Merchant

What is a merchant?

Merchant is a business or individual that accepts card payments in exchange for goods or services. In payments, the term refers specifically to any entity that holds a – an agreement with an acquiring bank that allows the business to process card transactions and receive settlement funds.

Every merchant is assigned a (MID) by their acquirer and categorized by a (MCC) that reflects their primary line of business. Both identifiers are embedded in every transaction the merchant processes and determine how that transaction is priced and underwritten.

Key facts

- Merchant account: the contractual agreement between the merchant and the acquiring bank that enables card payment processing and settlement. Without one, a business can't accept card payments directly.

- MID (Merchant Identification Number): a unique identifier assigned by the acquirer. It links every transaction to the correct merchant account and is required for payment processing.

- MCC (Merchant Category Code): a four-digit code grouping merchants by industry type. The MCC drives interchange rates, card network fees, and acquirer underwriting – a card-not-present subscription business operates under different terms than a brick-and-mortar retail store.

- Primary obligations: compliance with card network rules, PCI DSS security requirements, and the terms of the merchant agreement.

Types of merchants

These categories reflect how a merchant's business model and payment profile affect risk classification and acquiring terms. They aren't mutually exclusive – a single business often fits more than one.

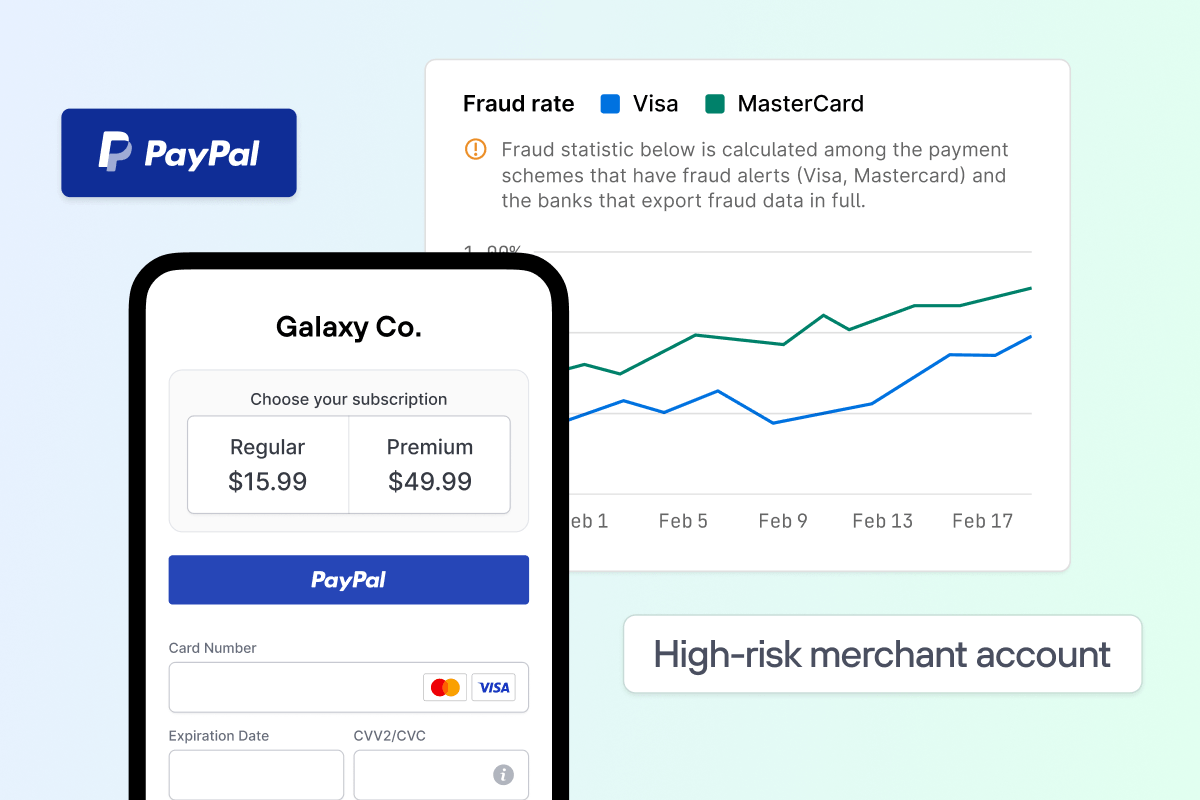

- E-commerce merchant: sells and transacts entirely online; no card is physically present. Higher fraud risk than in-person transactions, which typically results in higher dispute rates and more stringent underwriting requirements.

- Subscription merchant: charges customers on a recurring schedule using stored card credentials. Faces elevated chargeback risk from forgotten subscriptions and failed card updates.

- Marketplace seller: sells through a platform that manages payment infrastructure. The platform's merchant account processes the transaction; the individual seller may not hold a direct acquirer relationship.

- High-risk merchant: classified as higher risk by acquirers based on industry type – such as gambling, travel, or nutraceuticals – or historical chargeback rates. Typically subject to rolling reserves, higher processing fees, and stricter underwriting.

Why it matters

The merchant's MCC, business model, and transaction history determine the terms of their acquiring agreement: the processing fees they pay, any reserve requirements, and the chargeback rate thresholds they must stay under to keep their account in good standing.

Chargebacks are the primary financial risk merchants face in card-not-present environments. When a cardholder disputes a transaction, the issuing bank reverses the funds from the merchant's account pending resolution. Merchants who exceed the card network's chargeback thresholds enter monitoring programs with escalating penalties that can ultimately result in losing the ability to accept card payments.

Not to be confused with merchant of record: a direct merchant processes payments under its own MID and holds chargeback liability directly. A processes payments on behalf of underlying sellers – appearing on the cardholder's statement, absorbing chargeback liability, and handling tax and compliance obligations for those transactions. For the full breakdown, see .