Why credit card tokenization matters for online businesses

Industry

17 Nov 2025

8 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Credit card tokenization is quickly becoming the industry standard for secure and user-friendly online payments. Learn how tokens help decrease payment fraud, improve payment acceptance rates, and boost LTV for online businesses.

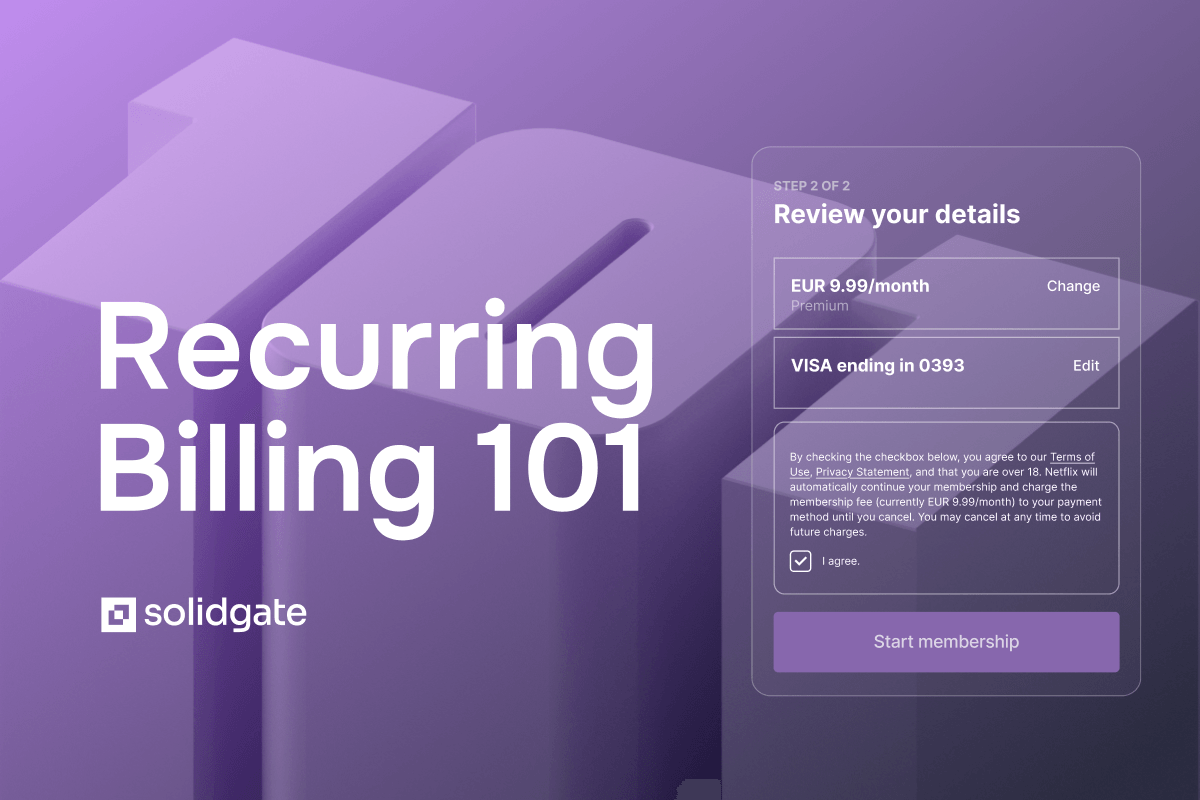

Credit card tokenization used to be something only the largest digital platforms like Netflix and Amazon could access.

Today, more credit card tokenization solutions provide a practical way for growing subscription and e-commerce businesses to protect revenue, improve approval rates, and reduce failed renewals.

At around $200k in monthly processing volume, many teams start to see familiar and recurring issues:

- more that slow down acquisition

- recurring payments are failing due to outdated card data

- stricter fraud controls as volume increases – perfectly legit payments get blocked

Credit card tokenization addresses these issues at the source by replacing vulnerable card numbers with secure network-issued tokens that issuers recognize and trust.

Businesses that adopt tokenization often see better acceptance, lower involuntary churn, and a smoother checkout experience that supports recurring revenue.

To understand why tokenization impacts these metrics so strongly, it helps to start with the basics: how it works, where it creates measurable impact, and what to consider when implementing it in your payment stack.

What is credit card tokenization?

(or network tokenization) is the process of replacing sensitive information, such as the primary account number (PAN), with a non-sensitive placeholder called a token, which is randomly generated and has no intrinsic value.

