PayPal disputes and chargebacks can quickly spiral out of control. Unlike traditional credit card chargebacks, PayPal follows its own chargeback process, making them unpredictable and difficult to fight. Many merchants start with a low dispute rate, only to see it quickly climb past chargeback thresholds for card schemes.

The problem with PayPal chargebacks for online merchants is threefold:

- It is easy to exceed PayPal’s thresholds, even if you run a low-risk business.

- Controlling your PayPal chargebacks is challenging due to PayPal’s obscure risk management mechanisms.

- If you cannot lower your risk metrics, PayPal may flag your account as high-risk, leading to increased reserve requirements and account processing limits that restrict your cash flow.

If PayPal is essential to your sales—like it is for 81% of growth-oriented online businesses in the U.S.—a tailored chargeback prevention and management strategy is critical to your operations and bottom line.

This guide breaks down how PayPal chargebacks work, why they happen, and how to stop chargebacks on PayPal before they become a problem for your business.

Table of Contents

Understanding PayPal disputes, claims, and chargebacks

Not all PayPal disputes turn into chargebacks. Understanding the differences is the first step to taking control of your metrics.

The initiation stage: PayPal dispute

The first opportunity to resolve a PayPal issue is at the dispute stage. This is the most critical point for chargeback prevention. When a customer reports a problem, merchants have the chance to communicate directly with them to clarify the situation or promptly issue a refund

- A customer reports an issue through PayPal (e.g., missing item, unauthorized charge, service complaint).

- You can communicate directly with the buyer to resolve the issue.

- If resolved at this stage, no chargeback is filed.

Resolving disputes at this stage is crucial. PayPal prefers amicable resolutions, and merchants who engage early can significantly reduce the risk of escalation. More than 60% of disputes can be resolved at this stage if you respond promptly.

The escalation stage: PayPal claim

If a dispute is not resolved, it moves to the claim stage, where PayPal steps in to make the final decision.

- If the dispute isn’t resolved, the buyer escalates it to a claim.

- PayPal steps in and decides who gets the money.

- If you don’t respond, PayPal rules in favor of the buyer by default.

At this stage, your ability to submit compelling evidence is critical. According to the updated Resolution Center rules, you have 10 days to respond to a dispute. This includes:

- Proof of delivery (tracking numbers, signatures, delivery confirmation emails).

- Customer communications indicating the issue was resolved.

- Clear refund policies that were presented before purchase.

The final stage: External chargeback

The most damaging scenario occurs when a customer files a chargeback through their issuing bank instead of using PayPal’s dispute resolution system.

- Instead of using PayPal’s system, the buyer disputes the transaction with their bank.

- The bank makes the final call—sometimes overruling PayPal’s decision.

- Chargebacks count against your risk metrics and can trigger account restrictions.

This is the worst-case scenario for merchants, as PayPal has limited ability to overturn chargebacks issued by banks. If your chargeback rate exceeds 1%, PayPal may place your account on review, restrict withdrawals, or increase your rolling reserve percentage.

Why do customers file for PayPal chargebacks?

Understanding the root cause will help you address it. The most common reasons include:

- Friendly fraud or unauthorized transactions.

- Subscription billing issues.

- Customer dissatisfaction.

- Delivery delays or missing shipments.

According to PayPal’s chargeback policies, fraud-related disputes account for 30-50% of claims. However, a significant portion stems from preventable misunderstandings—such as customers forgetting they signed up for a subscription or being unaware of the merchant’s refund or cancellation policies. We touch on this issue in our survey Success With Subscriptions: How Businesses Can Meet Customer Expectations.

Behind the scenes: How PayPal distributes chargeback rates

Because PayPal operates as a digital wallet, its fraud prevention mechanisms differ from those of traditional credit card processors. PayPal supports various payment methods, including e-checks, bank transfers, card payments, and Buy Now, Pay Later (BNPL), and doesn’t disclose exactly how it calculates and distributes chargeback rates among them.

Our data indicates that:

- PayPal assigns transactions across multiple merchant IDs (MIDs), making tracking chargeback rates difficult.

- Because PayPal doesn’t differentiate chargeback rates by card scheme, calculating an exact rate for a specific scheme is difficult. A rough estimate—such as distributing Visa and Mastercard transactions at 50%—can be used, but it’s not entirely precise.

As a result, some MIDs may exceed allowed chargeback rates, even if your overall rate remains below monitoring thresholds. Here’s the formula to calculate your PayPal chargeback rate:

Chargeback rate = total count of chargebacks (current month) / total count of sales (current month)

💡 Note: There is a distinction between “total card sales count” and “total sales count.” For example, a PayPal purchase made after a wallet top-up does not count as a card transaction.

