Payment API: What it is, how it works, and how to scale

Payments 101

Updated 29 Jun 2026

10 min

Andrii Kononenko

Head of Merchant Operations, Solidgate

A practical breakdown of payment APIs – components, integration, and why businesses move to a unified one.

If you've landed on this page, you're probably trying to figure out what a payment API actually is – and whether it's the missing piece in your payment stack.

Maybe you’re managing multiple providers and the overhead is starting to show, or you're planning to expand and realizing every new market means another full integration build.

Both come down to the same thing: how your payment API is set up. A direct connection to one provider at a time works until you need more than one.

A unified payment API sits across every provider you use – so routing, retries, and reporting are configurable from one place, without a new build every time something changes.

This guide covers what a payment API is, how it works, how to integrate it, and what to look for if you want infrastructure that scales with you.

TL;DR

- A payment API is a set of protocols that connects your business to payment processors, networks, and APMs

- Core components include endpoints, authentication keys, webhooks, and REST/JSON data formats

- A payment API replaces static routing and manual ops with configurable, automated logic

- Key benefits: fewer integration builds, centralized maintenance, configurable routing, and unified reporting across every provider

- Solidgate's payment orchestration API covers cards, APMs, subscriptions, smart routing, token vault, and reporting – all configurable from one place without changing your codebase.

What is a payment API?

A payment API (Application Programming Interface) is a set of protocols and endpoints that allow software systems to communicate with a payment processor or payment infrastructure platform.

A payment API gives you direct, programmable access to the payment logic itself. Routing rules, retry strategies, tokenization, webhooks, and reporting – all configurable through code, not a provider's locked-down dashboard.

How a payment gateway API works

When a customer clicks "Pay," here's what happens:

- Checkout initiation: Your frontend captures payment details via a hosted payment form or a client-side software development kit (SDK). The SDK tokenizes card data before it reaches your server, keeping raw card numbers off your systems entirely.

- Authorization request: Your server calls the payment API with transaction parameters: a payment token, amount, currency, merchant ID (MID), and any fraud signals.

- Routing decision: The API evaluates the request against routing rules – card type, Bank Identification Number (BIN), geography, and issuer preferences – and selects the optimal acquirer or processor.

- Issuer authorization: The processor forwards the request to the issuing bank. The bank approves or declines based on available funds, fraud score, and risk rules.

- Response and settlement: The API returns an authorization code or decline reason to your server. Approved transactions move to capture and settlement; declines trigger retry logic or alternative routing.

Webhooks push real-time event updates at each stage – authorized, captured, settled, disputed – so your systems react without polling.

Core insight: Understanding the API flow tells you where authorization rate losses happen and where automation can recover failed transactions before they become lost revenue.

Key components of a payment API

Endpoints are the specific URLs your system calls to initiate a charge, request a refund, check order status, or manage a subscription. A well-documented API exposes clear, versioned endpoints for every payment function: card charges, (APM) initiation, recurring billing, dispute handling, and reporting.

Authentication controls who can call the API. Most payment APIs use a public key, a secret key, and a cryptographic signature generated from both. The signature travels in each request header so the processor can verify the source and integrity of every call. Requests without a valid signature are rejected.

Webhooks and callbacks let the payment system push real-time updates to your server as events occur. A payment moves from processing to approved, a chargeback is filed, a recurring token is revoked. A webhook on a failed charge triggers a smart retry, an alert, or an account status change without manual intervention.

Data formats standardize how information is exchanged. Most modern payment APIs use Representational State Transfer (REST) architecture with JavaScript Object Notation (JSON) payloads. JSON is lightweight, human-readable, and widely supported.

Core insight: These four components determine what your payment API can do, how secure it is, and how much you can automate without manual intervention.

How to integrate a payment API

Most payment API integrations follow a consistent path to go-live:

- Get API credentials – The provider issues a public key, secret key, and merchant identifier. Credentials are split into sandbox and production environments.

