What is a payment orchestration layer and how does it work?

Industry

Updated 26 Jun 2026

9 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

Your PSPs process payments. The orchestration layer decides how, when, and through whom. We break down the architecture – and what it actually does for authorization rates and subscription retention

When you begin selling in international markets, becomes complex fast. A single solution can't sustain healthy authorization rates across regions on its own.

The challenge compounds as you scale. A company starting with Stripe for card payments may add PayPal for wallets, SEPA for European bank transfers, and Alipay for Asian markets. Each integration requires separate API work, a distinct security review, and ongoing maintenance.

Payment orchestration layer simplifies this process by providing a single point of contact to manage relationships with multiple gateways and providers.

This guide covers the architecture of the orchestration layer: what's inside, how it moves authorization rates and subscription retention, and when building versus buying makes sense.

TL;DR

- A payment orchestration layer sits above your payment service providers (PSPs) as the control plane – managing routing, tokenization, fraud screening, and reporting through a single integration.

- Smart routing, local acquiring, network tokenization, and adaptive fraud controls typically deliver a 2–4% authorization rate lift immediately after implementation.

- Subscription businesses that enable network token-based card updater services see up to 7.5% higher retention, as token credentials survive card expiry and reissuance.

- Every PSP you connect without an orchestration layer multiplies your PCI scope, token overhead, and routing complexity.

- Building makes sense only when payments infrastructure is your core product; most businesses processing $300k+ monthly recover the investment quickly by buying.

What is a payment orchestration layer?

A payment orchestration layer is the software tier that sits above your PSPs and acquirers. It controls how every transaction moves through your stack:

- Which acquirer handles it based on BIN, corridor, card type, and real-time provider performance

- How a gets retried

- How card data is stored

- How outcomes get reported across all your providers

For a broader look at the category, see our guide on.