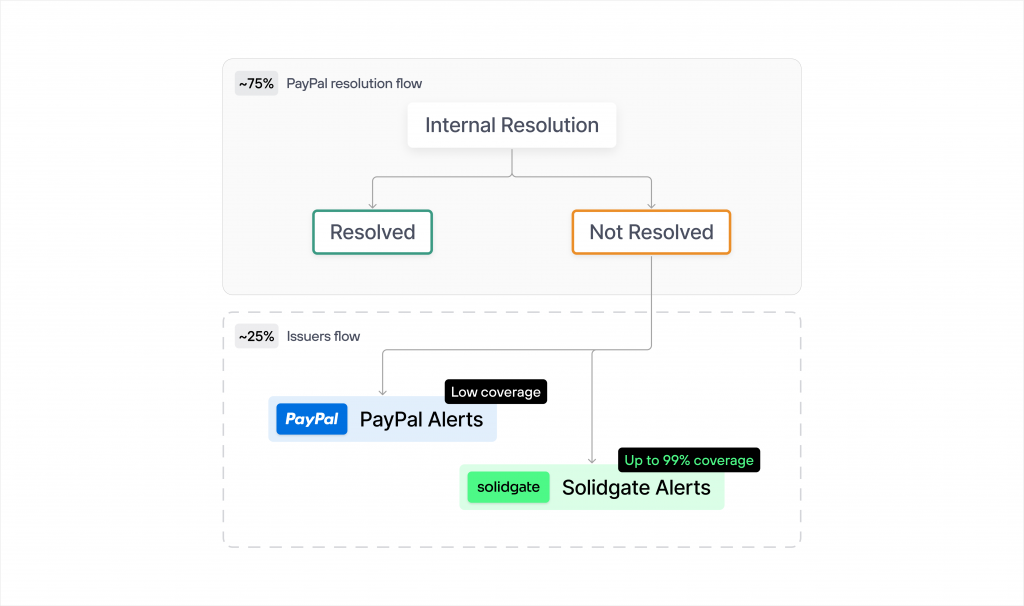

The limitations of PayPal’s pre-chargeback alerts

PayPal pre-chargeback alerts is a native PayPal feature that sends merchants alerts about transactions with an increased chance of a chargeback claim. It works like this: you receive an alert about a transaction in the PayPal Resolutions Center. After that, you have 20 hours to:

- Contact the customer.

- Offer a refund if needed.

- Provide evidence if the claim is invalid.

But there are a few problems. First, native PayPal’s pre-chargeback alerts lack full coverage, particularly for Visa transactions. This means you will still miss out on a significant chunk of alerts that will turn into chargebacks.

Another problem is the lack of visibility into transaction details. PayPal typically hides customer payment data, making it problematic to match alerts to transactions and track the source of chargebacks. Responding to all chargeback claims timely becomes almost impossible, especially if you have a high transaction volume.

As a result, many disputes slip through the cracks, turning into Visa and Mastercard chargebacks in the PayPal Resolutions Center. This increases chargeback ratios, places merchants into scheme monitoring programs, and leads to PayPal processing issues.

How to avoid chargebacks on PayPal step-by-step

To avoid all the problems that come with excessive PayPal chargebacks, you need proactive strategies tailored to PayPal’s system.

