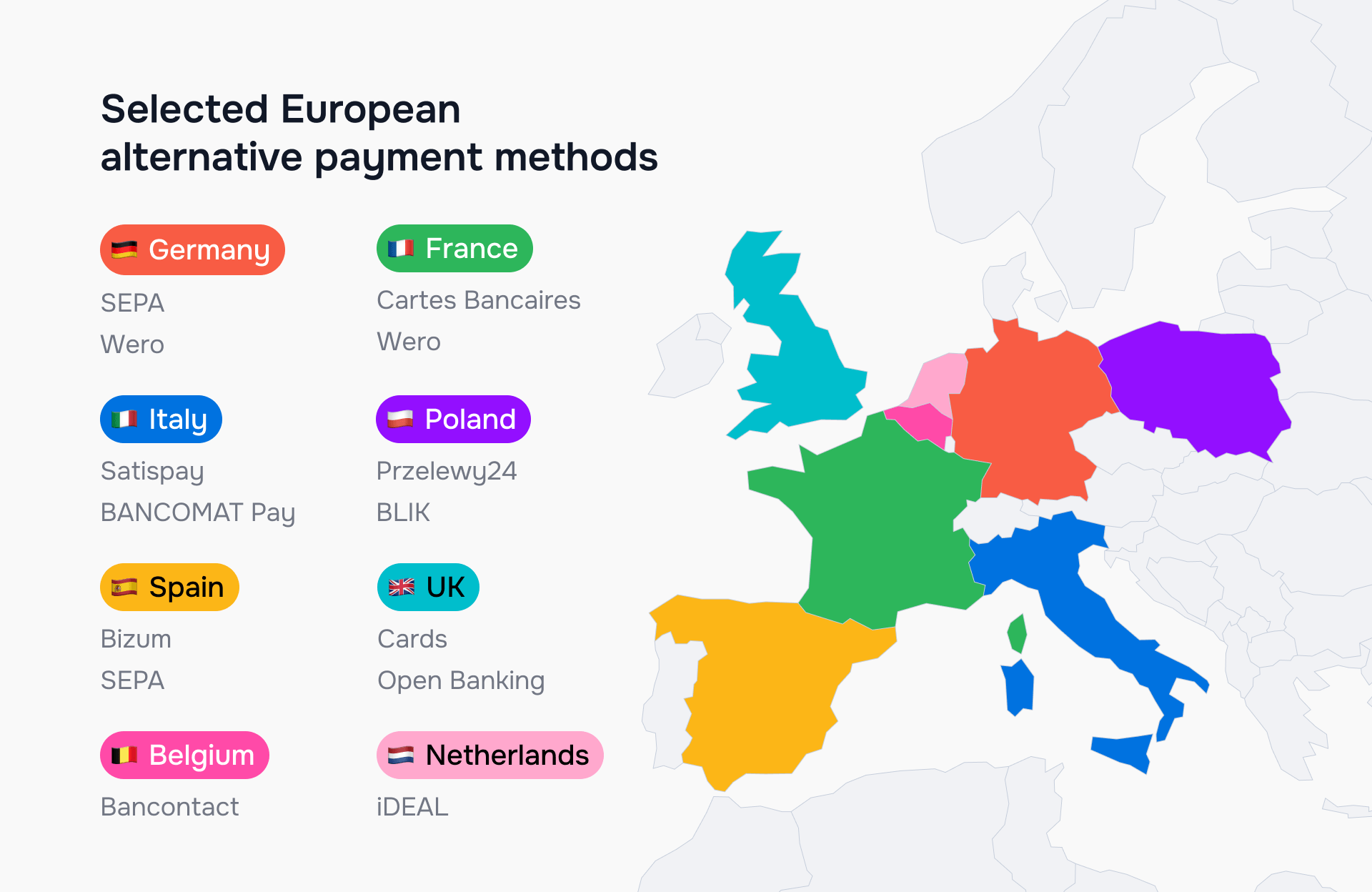

European payment methods: Popular local APMs by country

Industry

Updated 24 Jul 2026

11 min

Andrii Stoikov

Head of Support, Integration, Billing Operations, Solidgate

Cards face strong competition from local payment methods across Europe's biggest markets. This guide breaks down which methods lead in each country and what merchants need to know before expanding.

