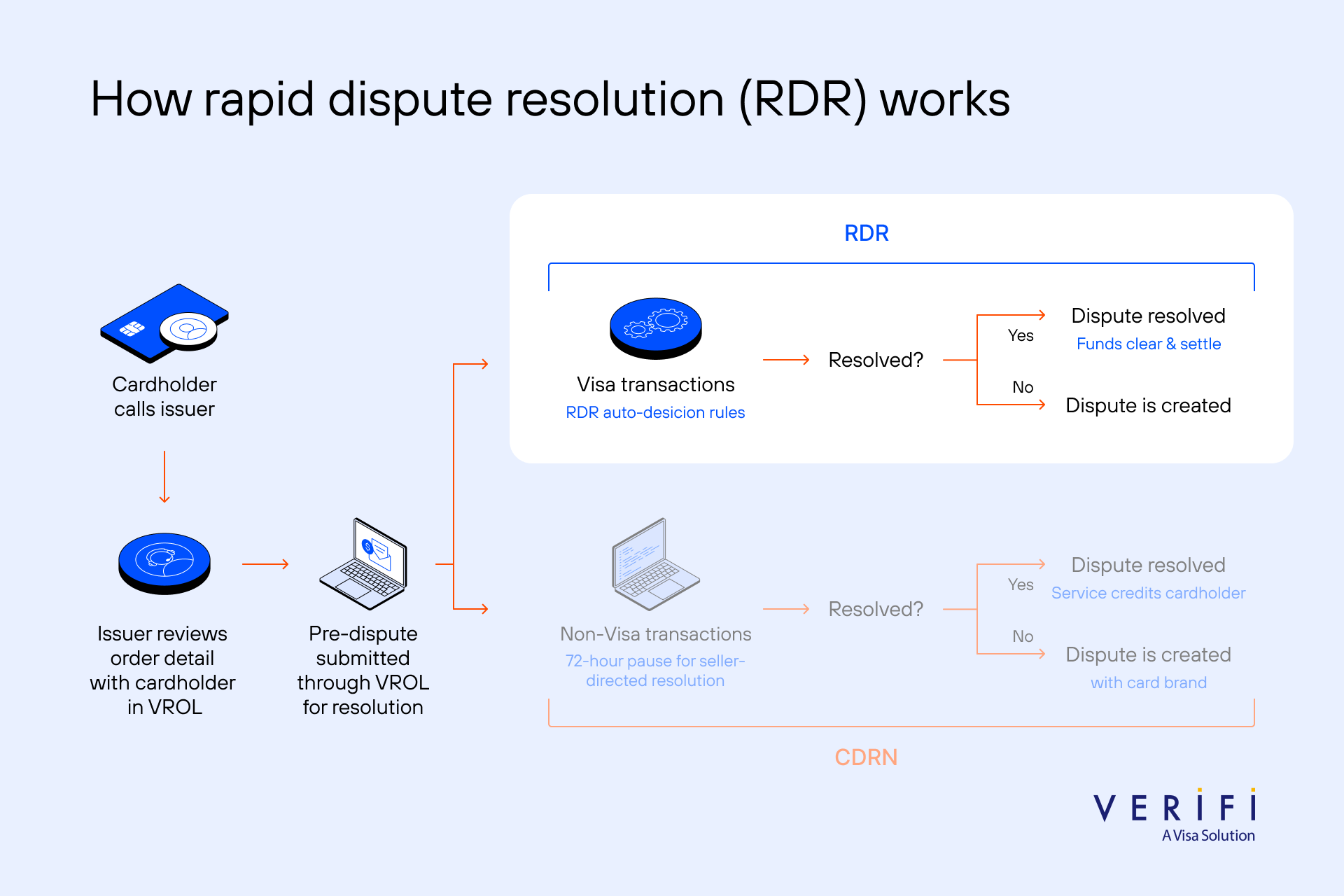

How does RDR work?

