6 Benefits of network tokenization for businesses (beyond security)

Industry

6 Mar 2026

6 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Network tokenization does more than prevent fraud. For subscription businesses, it lifts authorization rates, cuts involuntary churn, and grows customer LTV. Here's the full picture.

TL;DR:

- Network tokenization's security benefits are real, but they're not the main reason scaling digital businesses adopt it.

- The commercial case covers authorization rates, customer lifetime value, PCI compliance costs, international expansion, checkout conversion, and future payment compatibility.

- Each benefit compounds. Better auth rates mean more revenue per billing cycle. Lower involuntary churn extends customer lifetime. Frictionless one-click checkout lifts upsell conversion by up to 20%. Together, Solidgate data shows tokenization can drive up to +42.5% improvement in customer LTV.

gets most of its press for one thing: security. Yes, replacing raw card data with unique digital tokens does meaningfully reduce exposure to fraud and data breaches.

But if that's where the conversation stops, businesses are missing a bigger picture. The benefits of network tokenization for businesses extend well beyond locking down sensitive data.

The numbers frame the problem it solves:

- Global card fraud losses hit $33.41 billion in 2024, according to the .

- 70% cart abandonment rate, with checkout friction and payment trust failures among the leading causes.

- Authorization rates across card-not-present transactions remain well below where they should be.

Tokenization addresses all three. But security headlines tend to get the credit while the commercial outcomes go unnoticed.

This article covers six of those benefits that matter just as much to a business's bottom line.

1. Smoother checkout means fewer abandoned carts

Checkout friction is expensive. According to , nearly two-thirds of shoppers still struggle with manually entering their card details, and 25% abandon carts specifically because checkout is too complex or slow. That's a direct, measurable conversion problem.