A checkout built for one European market rarely converts in the next one. Card share of online payments across the euro area fell to, down from 54% in 2019, as local wallets and bank transfers took the difference. Merchants expanding across Europe who launch with cards only are optimizing for a shrinking share of the market.

The cost is visible at checkout. puts the average cart-abandonment rate at 70.22%, with 13% of that abandonment tracing directly to a missing preferred payment method. In Europe, that missing method is rarely exotic – it's iDEAL in the Netherlands, BLIK in Poland, Bancontact in Belgium.

This guide covers the leading European payment methods in eight of the continent's largest e-commerce markets and some of the key players behind each one.

TL;DR

- The right payment method depends entirely on the market: iDEAL covers 70% of Dutch online transactions, BLIK now outpaces cards three to one in Poland, and Bancontact is on virtually every Belgian bank card.

- Local methods are consolidating onto shared rails. Wero has 55 million users across Germany, France, and Belgium, and is absorbing iDEAL next. The EuroPA alliance connects Bancomat, Bizum, MB WAY, and BLIK into an interoperable network targeting e-commerce payments across 13 countries by 2027.

- The complexity of European APM coverage compounds with every market added. A payment orchestration integration handles local method activation, checkout localization, and multi-currency reconciliation in one place – so each new market builds on the same infrastructure.

Why payment preferences vary across Europe

Payment preferences in Europe split along a clear line: markets where banks moved collectively to build domestic rails, and markets where they didn't.

In the Netherlands, Belgium, and Poland, banks created shared payment infrastructure – Bancontact in 1989, iDEAL in 2005, BLIK in 2015 – giving consumers trusted to cards. In markets like the UK and France, no equivalent collective rail emerged, and card networks filled the gap instead.

Consumer trust follows that history. A Dutch shopper trusts iDEAL because they've paid their taxes, energy bills, and online orders through it for years – not because it's technically superior to a card. That behavioral lock-in is what makes a missing local method a checkout problem.

Germany sits in neither camp cleanly. Cards never dominated German online payments the way they did in the UK, but no single bank-owned rail emerged to replace them either. PayPal, invoice-based payment, and SEPA direct debit filled the space – and Giropay, the attempt at a domestic bank-transfer alternative, shut down entirely in 2024.

Core insight: Payment preference in Europe is a product of banking history. Where banks agreed on a shared domestic rail, local methods became the default. Where they didn't, card networks did.

Some of the most popular payment methods in Europe at a glance

Disclaimer: This article reflects a selection of widely-used payment methods across European markets and is not intended to be exhaustive. Payment method availability, market share, and status may change over time. Third-party brand names mentioned are the property of their respective owners and are used for informational purposes only. Solidgate is not affiliated with or endorsed by any of the brands mentioned unless expressly stated otherwise.

Alternative payment methods in the UK

In the UK, cards handle the majority of online transactions. The APM decision here is about layering the right options on top of cards – open banking for cost-conscious merchants, direct debit for subscription billing.

Open banking is the one method worth tracking closely. Payments reached in 2025, up 57% year-on-year.

Open banking payments tend to bypass card networks, which means no interchange fees on those transactions. For merchants processing significant UK volume, that cost difference adds up – especially on higher-value purchases where card fees are a fixed percentage of the transaction.

Pay by Bank

Pay by Bank routes payment directly from a shopper's bank account through open banking, bypassing card entry. The customer confirms inside their own banking app, and settlement runs through the UK's Faster Payments network.

Direct debit

Direct debit is the standard for UK subscription billing. The merchant pulls scheduled payments from a customer's account after a one-time authorization, with settlement over one to three business days. It suits recurring charges rather than one-time checkout.

Core insight: Cards are the default in the UK. Open banking is a cost-efficient addition for merchants already covering card acceptance.

Alternative payment methods in Italy

Italy has no single dominant payment method. Cards and wallets split the market closely, which means merchants need broader coverage here than in markets like the Netherlands or Poland.