Rapid Dispute Resolution (RDR) will verify the previously defined rules and, based on them, determine whether the claim is eligible for a refund. The credit will then be automatically posted to the issuer’s account.

After a cardholder issues a transaction dispute, it will go through a Resolve solution. The seller with Rapid Dispute Resolution Visa at his disposal can automatically have the credit returned to the cardholder.

The merchant must fix rules and parameters for this to work efficiently. In fact, start by defining the disputes to resolve with Rapid Dispute Resolution, then tailor the parameters to be followed when evaluating the transaction data. Here you can find some examples of parameters that you can define according to your business requirements:

- Amount and date of the transaction

- Issuer BIN

- Chargeback reason code

- Purchase identifier

- Currency code

- Dispute category

Another significant advantage of Visa transactions is that Visa guarantees protect sellers. It ensures that the dispute is resolved and that no chargeback is initiated. Moreover, there will be no manual action from the merchant to send the funds to the client, so that they will be resolved more quickly. It means a zero impact on the chargeback ratio and improved customer service.

When the amount claimed is debited, Visa will share this information with the acquirer bank and then with the merchant.

Is RDR effective in reducing chargeback costs?

Visa’s Risk Dispute Resolution program helps merchants reduce chargeback costs by automating processes, customizing fraud rules, preventing chargebacks, reducing false positives, and ultimately increasing sales and conversion rates while minimizing friction.

- Automate processes: RDR streamlines the chargeback process by automating specific tasks, such as generating and submitting dispute responses. This saves merchants time and resources, allowing them to focus on their core business operations.

- Customize fraud rules: RDR enables merchants to set up and tailor fraud detection rules to their specific business needs. By implementing tailored rules, merchants can identify and flag potentially fraudulent transactions, reducing the risk of chargebacks.

- Prevent chargebacks: When using RDR, Visa guarantees that transaction disputes will not end in chargebacks. This ensures merchants don’t have to pay chargeback fees and additional processing fees due to a high chargeback rate.

- Reduce false positives: By leveraging advanced analytics and machine learning, RDR helps merchants improve fraud detection accuracy. This reduces the occurrence of false positives, where legitimate transactions are mistakenly flagged as fraudulent, ensuring that genuine customers are not inconvenienced or discouraged from making purchases.

- More sales and higher conversion: With reduced chargebacks, merchants can retain revenue that would have otherwise been lost. This leads to increased profitability and a more positive bottom line. Moreover, by optimizing fraud prevention measures and reducing friction in the payment process, RDR helps enhance the customer experience, leading to higher conversion rates and more successful sales.

RDR benefits for merchants

Visa RDR offers several key benefits for merchants, aiming to streamline the dispute resolution process and improve their overall experience. Here are the key benefits of Visa RDR for merchants:

- Faster dispute resolution: Visa RDR reduces the time and effort required from merchants to address and resolve disputes. This helps merchants save valuable time and resources, allowing them to focus on their core business operations.

- Avoid chargeback liability: RDR-resolved transactions are not considered chargebacks, so merchants can avoid costly fees and issues with their payment processor.

- Real-time notifications: Help merchants proactively manage disputes and minimize potential negative impact on their business.

- Improved efficiency: By leveraging automated processes, Visa RDR streamlines dispute management for merchants, reducing manual effort and paperwork.

- Enhanced transparency: Visa RDR offers enhanced transparency throughout the dispute resolution process. Merchants can gain clear visibility into dispute status, track progress, and receive updates on the resolution timeline. This transparency helps merchants better manage their resources and plan accordingly.

- Reduced financial impact: Providing instant provisional credit to the cardholder while the investigation is underway helps mitigate the immediate financial impact on the merchant. This ensures that merchants are not unduly burdened by chargebacks and can maintain their cash flow.

- Improved customer experience: Promptly addressing and resolving disputes contributes to customer satisfaction and loyalty. It also helps maintain positive relationships between merchants and their customers, leading to potential repeat business.