- Set up the sandbox – Build and test your payment flow against the sandbox before any live transactions. Most providers supply test card numbers that simulate decline codes, 3D Secure (3DS) challenges, and edge cases.

- Build your server-side integration – Implement charge, refund, and webhook handler endpoints. Use the provider's backend SDK if available – it handles signature generation and reduces boilerplate.

- Embed the payment form – Use the frontend SDK to embed the payment form in your product. This keeps card data off your servers and simplifies Payment Card Industry Data Security Standard (PCI DSS) compliance.

- Go live – Switch to production credentials, run user acceptance testing (UAT), and monitor webhook delivery and authorization rates in the first 48 hours.

A basic card payment flow with webhooks typically takes an experienced team a few days to build. Full payment API integration – covering APMs, , reporting endpoints, and frontend SDK embedding – usually takes weeks.

Core insight: Documentation quality is a reliable signal of integration quality. A well-documented API reflects a provider that takes developer experience seriously – which matters when something needs debugging under pressure.

When your business needs a payment API

Not every business needs the same depth of API integration. But some scenarios make the need clear.

E-commerce at scale. High transaction volume requires routing control, multi-currency support, and fraud tooling that a single gateway can't provide. A payment processing API makes all of this configurable from one place – with the data granularity to spot underperforming routes before they affect revenue.

For a deeper breakdown of how routing decisions affect , see our guide.

SaaS and subscription businesses. According to Stripe, involuntary churn accounts for up to 40% of total churn. A payment API with smart retry logic, card updater services, and full lifecycle management – upgrades, downgrades, pauses, cancellations – recovers most of it automatically.

For example, Ajax Systems had no subscription billing infrastructure when they decided to launch SaaS in the EU. Using Solidgate, they went live in one week with 90%+ approval rates from day one.

→ See the full

Marketplaces and platforms. Managing payment flows across multiple merchants with split settlements, payout logic, and consolidated reporting requires API-level access to payment data.

Mobile and in-app payments. Frontend SDKs embed the payment form directly in your app. Users don't leave your product to pay – which removes a consistent drop-off point on mobile, where every extra page load and context switch costs you completions.

International payments. Cross-border payments need local acquirer , local APMs, and multi-currency pricing. Compliance requirements add another layer: Payment Services Directive 2 (PSD2), Strong Customer Authentication (SCA), and local tax rules all apply. As takes shape, API-based infrastructure makes compliance updates easier to absorb without rebuilding your core integration.

Core insight: Once you're processing in two or more markets, running recurring billing, or managing multiple providers, static infrastructure becomes the ceiling.

Why businesses move to a unified payment API

Working with multiple payment APIs at scale usually means dealing with:

- A separate build for each provider. Every PSP, digital wallet, or APM you add requires individual integration and configuration. There's no shared logic to carry over – each one starts from scratch.

- Each connection aging on its own schedule. Each provider ships security patches, compliance updates, and new features on its own timeline. Staying current across multiple APIs becomes a continuous maintenance task that grows with every connection you add.

- Separate security and data requirements. Authentication methods, encryption standards, and compliance requirements differ between providers. Your team manages each set independently, with no unified framework across them.

- Different data formats on the backend. Each provider returns transaction data in its own structure – its own decline taxonomy, settlement format, and reporting schedule. Before your finance team can analyze or act on any of it, someone has to translate and consolidate it manually, across every provider, every cycle.

Core insight: As payment stacks grow in complexity, businesses increasingly consolidate their operations under a single API integration. One connection manages access to all their payment services, reducing the overhead of running them separately.

Key business benefits of using a unified payment API

Fewer engineering resources, less ongoing overhead

With a unified API, your team builds the payment connection once – every provider, payment method, and market you add connects through what's already in place. Routing logic works the same way: you define the rules, the platform applies them across every transaction automatically. No new build per provider, no engineering sprint every time your routing strategy needs to change.