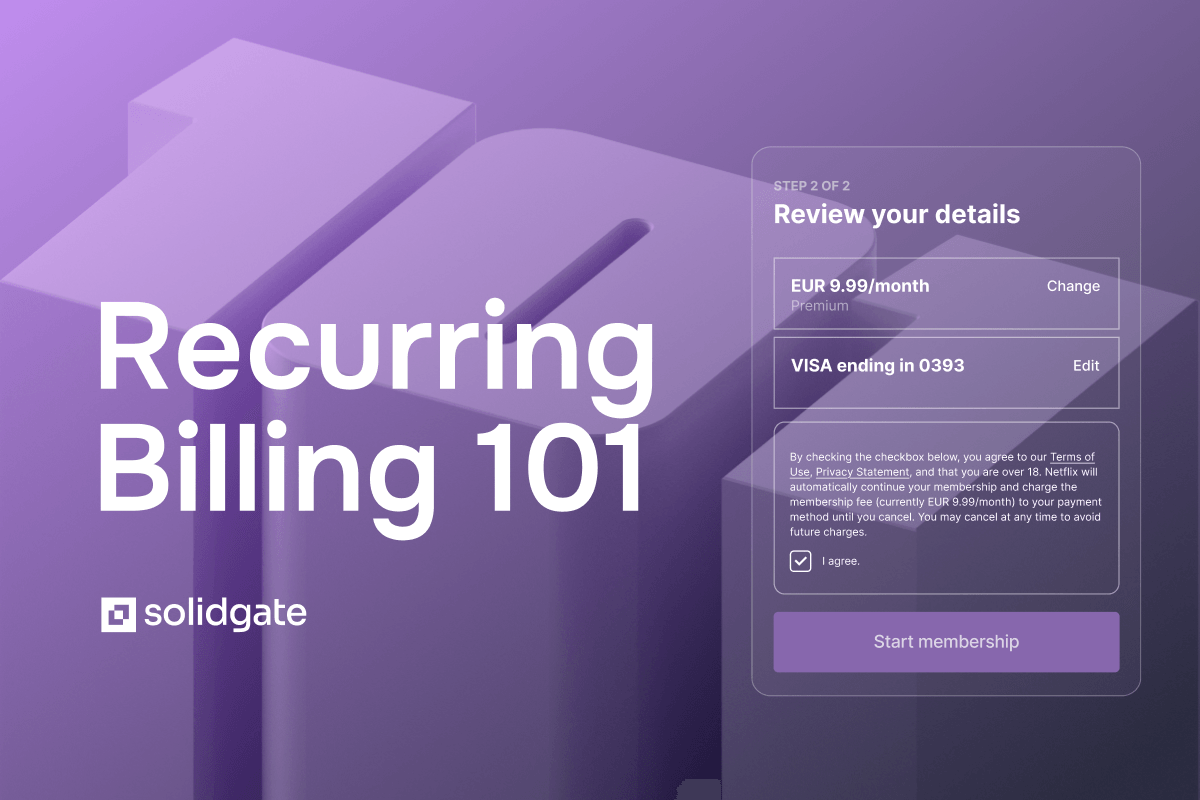

One of the most practical benefits of tokenized payment networks is one-click checkout. There's no prompting to re-enter a card number, no manual form fields to trip over, and no reliance on a customer remembering to update stored details when a card expires.

The token stays valid because the card network manages credential updates in the background automatically.

For subscription businesses, a tokenized one-click flow means that every upsell, upgrade, and add-on offer can convert at a dramatically higher rate than a flow requiring re-entry.

2. Lower fraud directly lifts authorization rates

The relationship between fraud and authorization rates is often underappreciated. When issuers see high fraud risk attached to a transaction, they decline it. That decline isn't always about a stolen card. It's frequently about low confidence in the transaction's legitimacy based on risk signals.

Network tokenization removes a significant source of that risk. A token is merchant-specific and paired with a unique transaction cryptogram, which means even if it's intercepted, it's useless elsewhere. The stolen data can't be replayed at another merchant, so the usual mechanics of card fraud simply don't apply.

The impact on approval rates is well-documented:

- Visa reports roughly a 6 percentage point improvement in transaction completion rates for tokenized payments, alongside a 40% lower fraud rate

- Mastercard data shows percentage points where tokenization is deployed, generating over $2 billion in additional monthly sales for merchants globally

For subscription businesses and e-commerce merchants processing high volumes, even a 2 to 3 percentage point improvement in authorization rates translates to meaningful recovered revenue per billing cycle. This is one of the most direct commercial benefits of network tokenization for businesses that depend on recurring card payments.

3. Higher customer LTV: less churn, more upsells

Network tokenization affects LTV through three connected mechanisms:

Fewer failed renewals

Subscription businesses lose customers every month to involuntary churn due to outdated card details. Based on our survey of 1,200 subscription businesses, the average business risks losing between 5.6% and 8.3% of its subscriber base each month to involuntary churn.

Learn more:

Network tokenization eliminates most of this category of loss with an . When a card is reissued, the card network automatically updates the token. Your stored credential stays valid, the renewal processes, and the customer never knows anything happened.

Solidgate data shows that merchants adopting network tokenization see retention improvements of up to +7.5% as a direct result of token lifecycle management keeping card credentials valid across reissuance events.

One-click checkout unlocks upsell revenue

Once a network token is provisioned on a customer's first transaction, every subsequent purchase – upgrade, add-on, cross-sell – can be completed in a single click with no data-entry requirements.

The contrast with a non-tokenized upsell flow is significant: without a stored token, a customer attempting a $20 add-on faces a full card-entry form with card number, expiry, CVV, billing address, and more.

With a token, they see one button. That friction difference drives a measurable conversion gap. Solidgate merchants using tokenized one-click flows see upsell conversion improvements of up to +20%.

Combined LTV impact

Across acceptance improvement, retention, and upsell conversion, network tokenization drives up to +42.5% improvement in customer LTV for subscription businesses. That's not a security outcome. That's a growth outcome.

