With an estimated 74% of European internet users now shopping online and skyrocketing inflation driving profit margins down, merchants are becoming more aware than ever that they need to invest in their online payment processes now. One of the top priorities is implementing more APMs.

The European market has many alternative payment methods available, so Europe presents a very high growth potential for alternative payments. The European alternatives to traditional banking have exploded recently, with Statista estimating that the market will grow to more than 1.5 billion transactions annually.

Alternative payment methods are an essential part of the digital economy. They can be used by consumers and businesses, who use them to pay for goods and services online. Alternative payment methods include cryptocurrencies, e-wallets, and direct debits.

This article aims to provide an overview of the alternative payment landscape in Europe. We’ll explore the different types of alternative payments, highlight some key players and mark down some unique challenges for sellers.

Table of Contents

What are Alternative Payment Methods?

Alternative payment methods are becoming increasingly popular in Europe. In fact, alternative payment methods have the potential to revolutionize how we pay for goods and services. But what is an alternative payment method?

Alternative payment methods are financial transactions that are not made via cash or major card schemes (Visa, MasterCard). They are popular in Europe but less commonly used elsewhere in the world.

Alternative payment methods can be very convenient for online shopping because they can often be processed instantly by the merchant when you purchase on their website (which means no waiting around for your funds to clear).

This is not possible with credit or debit cards – these must be authorized by your bank first, which takes time and may result in declined payments if there’s an issue with your account or card details.

Another advantage of alternative payment methods is that because they don’t require a bank account, they’re often cheaper than other forms of online payment like credit cards and debit cards (although this isn’t always true).

Let’s take a look at some of the popular payment methods in European countries.

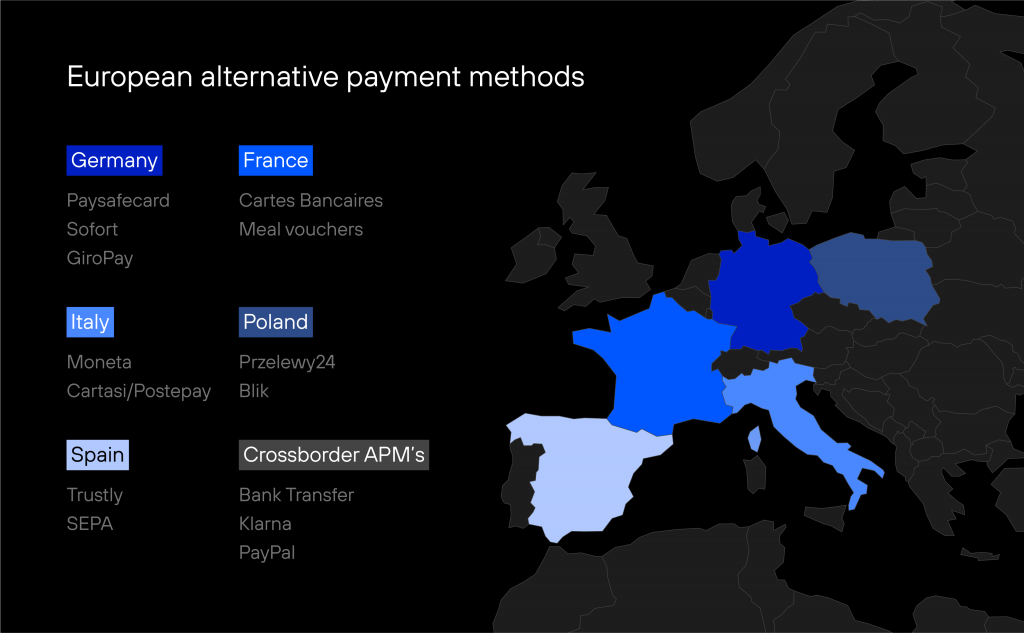

APMs in Germany

Alternative payment methods have become increasingly popular in recent years, especially in Germany, where credit card usage is not as widespread as in other countries. Consumers are looking for more secure and convenient ways to pay for their purchases, both online and in person. The three most popular alternative payment methods in Germany include Paysafecard, Sofort, and GiroPay, thanks to their ease of use and high level of security.

Alternative payment methods really started gaining traction in Germany in the early 2000s due to the development of the internet and online banking. Paysafecard arrived in Germany in 2001, Sofort was founded in Munich, Germany, in 2005, and Giropay launched the same year. These APMs have grown incredibly popular, with Giropay processing over 1 million transactions every month and Sofort being the most used payment method by 4% of Germans. Let’s take a closer look at each of these payment methods and how they work.