Global payment coverage through one integration

1 in 10 shoppers checkout because their preferred payment method isn't available. A unified payment API adds the local methods your customers expect in each market – PIX in Brazil, BLIK in Poland, or UPI in India – through the same integration that handles card transactions. Local takes this further: processing through a local bank in each market aligns with issuer preferences and delivers a 17.9% LTV improvement.

Centralized maintenance across all providers

Security patches, compliance updates, and provider-side changes apply at the platform level. Your engineering team stops tracking individual release cycles and chasing provider-specific updates. One maintenance task covers every connection in your stack, regardless of how many providers you run.

Consistent payment behavior across every provider

Your customers get the same payment experience regardless of which provider handles their transaction – the same form logic, the same error messages, the same retry behavior. That consistency builds trust, reduces friction at the moment it matters most, and removes a quiet but persistent source of checkout abandonment.

Unified reporting across all providers

Unified transaction data cuts the time your finance team spends on manual aggregation. Payment costs, settlement timing, and chargeback data are accessible through API endpoints or exportable reports – in one consistent format, across every provider. No more translating between settlement files before running a single report.

Core insight: Every provider, payment method, and market you add through a unified layer extends your payment coverage without extending your engineering or operational overhead.

What Solidgate's unified payment API covers

Solidgate's unified payment orchestration API covers the full – from transaction processing and to routing logic, token storage, and financial reporting.

Process every payment type from one integration

Card payments, APMs, Google Pay, Apple Pay, recurring charges, refunds, voids, and settlements all run through one API. For subscription businesses, the billing API handles the full lifecycle – create products and prices, set billing frequency, switch plans, pause, and cancel – without you building that logic in-house.

Route and manage access without engineering overhead

With Solidgate’s , you change your routing strategy from Hub without an engineering sprint.

Rules reference geography, card type, issuer, currency, transaction value, risk score, and custom metadata you define. Each route supports up to five cascade steps across card, Apple Pay, Google Pay, and network token flows – so a failed payment at one acquirer retries automatically at the next.

Every configuration change is versioned: draft before publishing, full history, one-click rollback if something breaks. A default route means no payment declines silently for a missing rule.

Access follows the same logic. Finance gets read-only, engineers get full control, and automated systems handle event verification independently – all scoped per channel. When credentials need rotating, old and new keys stay valid in parallel.

Own your customer credentials across every provider

With, Solidgate provides a scheme-issued token from Visa or Mastercard in place of raw card data. Issuers recognize these tokens as lower-risk credentials – Solidgate merchants using network tokens see improvements of up to +15%.

When a card is reissued, the token updates automatically, so the next billing cycle processes cleanly without a failed payment or a customer losing their subscription.

Those tokens are stored in Solidgate's – independently of any single acquirer, belonging to you.

If you migrate from another processor, existing stored cards transfer directly: tokens map to your current customer records without asking customers to re-enter their details. If you already have a direct integration with Visa or Mastercard's tokenization services, those tokens process through Solidgate without re-tokenization.