Where the orchestration layer sits in the payment stack

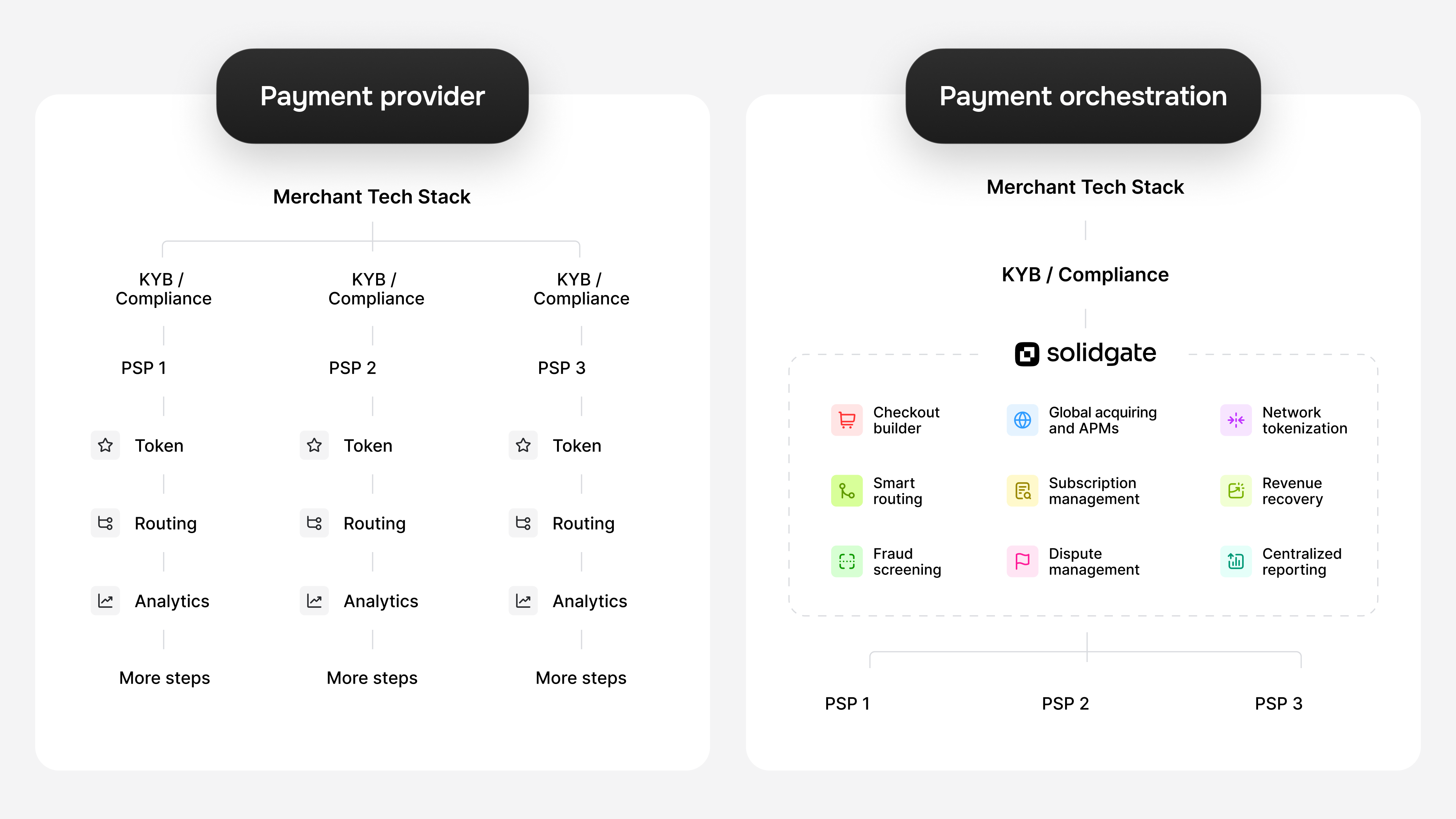

The payment stack has three tiers with orchestration sitting in the middle:

- Your business – tech stack, product, and billing logic

- The payment orchestration layer – connectivity, routing, tokenization, fraud, and reporting

- Your PSPs and acquirers – payment processing and settlement

Core insight: Every PSP you add without an orchestration layer multiplies your compliance, token, and routing overhead. The orchestration layer collapses all of it to one tier – one review, one token store, one place where routing decisions are made. Your PSPs stay beneath it, processing on their own rails.