RDR benefits for the cardholder

Visa RDR improves the cardholder payment experience and satisfaction by enabling refunds to be issued virtually instantly. Here are some key benefits of Visa RDR for cardholders:

- Real-time notifications: Visa RDR enables cardholders to receive notifications for their card transactions in real time. This helps them stay informed about their account activity and promptly identify any potential unauthorized or fraudulent transactions.

- Instant provisional credit: When a dispute is filed, Visa RDR allows cardholders to receive instant provisional credit for the disputed amount. This means that the cardholder’s account is credited with the disputed funds while the investigation is underway, providing financial relief and minimizing the impact on their purchasing power.

- Expedited dispute resolution: Visa RDR aims to speed up the dispute resolution process, ensuring cardholders receive prompt resolution. It leverages advanced technology and automated processes to streamline investigations and decision-making, reducing the time required to resolve disputes.

- Enhanced transparency: With Visa RDR, cardholders have greater visibility throughout the dispute resolution process. They can track the progress of their dispute, receive updates on the investigation, and have clearer visibility into the resolution timeline.

- Improved fraud protection: Visa RDR incorporates advanced fraud detection and prevention measures to protect cardholders from unauthorized transactions. By leveraging real-time transaction monitoring and notification systems, suspicious activity can be identified and addressed promptly, minimizing the risk of financial loss.

- Convenient self-service tools: Visa RDR provides cardholders with user-friendly self-service tools and resources to manage their disputes. This empowers them to initiate disputes, submit relevant documentation, and communicate with their card issuer through online channels, enhancing convenience and accessibility.

Visa RDR benefits cardholders by providing them with real-time notifications, instant provisional credit, expedited dispute resolution, transparency, fraud protection, and convenient self-service tools. These features aim to enhance the overall cardholder experience, increase confidence in using Visa payment cards, and ensure a seamless and secure payment experience.

Potential consequences of using RDR

While Visa RDR (Real-time Dispute Resolution) offers advantages for merchants, there are some potential drawbacks to consider:

- Limited control over dispute resolution: With Visa RDR, the dispute resolution process is primarily handled by Visa and the issuing bank. Merchants may have limited control or influence over the outcome of disputes. This can be frustrating for merchants who prefer to actively participate in resolving customer issues.

- Potential impact on cash flow: When disputes result in refunds, merchants may experience negative cash flow. Visa RDR aims to expedite the resolution process, but refunds can still take time to be finalized. This delay may tie up funds and affect the merchant’s working capital.

- False positives and increased liability: While Visa RDR uses automated systems for dispute resolution, there is a risk of false positives, leading to legitimate transactions being flagged as fraudulent. This can lead to unwarranted refunds for merchants, resulting in financial losses and increased liability.

- Reliance on cardholder cooperation: Visa RDR requires cardholders to provide accurate and timely information for the dispute process. However, not all cardholders may understand the process or be proactive in providing the necessary details.

- Potential impact on customer relationships: The dispute resolution process, even with Visa RDR, can be a source of frustration for customers. When disputes arise, they may impact the merchant-customer relationship, potentially leading to customer dissatisfaction or loss of trust.

Merchants should assess their specific business needs, dispute volume, and customer dynamics to determine how Visa RDR aligns with their operations. Understanding the potential drawbacks and developing strategies to mitigate them will help merchants make informed decisions about utilizing Visa RDR for dispute resolution.

How Solidgate can help

With real-time automation, smarter decisioning, and proactive chargeback prevention, is a game-changer for merchants looking to:

- Save time: No more endless back-and-forth with banks—disputes are handled instantly.

- Cut costs: Save $20–$50 dispute processing fee per case and avoid operational slowdowns.

- Stay out of VAMP: Reduce chargeback rates on Visa and avoid being flagged in

- Enhance customer experience: Customers get quick resolutions, boosting satisfaction and loyalty.

This powerful tool allows early adopters to test its full capabilities and influence future refinements.

If you’re looking to stay ahead of the game in dispute management, with one of our experts to discuss how we can help you scale your payments!