4. A smaller PCI DSS footprint and lower compliance costs

apply to every system that stores, processes, or transmits cardholder data. The broader the scope, the more complex and costly the audit.

When a business uses network tokenization, raw card data never touches its own infrastructure. What gets stored is a token: a non-sensitive substitute with no mathematical relationship to the original card number. That shift takes most of a merchant's internal systems out of scope for PCI DSS audits entirely, and the compliance burden moves to the tokenization service provider, which is already a Level 1 PCI-certified entity.

In practical terms, this means:

- Shorter self-assessment questionnaires (often qualifying for SAQ-A rather than the multi-week SAQ-D process)

- Fewer systems requiring quarterly vulnerability scans

- Less internal resource time devoted to annual certification cycles

For businesses without dedicated compliance teams, that reduction in scope is time and money saved.

5. International expansion without added payment complexity

Cross-border card at higher rates than domestic ones. Unfamiliar merchant profiles trigger issuer caution, and inconsistent card data creates processing errors. This has historically made international growth operationally heavier than it needs to be.

Network tokens reduce this friction at the infrastructure level. The issuer doesn't need to evaluate an unfamiliar merchant from scratch. The token and its associated cryptogram establish legitimacy within the payment chain.

Tokenization also simplifies compliance in regulated markets, reducing exposure under GDPR, the Indian tokenization mandate for recurring payments, and similar regional frameworks.

A business processing payments in three markets or thirty benefits from the same authorization lift and compliance simplification, without rebuilding payment infrastructure for each new territory.

6. A payment stack that works with what comes next

Payment technology keeps changing:

- Biometric authentication

- , where AI systems initiate purchases on behalf of consumers

- Stablecoin settlement

- IoT-connected payment devices are

All this is moving from pilot stages to production.

Network tokenization provides the foundation for what's to come. Mastercard's Agent Pay initiative, for example, uses tokenized credentials to allow AI agents to transact securely on behalf of users. The agentic token functions exactly like a standard network token at checkout, so merchants don't need new acceptance infrastructure.

What this means practically: if your token infrastructure is in place today, you're already compatible with the next generation of payment flows. The investment you make now extends forward.

What all benefits add up to

Security is a real benefit of network tokenization. But treating it as the only benefit undersells what tokenization actually does for a business operationally.

The full picture covers checkout conversion, authorization performance, compliance overhead, international payment reliability, and long-term platform flexibility. For scaling digital businesses, these effects compound.

The question isn't whether network tokenization is worth implementing – the data is clear on that. It's how much of this compound effect you're currently leaving unrealized, and what infrastructure you need to capture it.

Network tokenization is a revenue infrastructure decision

Solidgate’s manages network tokens from Visa and Mastercard within a single platform. We help you handle token provisioning, lifecycle management, one-click payment flows, and credential portability across processors.

Combined with smart routing and , it gives subscription businesses and e-commerce merchants the full range of tokenization benefits without direct scheme integrations or fragmented infrastructure.

Across Solidgate merchants, network tokenization has delivered acceptance rate improvements of up to +15%, retention gains of up to +7.5%, and upsell conversion lifts of up to +20%.

with a Solidgate payments expert to see what that looks like for your business case.

Frequently asked questions

It removes friction for returning customers: no re-entering card details, no expired card errors, no manual updates when a card is reissued. When payments work without any action from the customer, repeat purchases complete more reliably, and involuntary subscription churn goes down.

Yes, primarily through two mechanisms: a reduced PCI DSS scope lowers audit complexity and internal compliance overhead, while lower fraud rates mean fewer chargebacks and reduced exposure to dispute fees. Eliminating raw card data storage also removes a category of breach liability that would otherwise require ongoing investment to manage.

Network tokens carry issuer-verified trust signals that improve authorization rates regardless of transaction origin, which reduces the elevated decline rates common in cross-border payments. They also simplify compliance in regulated markets, making it operationally lighter to enter new territories without rebuilding the payment stack for each one.