How network tokenization improves authorization rates: A merchant’s guide

Payments 101

Updated 18 Jun 2026

6 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

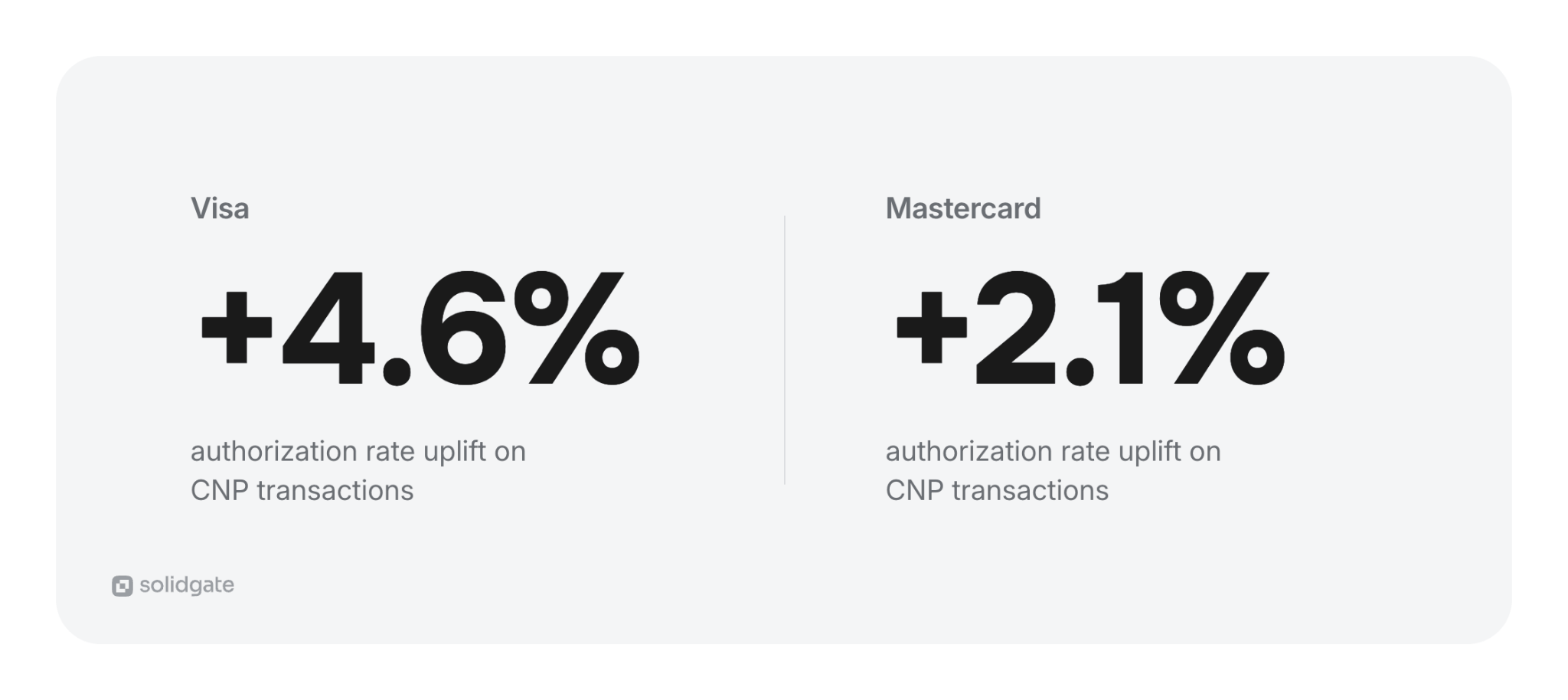

Visa reports 4.6%. Mastercard reports 2.1%. Here's what drives this authorization rate uplift.

According to , network tokens lift authorization rates on card-not-present (CNP) transactions by 4.6% compared to raw card numbers. puts the average at 2.1%.

Issuers approve tokenized transactions more often because the card network pre-validates each token before the authorization reaches them – a stronger signal than a raw PAN provides.

Network tokens are issued by the card scheme to replace the primary account number (PAN). Each token is tied to a specific card and merchant, and updates automatically when the underlying card changes. The result is higher authorization rates, fewer false declines, and uninterrupted billing across the full card lifecycle.