Enable external pre-dispute alerts for PayPal

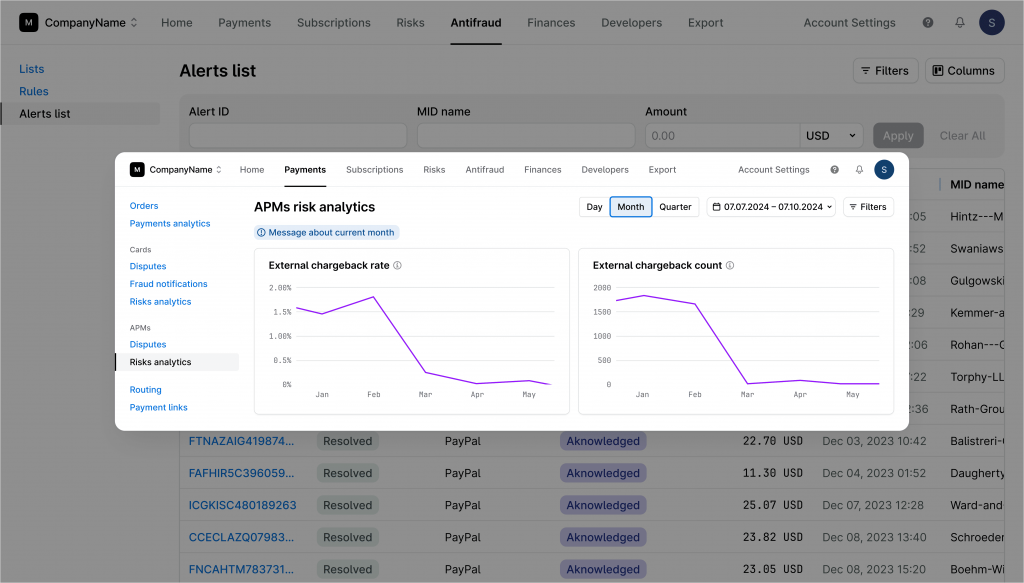

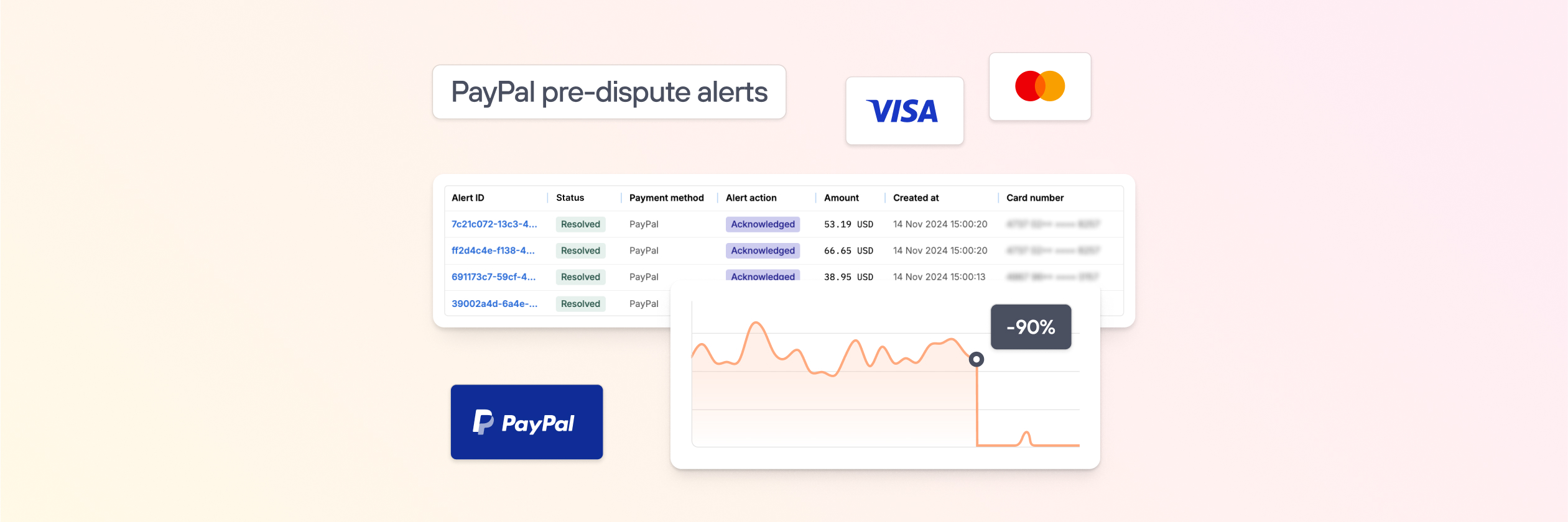

As said before, native pre-dispute alerts on PayPal don’t provide enough coverage and visibility into transactions, limiting your control over chargebacks. To solve this long-standing problem for global merchants, we at Solidgate have developed an industry-first PayPal dispute automation solution that overcomes these limitations and provides:

- Full pre-dispute alert coverage across all major card providers

- Real-time monitoring and matching of alerts to orders

- Fully automated alert handling

- Real-time data to optimize your refund policies and chargeback strategies

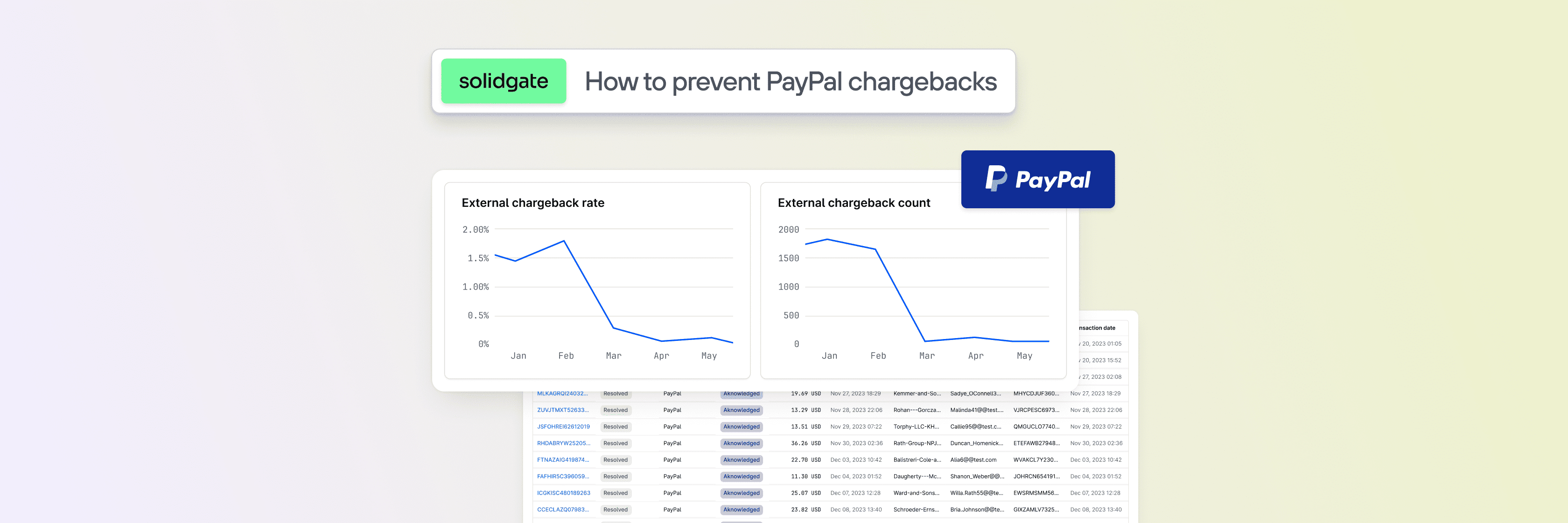

The results for our merchants have been astounding: PayPal chargeback rate dropped by 90% within just one month.

Want to reduce your PayPal chargebacks by 90%? Contact your account manager or book a call with our experts.

De-prioritize PayPal in your checkout flow

Offering alternative payment methods first (e.g., credit cards, Google Pay, Apple Pay) and placing PayPal below can encourage customers to use less risky methods. It will naturally reduce PayPal transaction volume and lower risk without impacting sales conversions. If possible, keep the volume of PayPal transactions below 25% in your payment structure.

Implement a clear “unsubscribe” flow

If you operate a subscription model, make sure your “unsubscribe” flow is as clear as day:

- Make the Unsubscribe button visible in emails and account settings.

- Send an immediate confirmation email upon cancellation detailing the effective date and refund policy.

- Develop a self-service portal where users can manage subscriptions and request refunds without contacting support.

This approach goes beyond reducing friendly fraud on PayPal, ensuring compliance with the new FTC negative option rule regulation.

Notify customers before re-billing them

Many subscription businesses don’t notify customers before automatic subscription renewals. Such charges catch customers off guard, resulting in increased refund requests and chargebacks. You can easily avoid this by sending an automated email notification 7-10 days before renewal.

Block/limit unauthorized transactions from the geographies with high fraud rates

Certain countries and Tier 3 regions, such as Latin America, Africa, and Southeast Asia, experience more fraudulent transactions. If your reports indicate a high volume of fraudulent transactions from specific locations, blocking or limiting traffic from these regions can reduce risk.

Taking control over PayPal chargebacks

It’s very easy for PayPal chargeback rates to get out of hand—and once they do, getting back in good standing is challenging. Proactively implementing prevention and resolution strategies is essential to protect your operations and bottom line.

Make sure to:

- Monitor all PayPal pre-dispute alerts to promptly refund those you don’t want to challenge.

- Tighten fraud prevention by blocking high-risk transactions.

- Ensure clear cancellation and billing communication (for subscription businesses)

With the right strategies, you can protect your revenue and keep your PayPal account from limitations.

![PayPal Fraud Prevention Recommendations [PDF]](https://solidgate.com/wp-content/uploads/2024/06/PayPal-fraud-prevention-guide.png)