Paysafecard

If you’re looking for a way to pay online without using a credit card, you may want to consider Paysafecard. This prepaid payment method is accepted in many countries worldwide and allows you to purchase it at various locations. It’s also a secure payment method because the money is transferred directly into your account (as opposed to being held by a third party), so it can be used for both online and in-person purchases.

Sofort

Sofort is a payment method that allows you to make and receive payments through your smartphone or computer. It’s available in all of Germany, which means it works for both B2B and B2C transactions. The technology behind Sofort is provided by the payment services provider Wirecard Bank AG with its headquarters in Munich, Germany.

The service was founded in 2000 by four German banks: Commerzbank AG, DAB Bank AG, Deutsche Bank AG, and Postbank, as well as private investors such as Ströer Interactive Media GmbH (now Ströer Digital Media SE) and Kreditech Holding SE.

In 2005 it was renamed “Sofort,” which translates into English as “immediately” or “instantly”; this name change was done so that people would associate Sofort more closely with the word “fast” than any particular type of transaction method (like wire transfers).

GiroPay

GiroPay is a payment service provided by Sofort AG. It’s similar to PayPal but only available in Germany. GiroPay is considered more secure than PayPal because it requires users to enter their CVV2 code when purchasing instead of just their password. This prevents hackers from accessing your account and stealing your money.

GiroPay lets you pay for goods and services online without needing an account with the merchant beforehand (similar to PayPal). You simply enter your card information on their website, approve the transaction, and complete your purchase as usual.

APMs in France

Alternative payment methods in France have a history dating back to the 1980s, when the Cartes Bancaires debit card was introduced as a secure and convenient alternative to cash and checks. In the 1990s, online payments started to gain popularity in France with the launch of the electronic wallet called Cybermut, created by the Crédit Mutuel Bank.

In the 2000s, the emergence of mobile payments led to the launch of services such as Paylib, a digital wallet created by a group of French banks in 2013. The same year, Lydia, a peer-to-peer payment app, was also launched in France. Another popular alternative payment method in France is meal vouchers, known as Titres-Restaurant, which have been in use since the 1960s. They are widely accepted in France and are a popular way for employees to save money on meals.

Overall, the history of alternative payment methods in France has been driven by a desire for convenience and security, as well as regulatory frameworks that have encouraged the development of innovative payment solutions. Let’s look at the most popular French APMs, Cartes Bancaires and Meal Vouchers in more detail.

Cartes Bancaires

In France, banks are the most popular choice for online payments. Most people use credit cards to make online purchases, although some prefer debit cards or prepaid cards. In France, there are many different payment methods: Cartes Bancaires is the most popular method because it offers a high level of security and is widely accepted by European merchants.

Meal Vouchers

In France, you can purchase meal vouchers from supermarkets and gas stations from €10 to €100. These are prepaid cards that can be used at restaurants, cafes, and bars. There are different versions for adults and children. Consumers can use them in any currency, but they aren’t as popular as they once were because of the rise of electronic payments like PayPal, which doesn’t require a physical card or cash to make payments.

APMs in Italy

Italians love their credit cards, especially when shopping online! 44% of Italians prefer using credit cards for e-commerce purchases, while 40% reach for their debit cards instead. Despite the prevalence of credit and debit cards, Italians are a little old school. 27% of in-store purchases are done via cash; however, this figure has more than halved since 2019, when 60% of brick-and-mortar shopping was transacted using cash.

The Covid-19 epidemic really shook up the payments industry in Italy. For the first millions of Italians were receiving and spending money digitally. Their salary was sent to their online bank account or prepaid card, and instead of going to the shops with a wallet full of cash, they were on lockdown and forced to shop online. It seems like the habit of using cards in Italy has stuck with Moneta and Cartasi/Postepay use skyrocketing, find out more about these Italian APMs below!

Moneta

Moneta is a payment system used in Italy. It’s owned by Banco BPM, the largest Italian bank; the company was created in partnership with Visa and Mastercard. The Moneta app allows users to pay for online and in-store purchases using their mobile phones. It can also be used to make payments through POS terminals at restaurants or shops.

Cartasi/Postepay

Cartasi/Postepay is a payment method that allows you to pay using your phone, bank account, credit card, or cash at the store. Cartasi/Postepay is only available in Italy.

APMs in Poland

The Poles have been slow to embrace new payment methods and online shopping in general. Despite being a country of 38 million, Poland’s e-commerce market is only worth $12 billion per year, whereas the UK’s e-commerce market is over 10x larger.

A lot of Poles, particularly the older generation, are suspicious of digital payment methods and still prefer to use cash. Only 18% of Poles use credit cards for online purchases due to the stigma debt has in the country. The majority of online transactions in Poland are conducted via online bank transfers (54%) and e-wallets (18%). E-wallets and mobile payment systems like Blik are only going to get more popular as the next generation fully embraces alternative payment methods, and Przelewy24 has already done a great job of facilitating online bank transfers. Find out how these APMs work below.