This article covers how tokenization improves authorization rates and reduces fraud in payments – the mechanisms behind the Visa and Mastercard figures, and what merchants see after making the switch.

If you’re new to network tokenization, we recommend starting with our guide on .

TL;DR

- PAN-based CNP transactions fail for three reasons: stale credentials, fraud false positives, and cross-border issuer friction. Network tokenization addresses all three.

- The authorization uplift is scheme-verified: Visa reports 4.6% on CNP transactions, Mastercard reports 2.1%.

- Three mechanisms drive the difference – card network pre-validation, a per-transaction cryptogram that proves legitimate use, and automatic credential updates on card reissuance.

- Solidgate merchants see acceptance rate improvements of up to +15% and retention improvements of up to +7.5%.

How network tokenization improves authorization rates and reduces fraud

CNP for three reasons:

- Credentials go stale when cards are reissued

- Issuers decline legitimate transactions because a raw PAN carries no proof of legitimate use

- Cross-border issuers apply extra scrutiny to unfamiliar merchant profiles

Network tokens address each failure point through a distinct mechanism.

The issuer recognizes where the token comes from

When a network token arrives in a payment request, the card network validates it before passing the authorization to the issuer. It checks that the token was legitimately issued, that domain restrictions are satisfied, and that the cryptogram is valid. The issuer receives a transaction the network has already cleared for trust. With a raw PAN, no such pre-validation exists – the issuer bears the full fraud assessment alone. That difference is what produces the higher approval rate.

Visa and Mastercard data confirm this: network tokens produce 4.6% and 2.1% higher authorization rates on CNP transactions respectively.

The impact is most visible in cross-border transactions. A raw PAN at an unfamiliar foreign merchant arrives without context – the issuer scores it more harshly, because that's the pattern that precedes cross-border fraud. A network token arrives pre-validated by the card network regardless of where the transaction originates. Cross-border declines driven by issuer unfamiliarity decrease as token histories deepen across billing cycles.

Every transaction includes proof of legitimate use

A raw PAN is the same static credential every time it's presented. It carries no proof that the entity presenting it is the legitimate cardholder. When a transaction looks even slightly unfamiliar – a new device, an unusual amount – the issuer's fraud model can tip toward a decline even when no fraud is occurring.

Network tokens address this through a per-transaction cryptogram: a one-time code generated specifically for that transaction and merchant, which expires immediately after use and cannot be replayed. When the issuer receives a tokenized transaction, it sees not just a credential but proof that the token was used legitimately at that specific moment. That proof shifts the fraud signal from uncertain to confirmed. , merchants report a false decline reduction of 5–8%.

Authorization rates and fraud outcomes improve simultaneously. Fewer false declines mean more legitimate revenue captured. Lower fraud exposure means fewer . The two improvements reinforce each other.

The credential stays valid when the card changes

Cards get reissued constantly – after a data breach, on expiry, when a cardholder reports one lost. Most people manage several active subscriptions and don't track which card is attached to each one. When their bank sends a replacement card, they don't update every service. With a PAN-based setup, the next charge can hit a number the issuer no longer recognizes and fails – the customer loses access to a service, often without knowing why.

Network tokens are linked to the underlying card account at the scheme level. When a card is reissued, the token updates automatically. The next billing cycle processes cleanly, with no failed charge and no customer action required. For , this removes one of the primary drivers of involuntary churn – revenue lost to a credential that went stale between billing cycles.

Core insight: Network tokenization improves authorization rates because it gives issuers a better signal at every decision point – a recognized credential source, transaction-level proof of legitimate use, and a credential that's always current.

Authorization uplift by use case

Network tokenization can improve authorization rates across all CNP transactions. Here are some of the use cases:

| Use case | Primary failure mode | Why tokenization has the most impact |

| Subscription and recurring billing | Stale credentials | Cards get reissued between billing cycles. The token updates automatically – the next renewal processes against valid credentials without any action from the merchant or customer. |

| Cross-border payments | Issuer unfamiliarity | A raw PAN at an unfamiliar foreign merchant arrives without context. A network token arrives pre-validated by the card network regardless of where the transaction originates. |

| One-time CNP (e-commerce, digital goods) | Fraud false positives | The per-transaction cryptogram proves legitimate use on every charge. Issuers decline fewer valid transactions flagged as suspicious on limited signals. |

Core insight: Subscription businesses processing cross-border sit at the intersection of the first two failure modes. Network tokenization addresses both in one infrastructure change.