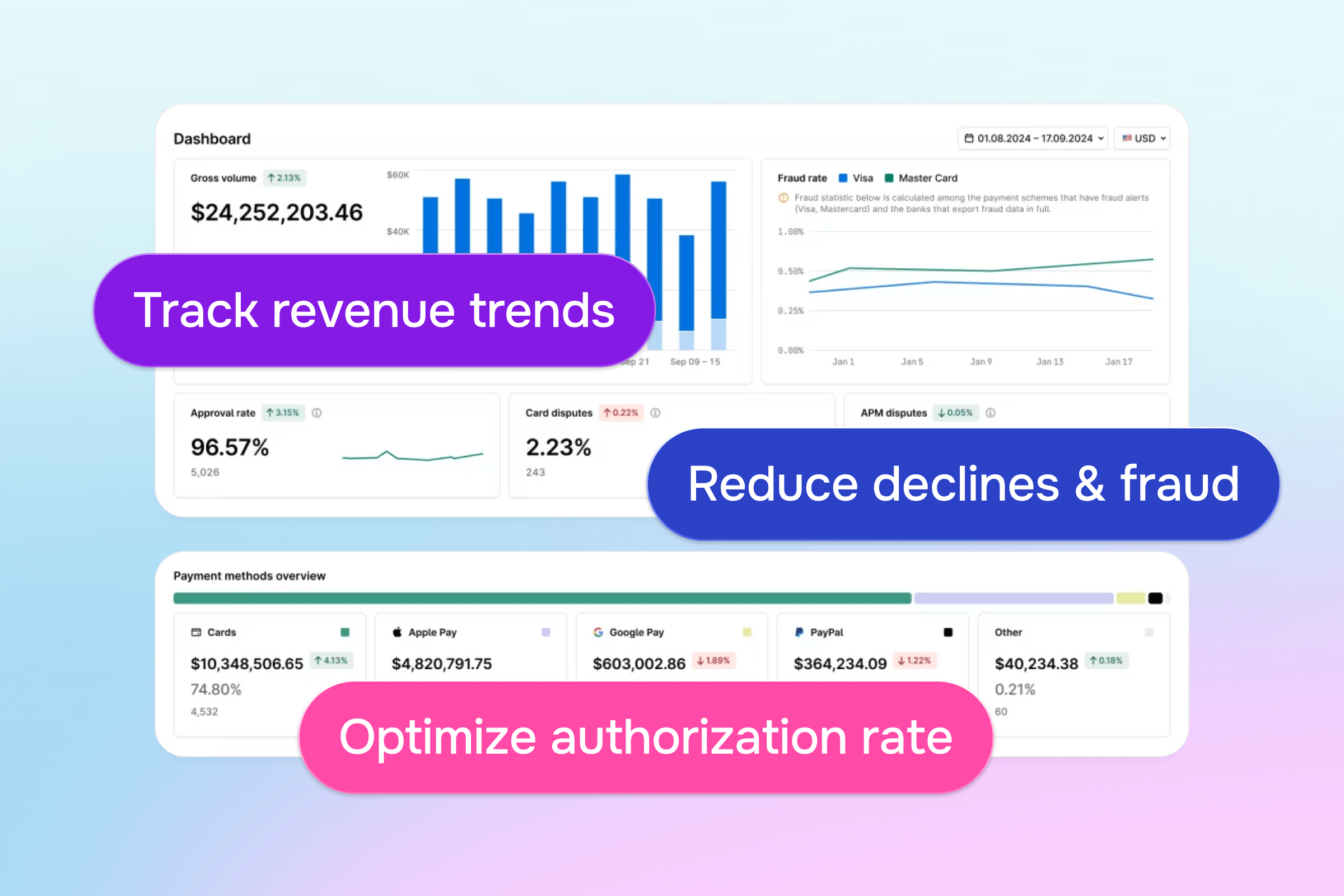

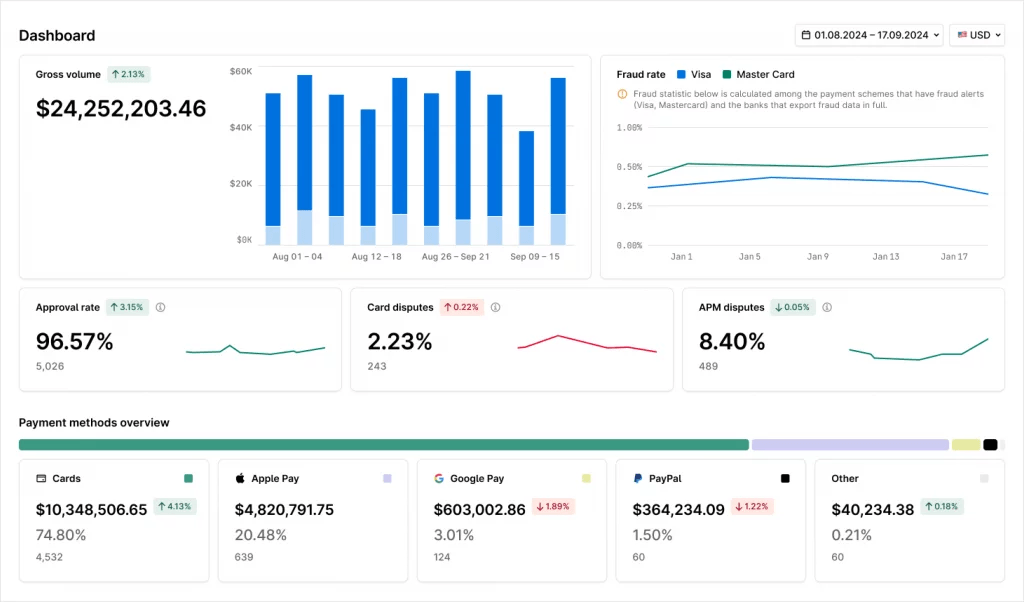

Reconcile across every provider without manual matching

Your finance team gets one view across card orders, APM orders, subscription data, chargebacks, and financial entries – all filterable by date range. Every record is broken down by provider, payment method, card brand, issuing country, fee type, and acquirer cost. Non-technical teams can pull the same data directly from Hub without touching the API.

Webhooks close the loop in real time. Your system receives signed, verifiable notifications for card order updates, APM orders, network token events, dispute alerts, fraud alerts, and subscription payment changes. So automated workflows act on outcomes directly, with no polling.

Build on the stack your team already knows

Your engineering team integrates using the stack they already work in. Frontend SDKs cover React, Vue, and Angular. Backend SDKs cover PHP, Node.js, Go, Kotlin, and Python.

The full API reference is at.

Core insight: The routing configuration, vault settings, and billing logic are all adjustable from Hub without touching your integration. When your payment setup needs to change, your codebase doesn't have to.

Control your payment infrastructure with Solidgate

Managing payments across multiple providers compounds in complexity faster than most teams plan for. A unified payment API is where that complexity starts to shrink – one integration, one control layer, one place to manage everything your payment stack needs.

That's the foundation Solidgate is built on. When your payment stack needs to change or you want clearer data across providers, you don't have to touch your code.

Ready to see what that looks like for your business? today.

Frequently asked questions

A payment API is the interface between your code and the payment processors, networks, and methods you use. When a customer pays, your system sends a request – transaction details, customer context, routing instructions – and the API handles the rest: acquirer selection, authentication, response handling.