Przelewy24

In Poland, you can use Przelewy24 to pay for things online or through your bank account. It’s a popular alternative payment method that allows you to transfer money from one account to another. You can do this in one of three ways:

Credit card – if you have a credit card issued by a Polish bank, then you can use it as your primary payment method on websites that accept Przelewy24. This is usually the most convenient and fastest way of paying with this method, as there are no additional fees involved (as opposed to online banking or bank transfer).

Bank transfer – if you don’t have access to a credit card but want to pay via Przelewy24 anyway, then transferring money directly from your bank account is an option. Make sure both the sender’s and recipient’s names match up correctly before submitting the transaction for processing. The downside of using this option is that additional fees may be associated with it (for example, if someone else has already used their credit card on the said website).

Online banking – many people prefer this alternative because they don’t have enough funds available on their cards at any given time (e.g., during holidays when demand rises significantly due to higher sales volume). However, sending payments directly from one person’s personal savings account without intermediary steps is not always possible, depending on the type of service purchased.

Blik

Blik is a mobile payment system that allows you to make payments with your smartphone. It was created by Blik Labs and is used by some Polish retailers, including popular brands like Tesco outlets, Eurekakids, and HMV Poland. Blik has grown in popularity as more Polish retailers accept it as a valid form of payment. You can now use your Blik app to pay for goods at over 10,000 locations throughout Poland.

APMs in Spain

Spain may not have a reputation for being an innovative tech hub, but they have embraced alternative payment methods. The first Spanish credit card was launched way back in 1970, and Spaniards have been making online purchases via PayPal since 2005.

The most popular online purchase methods in Spain are Mastercard and Visa, accounting for over 50% of all purchases. However, mobile and alternative payments are seeing a surge in popularity as Spaniards chase comfort, security, speed, and rewards. Spaniards have tons of choice when it comes to payment methods and frequently use Trustly, SEPA, online bank transfer, PayPal, and Klarna, keep reading to see how these APMs work.

Trustly

Trustly is a Swedish company that provides an online payment service, with headquarters in Stockholm. Retailers in Sweden, Finland, Denmark, and Norway use Trustly. It also has operations in Poland and Spain and a partnership with Italian mobile phone carrier TIM, allowing merchants to accept payments via TIM’s retail network.

The service allows users to exchange money between their accounts without entering bank account details or credit card information into online checkouts. Instead, they simply register with Trustly once and use their username as the unique identifier for all future transactions on any partner site.

SEPA

SEPA is a single payment space for Europe. It is an initiative of the European Union and was created to improve cross-border payments within Europe. SEPA allows people in Spain to make payments in euros instead of having to pay in their local currency.

For example, if you live in England and want to buy something from Germany, you would have had to pay your German seller via Bank Wire Transfer or PayPal until now because they were not compliant with UK regulations on international payments (for example, Maestro cards). However, if you use SEPA, it will allow this transaction as well as many others like:

- Credit card transactions

- Direct debits

- Direct credit transfers

APMs in UK

Brits have virtually every single payment method at their fingertips. A wide range of vendors accept everything from e-wallets to credit cards to bank transfers. Credit and debit cards account for over 50% of online transactions in the UK, with e-wallets coming in second at 32%. Unlike in the Netherlands, online bank transfer is not popular at all, accounting for only 7% of payments, but that might change with the emergence of Pay by Bank app by Mastercard, which offers instant and easy transfers. See below some of the top alternative payment methods in the UK.

Pay by Bank app

The Pay by Bank app from Mastercard allows you to make instant online payments using your bank balance. You don’t have to download any apps, simply select Pay by Bank app at checkout, you will then be taken to your online bank account, where you can see your balance and confirm your payment with one click!

UK Direct Debit

With direct debit, you authorize your bank to transfer a specific amount of money to a 3rd party on the same day for an agreed-upon period of time. How it works is a company will send you a direct debit authorization form. Once you have filled out the form, the company will send the form to their bank, which will collect the money from the bank. Direct debits help businesses collect payments automatically, and customers don’t have to worry about paying individual bills every month.

APMs in the Netherlands

Credit cards are not widely used in the Netherlands, with many vendors straight-up refusing to accept them. Even at some major supermarkets in the Netherlands, you can’t use your credit card. Interestingly, Visa and Mastercard debit cards are treated as credit cards and are rejected in numerous stores, so don’t panic if your transaction gets declined when shopping in Amsterdam.