Satispay

Satispay is the most established domestic wallet, with users and 450,000 merchants by mid-2026. It links directly to a shopper's bank account and confirms payment through the app, bypassing card networks. For a market with no clear leader, that reach makes it the practical first APM to add.

BANCOMAT Pay

BANCOMAT Pay covers a different segment – cardholders who prefer paying from their bank account without downloading a separate wallet. It connects to Italy's national debit-card infrastructure, letting cardholders pay by phone number or QR code.

Core insight: Italy's split market means card acceptance alone leaves a share of shoppers without their preferred method. Satispay is the practical first APM to add for merchants targeting Italian consumers.

Alternative payment methods in Spain

Spain's payment mix is shifting faster than most European markets. Cards still lead online transactions, but Bizum – originally a peer-to-peer transfer app – closed 2025 with over e-commerce payments.

For merchants, that growth signals Bizum has moved past an optional add-on into a method Spanish shoppers actively expect at checkout.

Bizum

Bizum runs on SEPA Instant Credit Transfer rails, settling directly between bank accounts. At checkout, shoppers authenticate by phone number rather than card details, confirming payment inside their own banking app.

More than 30 million users – close to the entire adult banking population in Spain – are registered, and 111,000 businesses are already integrated into the ecosystem.

In 2026, Bizum launched NFC in-store payments, extending the same infrastructure from e-commerce into physical retail.

Core insight: Bizum's e-commerce growth makes it the clearest APM priority for merchants entering the Spanish market.

Alternative payment methods in Germany

Germany's payment landscape changed in 2024. , once widely used in Germany, was discontinued as a standalone payment method in 2024. entirely by the end of that year, after acquirers lost the ability to migrate to its required new API.

Rather than building a new domestic scheme, German banks chose to back Wero – the pan-European wallet built by the European Payments Initiative.

PayPal, SEPA bank transfers, and digital wallets including Apple Pay and Google Pay remain the established options for German e-commerce in the meantime.

SEPA bank transfers

transfers let shoppers pay directly from their bank account in real time. They run on the same instant-payment infrastructure now mandatory across the euro area under the EU's Instant Payments Regulation.

Wero

Wero settles payments between bank accounts over SEPA Instant Credit Transfer rails. It launched for German e-commerce in November 2025 – making it the newest option here, with a shorter track record than SEPA transfers.

Core insight: Wero and SEPA bank transfers are the practical options for merchants building a German checkout today.

Alternative payment methods in Poland

Poland's e-commerce is dominated by bank-owned payment infrastructure. BLIK – a mobile payment scheme co-owned by six of Poland's largest banks – has become the default checkout method. Online payments via BLIK now outnumber card payments roughly three to one.

Polish consumers are also active cross-border shoppers – from international platforms in 2025. This means foreign merchants without BLIK are competing against platforms that already offer it.

BLIK

BLIK is a mobile payment system that allows customers to make payments with their smartphone. It 1.39 billion transactions worth €48.8 billion in the first half of 2025 alone, including 661.6 million e-commerce payments.

At checkout, shoppers open their banking app, generate a six-digit one-time code, and enter it instead of card details. Because the scheme is bank-owned rather than a third-party wallet, it required no separate app – which is why adoption reached this scale.

Przelewy24 – payment aggregator

Przelewy24 is not a consumer-facing payment method — shoppers don't choose it at checkout. It operates as a payment aggregator in Polish e-commerce, bundling BLIK, cards, and bank transfers behind a single merchant integration.

For merchants entering the market, it removes the need to build direct connections to individual Polish banks and handles reconciliation across all three method types in one place.

Core insight: Poland's payment mix is built around BLIK. Merchants entering the market without it are missing the method shoppers reach for first.

Alternative payment methods in France

France is a card-led market, with Cartes Bancaires (CB) as the dominant domestic scheme. CB covers around of domestic card transactions in France, with 80 million cards in circulation and €750 billion processed annually. Nearly every French bank card carries the CB logo alongside Visa or Mastercard branding.