A payment API is a technical interface – the mechanism by which your system connects to payment processors and networks. ACH (Automated Clearing House) is a specific payment network used for bank-to-bank transfers in the US. You can use a payment API to initiate ACH transactions alongside card payments, digital wallets, and other APMs.

The most widely used payment APIs come from major payment service providers – Stripe, Adyen, Checkout.com, and Braintree. These work well for businesses running on a single provider. When a business expands into multiple markets, a single PSP API starts to limit what you can do. A platform like Solidgate adds a layer on top of your existing PSPs. One API connects to multiple PSPs, with routing logic, cascading, and unified reporting across all of them.

Most online payment APIs use a combination of a public key, a secret key, and a cryptographic signature generated by hashing the two together. The merchant ID and signature pass in request headers so the payment processor can verify the source and integrity of each call. Some APIs also support IP allowlisting and webhook signature verification for additional security layers.

It depends on three things: how many payment methods you're launching with, whether you're building from scratch or using an SDK, and how complex your routing and billing logic is. A card-only setup with an SDK typically takes a few days. Adding APMs, subscription billing, and multi-acquirer routing adds two to four weeks on top of that. The biggest time sink is usually edge case testing – declined transactions, webhook retry handling, and cascade behavior.

PCI DSS compliance is the baseline. Level 1 PCI DSS certification means the provider has been independently audited against the highest security requirements. Beyond that, look for 3DS2 (3D Secure 2) support for strong customer authentication, network tokenization to avoid storing raw card data, Transport Layer Security (TLS) encryption for all API traffic, and a clear key management policy for API credentials. If you're processing in Europe, PSD2 and SCA requirements must also be supported.

Recent articles