How Solidgate drives the authorization uplift

Direct scheme access, PCI-certified vault infrastructure, and integration logic across every payment flow – most merchants don't have any of these in place.

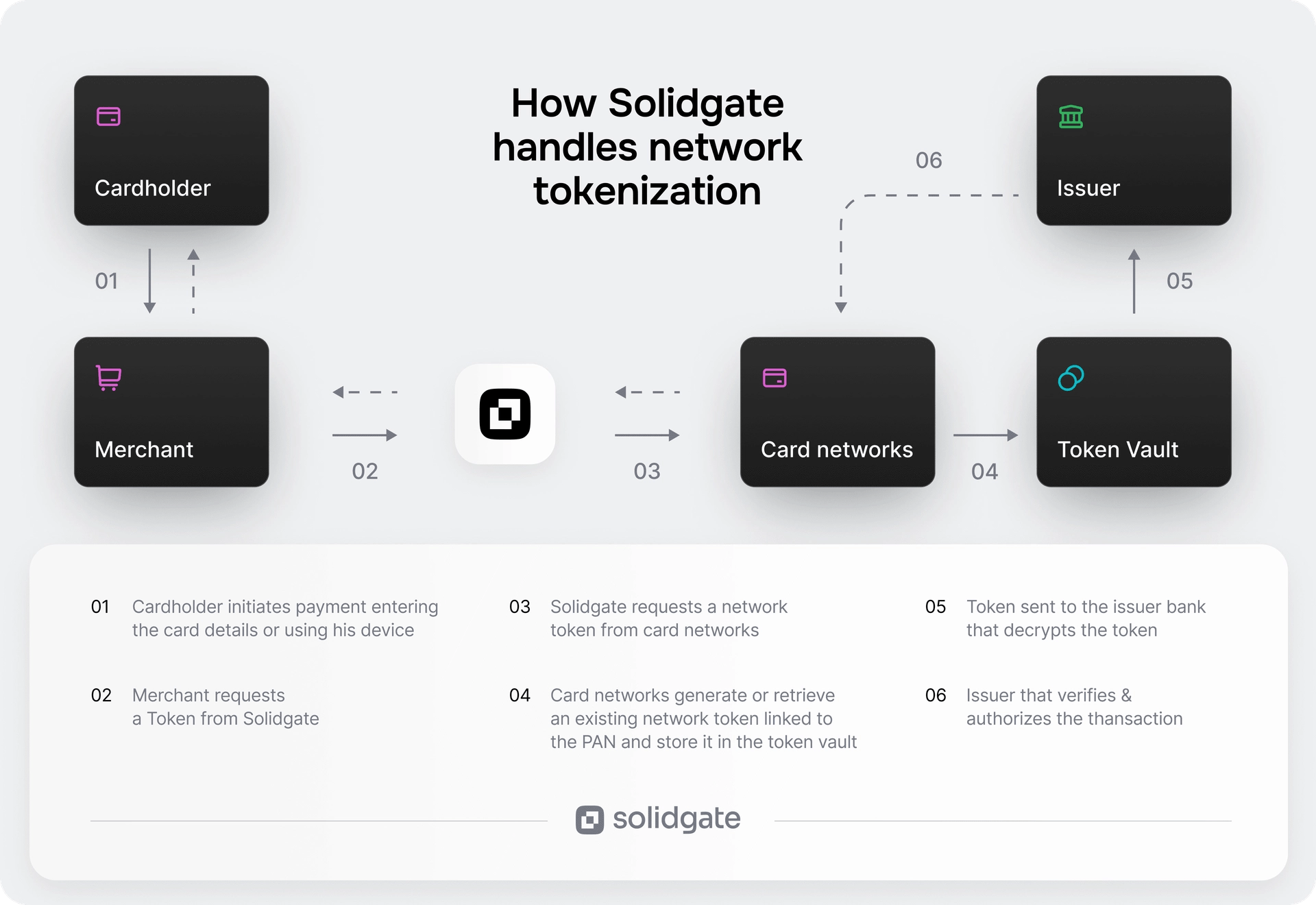

Solidgate is a with direct partnerships with Visa Token Service (VTS) and Mastercard Digital Enablement Service (MDES). It manages the full token lifecycle on the merchant's behalf, across 100+ global providers, acquirers, and alternative payment methods.