Wero is the main APM to track for France. It replaced Paylib for peer-to-peer payments in autumn 2024 and has active users in France. E-commerce checkout is in autumn 2026, with in-store payments planned for 2027.

Cartes Bancaires

CB routing applies automatically at domestic checkout for most French-issued cards. Merchants accepting Visa or Mastercard in France are typically already accepting CB – but direct CB acquiring, rather than routing through international scheme rails, can improve and reduce processing costs on domestic transactions.

Wero

At checkout, shoppers authenticate by phone number or email rather than card details – no IBAN required. Once live for e-commerce in autumn 2026, payments will settle instantly between bank accounts with no interchange fees for merchants.

Core insight: France is one of the few European markets where cards remain default.

Alternative payment methods in the Netherlands

The Netherlands is one of Europe's most cashless markets. Bank-based payments dominate online checkout, with iDEAL accounting for the vast majority of transactions. Cards play a secondary role, and credit cards in particular have low acceptance – many Dutch merchants and consumers actively avoid them.

iDEAL

iDEAL accounts for of all e-commerce transactions in the Netherlands, processing more than 1.5 billion payments per year. At checkout, it redirects a shopper to their own online banking environment to confirm payment, then returns them to the merchant once the bank confirms the transfer.

One limitation merchants should plan for: iDEAL carries no mechanism, unlike card payments.

The European Payments Initiative announced iDEAL's transition to "iDEAL | Wero" in October 2025. The underlying rails and checkout experience stay the same through the transition.

Core insight: iDEAL processes the majority of Dutch online transactions. Merchants entering the Netherlands without it are starting at a structural disadvantage.

Alternative payment methods in Belgium

Belgium's payment landscape is more concentrated than most European markets. Bancontact is the dominant method – present on nearly Belgian bank cards and accepted across online and in-store commerce. More than one in two Belgians made at least one mobile payment in 2025.

Bancontact

Bancontact links directly to a Belgian bank account and functions at checkout like a debit card – shoppers either enter their card details or scan a QR code, depending on the device. It is embedded in virtually every Belgian bank card and integrated into most Belgian banking apps, which is why it functions as infrastructure rather than an optional payment method.

Core insight: Belgium's payment mix is built around Bancontact. Merchants entering the market without it are missing the method Belgian shoppers reach for by default.

SEPA, Wero and the pan-European rails

Europe's local payment methods are consolidating onto shared infrastructure. The required all euro-area banks to support instant SEPA transfers from 2025 – the same rails that Wero, Bizum, and iDEAL run on.

Before this regulation, instant A2A settlement was available in some markets but not others. Now it's mandatory across the euro area, which is what makes a single pan-European wallet technically possible.

SEPA

SEPA – the Single Euro Payments Area – covers and lets merchants collect euro payments directly from customer bank accounts. It comes in two forms relevant to merchants:

- SEPA Direct Debit: pulls recurring payments from a customer's account on a schedule

- SEPA Instant Credit Transfer: settles one-time payments in under 10 seconds

The first suits subscription billing; the second is what iDEAL, Wero, and Bizum all settle on.

Wero

Wero, built by the European Payments Initiative, reached users by June 2026. It launched e-commerce checkout in Germany in November 2025 and Belgium in March 2026, with France following in autumn 2026.

Wero has absorbed Giropay and Paylib, is replacing Payconiq, and is gradually migrating iDEAL – with the Netherlands transition running through the end of 2027. For merchants, this means one integration will progressively cover payment methods that currently require separate builds per country.

Pan-European interoperability: EuroPA

A parallel consolidation is underway across Southern and Northern Europe. Bancomat (Italy), Bizum (Spain), and MB WAY (Portugal) are now interoperable through the EuroPA alliance. Users of each scheme can send money across Italy, Spain, Portugal, and Andorra through their own local app, without a separate account.

BLIK (Poland) the same alliance. EuroPA (European Payments Alliance) and EPI (European Payments Initiative) have now to connect their networks, targeting e-commerce payments across 13 countries by 2027. For merchants, this means Wero and EuroPA-linked methods are moving toward a shared layer – integrating one will progressively give access to a much broader European network.