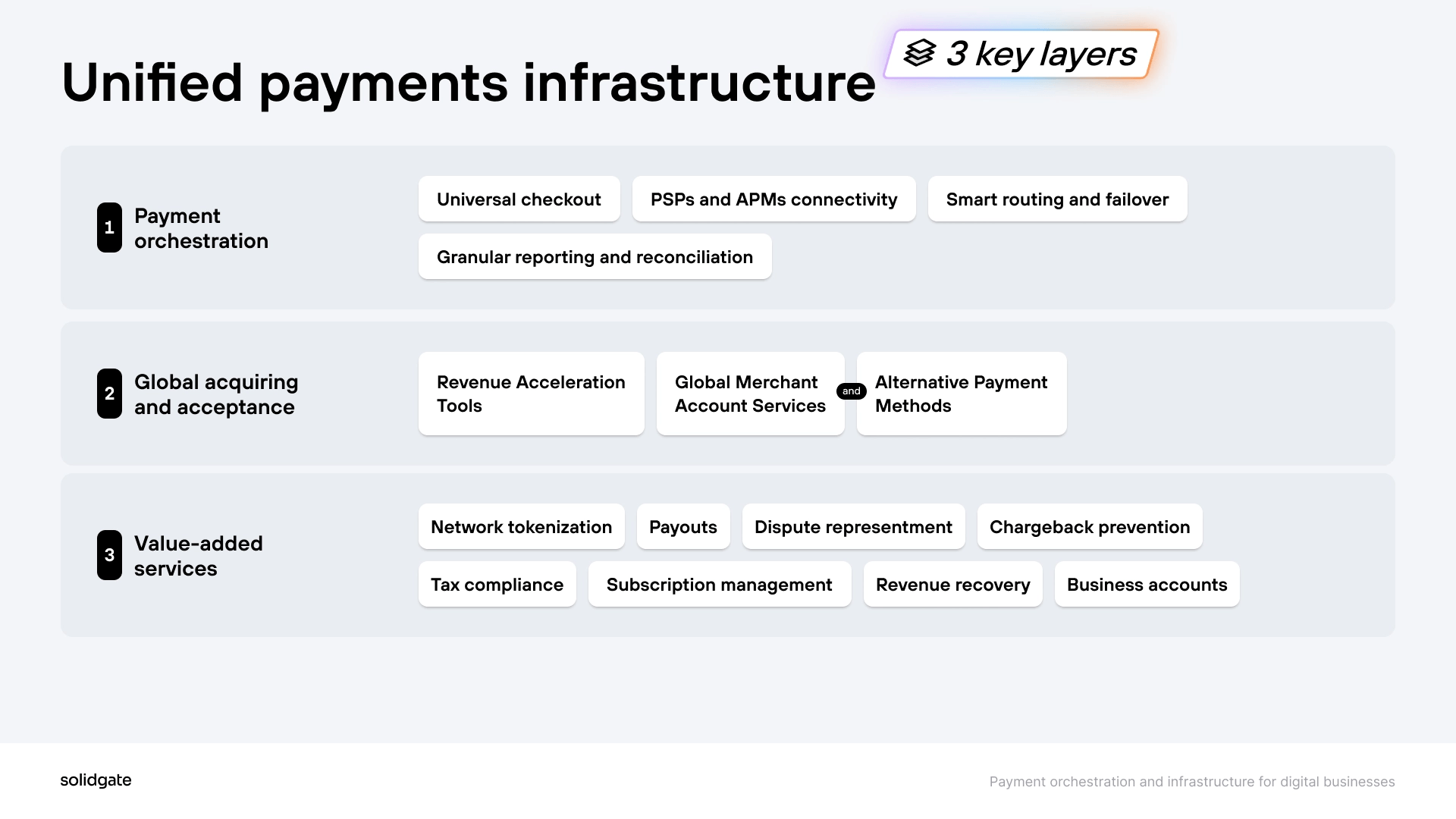

What's inside a payment orchestration layer

The orchestration layer has four core components:

Provider connectivity

The orchestration layer connects to your payment providers through a single integration point. Once connected, the routing engine can direct transactions to any acquirer or alternative payment method (APM) in the network. Adding a new provider doesn't require a separate integration project – it activates within the existing framework.

Routing and failover engine

Routing layers read BIN (Bank Identification Number), issuer country, amount, currency, and customer history in real time. It selects the best-fit acquirer before each authorization attempt. Rules can be static ("always route LATAM transactions to Ebanx") or dynamic ("route to the acquirer with the best approval rate for this BIN"). If the primary acquirer is unavailable, failover logic moves the transaction to the next configured provider automatically.

Checkout builder

The checkout builder covers three types:

- A hosted checkout page (a full page the platform hosts)

- An embeddable (sits within the merchant's own page)

- (shareable URLs that take the customer directly to payment)

All three read the customer's location, device, and currency – then surface the payment methods that match without requiring configuration changes at the individual PSP level.

Reporting and reconciliation

The reporting layer pulls transaction data from every connected provider into a single dashboard. It covers authorization rates by acquirer, corridor, and payment method – alongside chargeback ratios and subscription KPIs like MRR and churn. No exporting from individual PSP portals, no manual reconciliation.

Full-stack platforms like Solidgate extend the orchestration layer with two additional layers.

Global and acceptance provides acquirer relationships the merchant doesn't have to bring themselves.

With pure orchestration, the routing engine can only direct transactions to acquirers you've already onboarded – meaning a separate KYB review, contract, and MID provisioning for each one before any traffic flows through that route.

With acquiring built into the platform, merchants launch on local rails immediately, with one onboarding and one contract. External acquirers can be layered in later when volume or commercial terms justify the additional setup.

Value-added services compound the core routing and checkout capabilities into direct revenue impact:

- Network tokenization – replaces raw card data with Visa/Mastercard network tokens

- Subscription management – handles the full billing lifecycle: trials, billing calendars, plan upgrades and downgrades, renewal scheduling, and cancellation logic

- Revenue recovery – smart dunning retries failed renewals on a tiered schedule, accounting for time zone, issuer behavior, and decline code

- Chargeback prevention – notify your team before a chargeback files, giving you a response window before it escalates

- AI-powered dispute representment with automatic evidence generation and submission to easily lost to chargebacks

- Tax compliance – calculates, collects, and reports taxes based on customer location, transaction type, and applicable rates across jurisdictions

- Payouts – outbound payment flows to merchants, partners, or sellers within a marketplace structure

- Business accounts – financial account infrastructure for platforms managing funds on behalf of their users

Core insight: The four core components handle connectivity, routing, checkout, and reporting. The value-added services are what turn that infrastructure into a revenue performance system.

How a payment orchestration layer improves authorization rates

Most Solidgate merchants report an immediate 2–4% authorization rate lift after implementing the orchestration layer. The improvement comes from four mechanisms that work independently and reinforce each other.

Local acquiring removes the cross-border risk signal

When a transaction routes through a foreign processor, the issuer recognizes it as cross-border and applies stricter fraud criteria, triggering more declines. But when the same card routes through a local acquirer – one the issuer treats as domestic – that risk signal disappears.

For example, your rate may hover at 74% in the Netherlands, while showing a strong 85% in the US. For companies processing over $15-20M a year, these drops in acceptance will quickly show up on your balance sheets.