The Dutch are obsessed with their Maestro and Vpay debit cards. Debit cards are by far the most popular payment method in the Netherlands, accounting for 60% of transactions. In second place is iDEAL, which allows the Dutch to make online bank transfers instantly.

iDEAL

iDEAL was launched in 2005 and facilitates online payments via bank transfer in the Netherlands. It allows Dutch people to pay virtually everything online using cash in their bank account. iDEAL is responsible for 70% of all online payments in the Netherlands and is used to pay for everything from energy bills to online shopping.

The way iDEAL works is that during checkout, the customer selects iDEAL as their payment method and bank. Then they are transferred to their online bank, where they enter their account number and confirm the transaction using 2FA. The merchant receives the money instantly. The only downside to iDEAL is there is no chargeback capability. Find out about some of the top alternative payment methods in the Netherlands which are growing in popularity.

BitPay

BitPay, launched in 2011, is a Bitcoin payments company that allows you to spend your Bitcoin in-store and online. How it works is that you download the BitPay app, get a Mastercard BitPay card, connect your Bitcoin wallet, and then use the card like a standard debit card.

While BitPay is not incredibly popular in the Netherlands, it has seen a sharp uptick in usage as more and more people use Bitcoin. It is currently estimated that 3% of Dutch own at least some Bitcoin, so expect BitPay’s Dutch users to continue to grow!

Hyperwallet

Hyperwallet is a PayPal company that helps companies pay people. With the click of a button, Hyperwallet allows you to send local payments across the world in 20 + currencies. Some of the payment methods include bank transfer, prepaid card, gift card, cheque, and cash pick up. As the Netherlands is a small country, but with a strong economy, there are numerous businesses with employees and clients spread around the world. Hyperwallet makes it easy for these businesses to quickly and securely pay individuals no matter where they are, what currency they use, and what payment method they prefer.

APMs in Belgium

Belgium is similar to the Netherlands in the fact that credit cards and Visa/Mastercard are not popular. The number 1 payment method is a local debit card, Bancontact, which was used 2.3 times in 2023 alone. Interestingly bank transfers and e-wallets are rarely used in Belgium, accounting for 2% each of online purchases. Instead, Belgian people are increasingly turning to mobile payments facilitated by the likes of Payconiq. Below we will explore Bancontact and Payconiq in a little more depth.

Bancontact

There are over 15 million Bancontact cards making it the most popular online payment method in Belgium. Bancontact is a debit card that is linked to a Belgian bank account and is just like Visa or Mastercard. You can enter your card details during checkout to shop online or tap/swipe when shopping in-store.

Payconiq

Payconiq is the top QR code and mobile payment processor in Belgium. With Payconiq, you can scan a QR code, then open the Payconiq app or other supporting apps such as ING Banking and KBC Mobile, enter the amount you need to pay, and confirm the transaction. You can link your card or bank account to the Payconiq app.

Crossborder Alternative Payments Methods

Bank Transfer

Bank transfer is the most common payment method in Europe. It can be used to pay for goods and services or send money from one account to another. To send a bank transfer, you need the recipient’s IBAN, a unique way of identifying individuals and businesses across Europe. For example, if you want to pay your friend in Barcelona €100 for coffee on Monday morning, all you need is their IBAN (a unique identifier) and an internet connection!

Klarna

Klarna is a Swedish company that offers payment methods for online retailers. Klarna’s customers can pay for goods and services online without a credit card, which makes Klarna an excellent alternative to PayPal and other credit card payments. This means the customer does not need to enter personal data such as name, address, or phone number when making a purchase.

PayPal

PayPal is a secure payment method that allows you to pay online without disclosing your financial information. PayPal works by linking your credit card, debit card, or bank account to your PayPal account. You can then use this account to send or receive payments from anyone with an email address. To pay for goods and services using PayPal, simply choose the “PayPal” payment option when purchasing on any website that accepts it.

Conclusion

We hope this article has helped you understand the importance of offering European alternative payment methods. The popularity of these methods continues to grow and will be even more critical in the future as eCommerce keeps skyrocketing.

FAQs

What are the popular European payment methods?

The popular European payment methods include SEPA Direct Debit, Sofort, Giropay, iDEAL, and EPS. These payment methods are widely used across Europe and offer convenient and secure ways for consumers to make online payments.

What is SEPA Direct Debit?

SEPA Direct Debit is a payment method that allows merchants to collect payments directly from the customer’s bank account. It is available in the Single Euro Payments Area (SEPA), which includes countries in the European Union, as well as Iceland, Liechtenstein, Monaco, Norway, San Marino, and Switzerland.

What is iDEAL?

iDEAL is a popular payment method in the Netherlands. It allows customers to make online payments directly from their bank accounts. iDEAL transactions are processed in real-time and provide a seamless and secure way to pay for goods and services online.