Here’s a simple example. When a card is added to Apple Pay, the real number is replaced with a device-specific token. The token is context-locked, meaning it works only within the specific environment it was issued for and becomes useless if compromised.

Credit card tokenization takes this concept and applies it across the entire system. For Visa, it’s (VTS); for Mastercard, it’s (MDES). American Express and have their own versions.

Key characteristics of network tokens:

- Linked to the merchant rather than a specific acquiring bank.

- Update automatically when a card expires or is reissued.

- Include additional authentication data that issuers trust.

- Usable across acquirers (when implemented through network services).

- Can't be reverse-engineered into the original card data.

How network tokenization works in online payments

Tokenization fits into the existing card-not-present (CNP) flow with only a few structural changes. Here is what happens at each stage.

Step 1. Cardholder → Tokenization Service

When a cardholder enters their payment details, the tokenization service (e.g., payment processor) converts the PAN information into a network token and securely stores it in a token vault. This vault connects directly to networks such as Visa and Mastercard.

Step 2. Merchant → Acquirer

Instead of transmitting actual card data, the acquirer receives the network token. This reduces the risk of sensitive data being exposed during processing.

Step 3. Card network processing

The network token stays within the card network’s secure infrastructure; the actual PAN isn’t exposed. The token is then updated automatically when the card data is renewed, replaced, or compromised.

Step 4. Issuer verification

When the issuer receives the tokenized transaction, they trust it more because it comes from the payment network’s vault. This leads to fewer antifraud checks and faster processing compared to transactions using real card data.

This flow offers several significant advantages beyond basic data protection.

What are the top benefits of network tokenization for businesses?

Implementing tokenization supports business growth on several fronts: higher approvals, better retention, and smoother repeat purchasing for cross-sells and upsells. Here are the results our clients saw firsthand from implementing the Solidgate .

Lower fraud rates

Visa reports that CNP transactions using network tokens see fraud levels drop by about 40%. For a business processing around $20 million a year with a 0.8 percent fraud rate, that reduction prevents roughly $64,000 in direct fraud losses.

Here’s why: credit card tokenization makes it incredibly difficult for fraudsters to misuse stolen payment information. Even if tokens are intercepted, they can’t be used for unauthorized transactions outside the merchant’s system.

Network tokenization also reduces your PCI DSS compliance scope. When sensitive card data is replaced with tokens, many of the complex no longer apply to those parts of your environment.

As a result, you have fewer systems to secure, so you can meet security standards with less effort.

Improved payment acceptance

A healthy acquisition funnel depends on initial payment approval. But this approval relies on meeting the issuer's anti-fraud standards, which can be very stringent.

Tokenized transactions carry lower fraud risk by design – tokenized credentials meet issuer security expectations, which often leads to fewer false declines.