Failover and smart retries prevent single-acquirer dependency

With an orchestration layer, you can easily set up customized rules that direct payments to acquirers most likely to approve them in a given region. If the chosen provider declines or fails to process the transaction, failovers automatically re-route the payment to an alternative provider.

If a soft decline occurs, smart retry logic helps recover as many sales as possible by intelligently retrying payments at the best times.

Routing customization in Solidgate Hub.

Network tokenization earns higher issuer trust

carry a different authentication signal than standard card-not-present transactions. Instead of the merchant sending raw card data, authentication comes from Visa or Mastercard's own token vault – a source issuers trust by default. Our clients in subscription services see up to a 15% increase in payment acceptance after rolling out network tokens for card-on-file transactions.

Adaptive fraud management cuts false declines

Orchestration providers integrate fraud detection engines, adaptive 3-D Secure authentication flows, , chargeback prevention, and risk scoring. This allows you to protect your revenue and reputation while still approving as many legitimate transactions as possible.

High-risk cards trigger a 3DS flow for extra verification, while trusted customers can pay in one click.

Core insight: The orchestration layer lifts authorization rates by changing what the issuer reads on every transaction. Local routing, network tokenization, and adaptive fraud rules each remove a different reason to decline.

Why scaling businesses adopt a payment orchestration layer

The success for subscription-based businesses lies in strong acquisition, retention, and expansion. Here’s how an orchestration layer helps with all three.

Localized checkout for higher conversion

According to a , 8% of respondents abandoned checkout because their card declined. A further 10% left because the site didn't offer their preferred payment method.

Among the key orchestration layer benefits for clients is checkout customization. You can offer customers from different regions their preferred payment methods by quickly adding and testing them in your checkout. In the US, it’s PayPal; in Brazil, it’s SmartPix; in Poland, it’s BLIK; in China, it’s AliPay, and so on.

You won't have to spend months building integrations from scratch, as you would without orchestration. Adding new payment methods this way takes days, at most weeks, requiring minimal development efforts from your side.

This speeds up your time-to-market, allowing you to test checkout performance and adjust your strategy on the go.

See how we helped into North America, LATAM, MENA, and SEA by adding local payment methods without rebuilding their integrations.

Lower involuntary churn and higher LTV

Based on our of 1200 subscription businesses, they lose up to 9% of customers each month to involuntary churn caused by failed payments.

Beyond false fraud signals, many fail because card data changes over time:

- The card may have been reissued due to upgrades or theft

- The original card has expired

- The cardholder’s account was closed or upgraded

- The customer’s name or changed

Network tokenization provides services that automatically update customers’ new card data. This prevents many recurring payment failures and has delivered up to a 7.5% increase in retention for some merchants.

Cost control at scale

Exposure to a single vendor provides little room for cost control or negotiation. Payment providers offer different rates depending on transaction type, volume, geography, and even market conditions, which can shift over time.

Routing each transaction to the lowest-cost acquirer – local vs. cross-border, high-ticket vs. low-ticket – reduces fees without affecting authorization rates. For high-volume merchants, even a 1% reduction in processing fees can lead to hundreds of thousands of $ saved each year.

The orchestration layer also cuts operational overhead. Instead of maintaining separate integrations with multiple PSPs and running manual reconciliation across each, your team manages one connection. Finance gets unified reporting across all providers and ops gets automated matching.

Core insight: Better checkout conversion brings more subscribers in. Lower involuntary churn keeps them longer, and cost routing improves the margin on every transaction in between.

Build vs. buy a payment orchestration layer

Some engineering teams consider building orchestration in-house. Here's an honest read of what that decision involves.

| Build | Buy | |

| Upfront cost | 6–12 months of engineering time | Integration fees + platform subscription |

| Ongoing cost | Dedicated headcount for PSP maintenance, API updates, PCI scope | Transaction-based or monthly pricing |

| Speed to market | Slow – each new PSP or APM is a new project | Fast – new connectors can activate in days |

| Routing flexibility | Full control at every level | Configurable within platform limits |

| Best for | Payment infrastructure as a core competitive product + large enterprises | Payments as infrastructure, not product |

When to buy

Think about buying a payments orchestration layer, when:

- You're scaling into new markets faster than your team can build PSP integrations

- Involuntary churn is already showing up in retention metrics

- Reconciliation across multiple PSPs is consuming finance hours that belong elsewhere

The threshold most subscription businesses hit is around $300k–$1M in monthly processing volume. Below that, a single PSP usually handles the load without meaningful friction. Above it, routing complexity, authorization rate variance across corridors, and operational overhead typically justify the switch.