Core insight: Europe's local payment methods are consolidating onto shared rails. For merchants building across multiple European markets, a single integration with Wero or a EuroPA-linked method will progressively cover more countries – without a separate build per market.

How to accept these payment methods across Europe

Accepting European across multiple markets involves three practical decisions:

- Which methods to prioritize per market

- How to integrate them technically

- How to handle reconciliation across different settlement timelines and currencies

The right method depends on where your customers are. A merchant expanding into Poland needs BLIK before anything else. One entering Belgium needs Bancontact. The country sections above map that out.

The integration and reconciliation parts are where most of the complexity sits. EU payment processing solutions vary by market – each local method has its own technical requirements, settlement timeline, and compliance rules. Building them individually means a separate engineering effort per country, plus ongoing maintenance as schemes update their APIs and branding.

A payment orchestration platform – like Solidgate – connects you to multiple APMs and via a single integration. Merchants configure new methods without a separate build per country.

The detects the shopper's location and surfaces the right local method automatically – Dutch shoppers see iDEAL, Polish shoppers see BLIK. Settlement across all connected methods and currencies runs through one consolidated view, reducing the reconciliation overhead that grows with every market added.

Nova Post expanded payment acceptance across 15+ European markets through a single Solidgate integration – with BLIK in Poland, iDEAL in the Netherlands, and Open Banking across Europe live from day one in each market. Average onboarding per EU market was two weeks, with 95%+ approval rates across all markets from launch.

See the full .

Core insight: The integration challenge in Europe is not knowing which methods to add – it's building and maintaining them without compounding engineering work with every new market. A single orchestration integration solves that.

Scale your payment stack with Solidgate

Getting local payment methods live is the first step. Scaling performance across them is a different problem – one that involves:

- Routing each transaction to the best-performing provider per market

- Keeping stored card credentials portable across acquirers

- Recovering failed payments before they become churn

- Managing fraud without adding checkout friction

Solidgate is a that sits across your entire payment stack with routing, tokenization, local method coverage, fraud prevention, and reconciliation in one place. So each new market you enter builds on the same infrastructure rather than adding to the complexity.

If you're mapping which European payment methods and infrastructure layers would move the needle for your expansion, .

Scaled payments across Europe

with 95%+ approval rates

Frequently asked questions

There’s no single best way to pay in Europe. Cards lead in France and the UK, while local alternatives dominate elsewhere: iDEAL in the Netherlands, BLIK in Poland, Bancontact in Belgium, and Bizum in Spain. Checkout coverage needs to match each country rather than assuming one method fits the continent.

There's no single best method – the right one depends on the market. For the Netherlands, iDEAL is close to mandatory. For Poland, it's BLIK. For cross-border European sales, Wero is worth tracking.

SEPA Direct Debit lets merchants collect payments directly from a customer's bank account across the Single Euro Payments Area, which covers the EU plus Iceland, Liechtenstein, Norway, Switzerland, and a few other countries. It suits recurring billing more than one-time checkout, since it settles over one to a few days.

iDEAL is the Netherlands' dominant online payment method, processing more than 1.5 billion transactions in 2025, per the. It redirects shoppers to their own bank's app to confirm payment instantly, with no chargeback protection for merchants. iDEAL is transitioning to the Wero brand starting in 2026.

APMs match checkout to how shoppers in a given market actually prefer to pay, which reduces abandonment tied to unfamiliar payment flows. Many online payment methods in Europe settle faster than cards, carry lower costs, and reach shoppers who don't use or trust international card networks for online purchases.

The main risk is limited chargeback protection – iDEAL, for example, offers none, which shifts dispute exposure onto the merchant. APMs also vary by country, so a method that converts well in one market may have no presence in another, adding integration and reconciliation work for each one added.

APMs improve conversion by removing one of the main causes of checkout abandonment: a missing preferred payment method, which accounts for 13% of cart abandonment industry-wide. Offering iDEAL in the Netherlands or BLIK in Poland meets shoppers with the payment flow they already expect and trust.

Recent articles