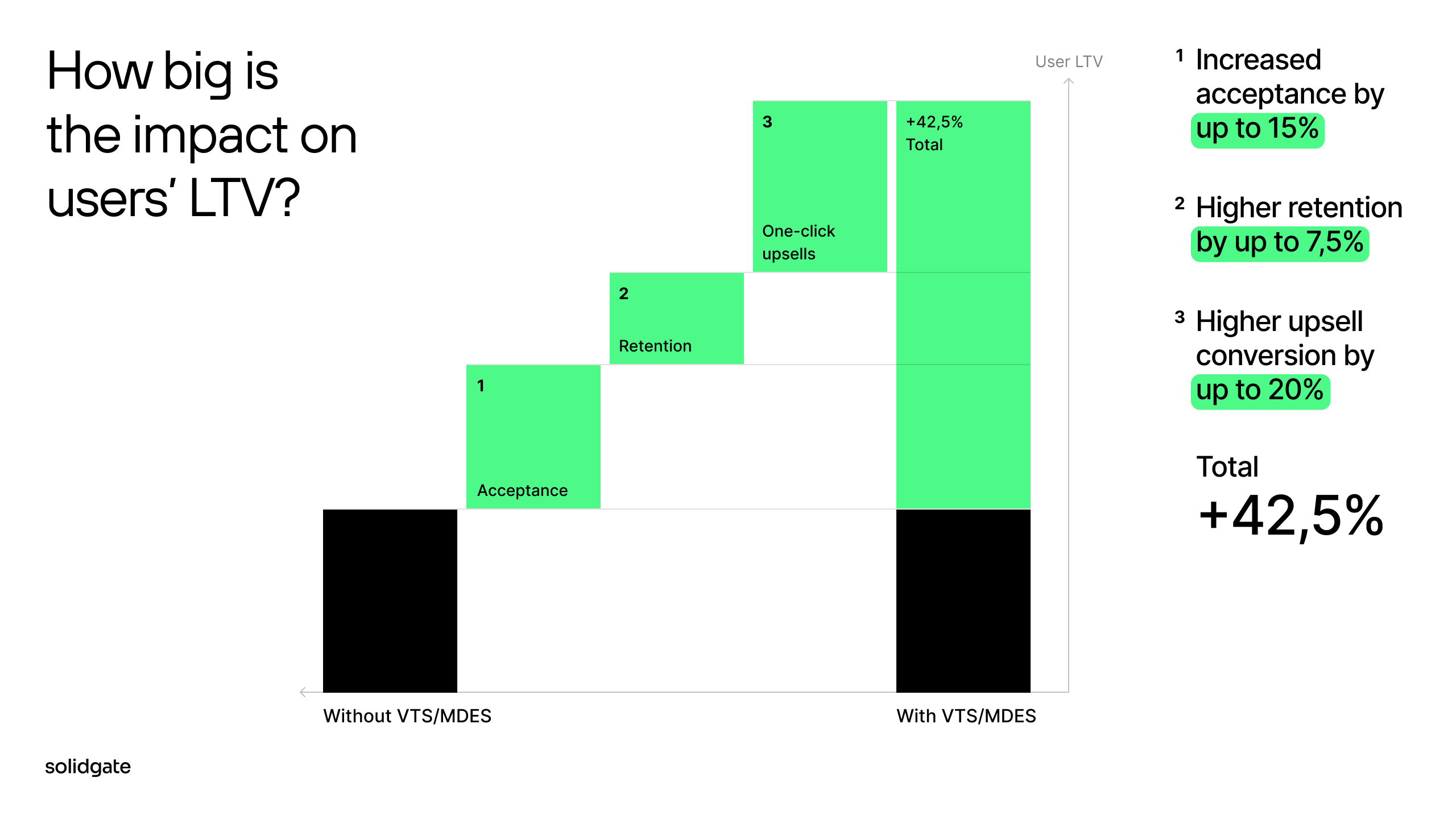

Our clients in customer subscription services see up to a 15% increase in after implementing network tokens paired with strategies.

Lower involuntary churn and higher LTV

Based on our of 1200 subscription businesses, they lose up to 9% of customers each month to involuntary churn caused by failed payments.

Beyond false fraud signals, many failures happen because card data changes over time:

- The card may have been reissued due to upgrades or theft

- The original card has expired

- The cardholder’s account was closed or upgraded

- The customer’s name or changed

Credit card tokenization provides that can automatically get customers’ new card data. This prevents many recurring payment failures and has delivered up to a 7.5% increase in retention for some merchants.

Seamless upsell and cross-sell with one-click payments

Network tokens make the checkout experience much smoother. Once the VTS/MDES token is created on the 1st transaction, it can be used for subsequent transactions with virtually no data entry requirements.

This enables a one-click checkout flow, which is invaluable for seamless upsells, cross-sells, and repeat purchases, resulting in up to a 20% increase in conversions.

Top use cases for credit card tokenization: subscriptions, e-commerce, and mobile payments

Network tokenization is now used across a wide range of online payment flows, with subscriptions, e-commerce, and mobile payment services leading the charge.

Subscription services

Subscriptions are first in line to benefit from network tokenization.

A simple example: subscription businesses rely on payment credentials that remain valid for long periods. Tokens are linked to the business rather than a specific acquiring bank, which keeps recurring payments consistent even if the merchant changes providers.

That’s why services like Netflix use network tokenization. A token isn't tied to a specific bank – it’s linked to the business itself. This eliminates the so-called vendor lock-in, meaning the client isn’t dependent on any particular acquiring bank.

Add to that a lift in authorization rates and customer LTV of 2 to 15%, and the business case for implementing network tokenization for subscriptions becomes very clear.

E-commerce

E-commerce businesses were early adopters of tokenization because they handle large transaction volumes and face continuous fraud pressure.

Tokenization lets retailers offer saved payment methods and one-click checkout without storing sensitive card data. When customers save their payment information for future purchases, the system stores tokens instead of actual card numbers.

This approach enables the convenience customers expect while maintaining the security your business needs.

Mobile payments

Mobile payment platforms like and rely heavily on tokenization technology. When users add their credit cards to these digital wallets, the services generate unique tokens for each card-device combination.

These tokens are used for all subsequent transactions, ensuring that the actual card information never leaves the secure digital wallet system.