When to build

Building makes sense when payment infrastructure is your core competitive differentiator – the routing logic or checkout experience itself is the product. This applies to payment companies, large financial platforms, and businesses at $500M+ TPV with genuinely bespoke requirements.

If that's your situation, know what you're committing to. The integration work is only the start. Each PSP connection requires its own API integration, security review, and token store. compliance must be maintained across every connection. When a PSP changes its API (which happens regularly), your team patches it. When you add a new market, your team builds the integration from scratch.

A basic multi-PSP setup with a shared token vault takes six to 12 months to build and requires dedicated headcount to maintain. That's before smart retry logic, network tokenization, , or unified analytics.

Core insight: Build if payments is your product. Buy if payments support your product.

Scaling your subscription business with a payment orchestration layer

Global subscriptions face very specific payment challenges:

- Adapting to local payment preferences

- Managing transaction declines and authorization rates

- Managing recurring payments

- Staying compliant with regional laws

It's a lot to manage, particularly if your payment infrastructure isn't optimized for growth.

All-in-one orchestration layer simplifies these complexities by streamlining your payment processes and making them more efficient. By centralizing everything on a single platform, you can ensure smooth transactions, higher approval rates, and better customer retention, while keeping costs in check and reducing fraud risk.

At Solidgate, our is built to support the growth of subscription businesses.

If you’re looking to expand your payment options, improve payment acceptance, and simplify operations, – we’ll be happy to show you how it works.

Frequently asked questions

A payment orchestration layer is middleware that sits between your business and your payment providers. It manages routing, tokenization, fraud screening, subscription billing logic, and reporting across all connected PSPs through a single integration – replacing direct, siloed connections to each provider.

When a transaction initiates, the routing engine reads the card BIN (Bank Identification Number), issuer country, amount, and customer history. It selects the best-fit acquirer before the authorization attempt – based on your configured rules. If that acquirer declines or goes down, failover logic re-routes to the next provider automatically.

Full-stack platforms like Solidgate also store card data in a central vault. When a card is reissued or expires, recurring payments keep processing without the customer re-entering details. Every outcome – authorization rate, chargeback, settlement – feeds back into a single reporting dashboard across all connected providers.

Orchestration layers simplify PCI DSS compliance by centralizing data security across all connected providers. Instead of maintaining a separate compliance scope for each PSP integration, merchants manage one through the orchestration layer. Network tokenization further reduces PCI scope: raw card numbers are replaced with tokens at first capture and never stored or transmitted in raw form afterward.

Orchestration layers can be particularly useful for subscription businesses. They help manage recurring payments more efficiently, reduce churn, and ensure payments are processed smoothly, which can improve overall customer retention.

For e-commerce businesses, especially those with a global presence, orchestration simplifies the integration of different payment methods, reduces declines, and enhances the overall checkout experience. This makes it easier to manage payments across regions without the complexity of multiple integrations.

Enterprises scaling internationally can also benefit from orchestration, as it connects to a wide range of providers and payment methods. This simplifies cross-border payment processing and reduces the need for separate integrations in each region.

Finally, businesses dealing with high transaction volumes or operating in regulated industries can leverage orchestration to streamline fraud detection, compliance, and reporting, reducing risks and improving operational efficiency.

There are a few key areas where you can save money with an orchestration layer. First, it cuts down on development costs. Instead of building out individual integrations with each payment provider, you only need to integrate once with the orchestration layer.

Then, it helps with transaction fees. The layer routes payments to the most cost-effective processors, which means you're not overpaying for transactions.

You’ll also see fewer payment declines, thanks to intelligent payment routing and , improving your authorization rates.

Plus, it integrates fraud detection, which means fewer chargebacks and manual handling, saving on those costs too. On top of that, it reduces operational overhead by automating tasks like reporting, reconciliation, and fraud prevention, letting your team focus on more strategic activities.

Orchestration layers enhance payment success rates by using intelligent routing to direct transactions to the most reliable gateways. In the event of a failure, the system automatically switches to backup providers. Real-time monitoring detects potential issues early, and retry logic ensures that failed payments are reattempted through alternative providers, reducing friction for customers.

An orchestration layer strengthens security by centralizing compliance management across all connected gateways. It applies consistent security protocols across multiple providers, reduces the number of direct integrations that need separate security management, and offers unified fraud detection capabilities. As new gateways are added, security standards are maintained consistently.

Recent articles