Direct scheme partnerships

When a customer pays for the first time, Solidgate provisions a network token from Visa or Mastercard in place of the raw PAN. That token is stored in Solidgate's and used for every subsequent charge – renewals, upgrades, card-on-file purchases. The raw PAN never re-enters the payment flow.

Each charge pairs the token with a unique per-transaction cryptogram. The card network validates both before the authorization reaches the issuer, so the issuer receives a pre-cleared transaction. Solidgate merchants see acceptance rates improve by up to 15%.

Token portability across all your providers

PSP-level tokens work within the ecosystem of the provider that issued them. This means they don't transfer when you add an acquirer, switch providers, or reroute volume.

Solidgate stores tokens at the orchestration layer, above individual acquirers and PSPs, so tokens route to any connected providers without re-tokenization.

For example, when one of Zeely's tier-2 acquiring banks closed, all tokens were preserved on the Solidgate side. The entire recurring payment tail transferred to new acquirers with near-zero loss. Network tokenization combined with acquirer migration, smart routing, and cascading resulted in a +8pp approval rate lift.

→ See the full .

Automatic credential updates

When a card is reissued, the token refreshes automatically through VTS and MDES – handled by a . The next billing cycle processes against valid credentials, with no failed charge and no customer action required.

After MEGOGO implemented VTS/MDES tokenization and account updater across its renewal flows, subscription churn dropped by 5%.

→ See the full .

Across Solidgate's merchant base, retention improvements reach up to +7.5%.

Core insight: Direct scheme partnerships, acquirer-agnostic token storage, and automatic credential updates each address a distinct authorization failure mode – and all three are available through one integration with Solidgate.

Network tokenization as part of a full payment stack

Network tokenization raises the baseline authorization rate but the largest gains come when it runs alongside the rest of the payment stack.

sends each transaction to the acquirer most likely to authorize it, using the network token as the credential throughout. recovers soft declines that persist despite strong credentials. Solidgate's manage risk across the full transaction lifecycle, complementing the per-transaction cryptogram's fraud signal at the issuer level.

Together, these cover the full payment funnel: tokenization lifts the first-attempt rate, routing optimizes the path, and retries recover what slips through.

If authorization rate gaps are costing you revenue, to map your current setup and identify where the improvement would be largest.

Frequently asked questions

Visa reports a 4.6% authorization rate uplift on CNP transactions using network tokens versus raw card numbers. Mastercard reports a 2.1% average increase. These figures reflect the combined effect of card network pre-validation, per-transaction cryptogram validation, and automatic credential updates. Individual merchant results vary based on card mix, transaction type, and geography.

Three mechanisms drive the difference. The card network validates the token – checking legitimacy, domain restrictions, and the cryptogram – before passing the authorization to the issuer, who receives a pre-cleared transaction. Each consumer-initiated transaction also includes a per-transaction cryptogram that proves legitimate use at that specific moment. And the token updates automatically when the underlying card is reissued, so the issuer never receives a stale credential.

Network tokenization reduces fraud through the per-transaction cryptogram – a one-time code tied to that specific transaction and merchant that expires immediately after use. Intercepted tokens have no replay value. Issuers see verified proof of legitimate use on every charge, so fewer valid transactions get flagged as suspicious.

Yes. Visa reports 4.6% on CNP transactions; Mastercard reports 2.1%. The difference reflects each scheme's measurement methodology and data period rather than a fundamental difference in how tokenization works. Both figures measure tokenized versus non-tokenized CNP transactions as an average across participating merchants.

Cross-border transactions fail at higher rates because issuers apply extra scrutiny to unfamiliar merchant profiles. A network token arrives pre-validated by the card network on every transaction, regardless of where it originates. That pre-validation removes the unfamiliarity signal that drives cross-border declines – and the effect strengthens as token history builds across billing cycles.

Network tokenization, , and retry logic each operate at a different point in the authorization funnel. Tokenization raises the first-attempt approval rate by giving issuers a stronger credential signal. Routing directs each transaction to the acquirer most likely to approve it. Retry logic recovers the soft declines that slip through despite strong credentials.

Recent articles