Mobile tokenization offers additional benefits:

- Device-specific security: Each device receives unique tokens

- Biometric authentication: Fingerprint or face recognition adds extra protection

- Contactless convenience: Fast, secure payments without physical cards

- Multiple card support: Users can tokenize

- Merchant compatibility: Works with existing payment terminals.

How to choose a credit card tokenization solution

Selecting a tokenization solution is a strategic decision that affects security, conversion, and long-term flexibility. A few factors carry the most weight.

- Secure architecture: Ensures sensitive data never enters your environment and supports network-level tokens with reliable vaulting.

- Compatibility with your current payment stack: A good token should work across acquirers, gateways, and regions without forcing changes to your existing setup. Format-preserving tokens and seamless routing support help you avoid operational friction as volumes grow.

- Issuer trust and acceptance impact: Network tokens often lead to fewer antifraud checks and more approvals. Prioritize tokenization solutions that integrate directly with Visa and Mastercard token services, since this usually improves renewal rates and overall acceptance.

- Scalability for recurring and stored-credential models: Subscription businesses rely on token stability. The service you choose should support long-term token lifecycle management, reliable refresh mechanisms, and consistent behavior across retries and recurring transactions.

- Control and portability: Your tokenization layer should avoid vendor lock-in. Tokens tied to your business rather than a single acquirer give you the freedom to switch providers, add redundancy, and optimize routing without disrupting the customer experience.

- Compliance footprint: A well-designed tokenization solution reduces your scope. This lowers operational overhead and lets your team focus on scaling rather than maintaining a heavy compliance burden.

This set of factors helps you evaluate tokenization solutions through the lens of security, flexibility, and long-term performance – core priorities for any business operating at scale.

Note: Tokenization works best when paired with a strong layer that can route transactions across acquirers without breaking token continuity.

Bringing tokenization into your payment strategy

Tokenization removes sensitive data from your systems, reduces fraud exposure, and improves the stability of stored-credential payments.

For businesses that rely on renewals, retries, and long customer lifecycles, it offers measurable gains in acceptance and retention. As grows more complex, tokenization becomes a practical way to keep payment operations secure and adaptable.

If you want a clearer picture of how tokenization service can lift approvals, cut failed renewals, and make your revenue more predictable, we can walk you through it. and we’ll show what this could look like in your setup.

Glossary

- PAN (Primary account number) is the actual credit card number printed on the card.

- Network tokenization is tokenization performed by payment networks like Visa, Mastercard, Amex, and Discover.

- VTS () is Visa’s tokenization infrastructure for creating and managing network tokens.

- MDES (Mastercard Digital Enablement Service) is Mastercard’s equivalent tokenization service for issuing Digital PANs.

- Digital PAN is a lifecycle-managed token that updates automatically when the physical card changes.

- Stored credential / Recurring credential – card details saved for future billing or subscription payments.

- CNP (Card-not-present) transaction is a payment where the cardholder is not physically present – online, in-app, or subscription.

- Token vault is a secure environment where network tokens are stored and managed.

- Vendor lock-in – dependency on a single PSP or acquirer.

Frequently asked questions

Tokenization protects customer information by replacing sensitive credit card data with meaningless tokens. Even if cybercriminals breach a system using tokenization, they only find tokens that cannot be used to make unauthorized purchases or reveal the original card information. The actual credit card data is stored separately in a highly secure vault system that criminals cannot access through typical data breach methods.

Yes, credit card tokenization is not only compliant with PCI DSS but also helps businesses achieve compliance more easily. When properly implemented, tokenization reduces the scope of systems that must meet strict PCI DSS requirements because those systems no longer store sensitive card data. This simplification makes compliance less expensive and complex for merchants while maintaining the security standards that PCI DSS is designed to enforce.

Absolutely. Mobile payment platforms like Apple Pay and Google Pay rely extensively on tokenization technology. When you add a credit card to these digital wallets, the service generates unique tokens used for all transactions.

This approach enables the convenience of mobile payments while ensuring that your actual card information never leaves the secure digital wallet system, providing excellent security for contactless and mobile transactions.

Tokenization strengthens payment security in several ways. The points below highlight the most impactful mechanisms that reduce fraud risk in online transactions.

- Reduced attack surface - Sensitive data is stored in fewer places.

- Useless stolen data - Tokens have no value outside the secure system.

- Immediate fraud detection - Suspicious token activity can be blocked in real-time.

- Invalid tokens - Stolen tokens fail when used elsewhere.

- Transaction tracking - All token usage can be monitored and analyzed.

- Rapid fraud detection - Unusual token patterns trigger immediate alerts.