Static vs dynamic payment routing: How to choose the right approach for your stack

Payments 101

Updated 26 Jun 2026

8 min

Anton Tsyslytskyi

Product Manager, Solidgate

Static routing sends every transaction down the same path. Dynamic routing picks the best acquirer in real time – and the difference shows up directly in your approval rates.

Your payment provider tells you your overall approval rate is 82%. Break it down by market, and Germany sits at 91% while Poland is at 67%. Same PSP, same configuration, but wildly different outcomes.

That gap is often a routing problem – specifically, a static routing problem. Businesses on static, single-acquirer setups often find their best and worst markets sitting 10+ percentage points apart on authorization rates.

The culprit here isn’t fraud or product issues, but one fixed path can't match every issuer's preferences. Switching to dynamic payment routing closes most of that gap.

This article breaks down how static and dynamic routing work, where each makes sense, and how a hybrid setup delivers the best of both.

TL;DR

- Static routing sends every transaction through a fixed, pre-configured acquirer path. Simple to set up, but inflexible at scale.

- Dynamic payment routing selects the best acquirer per transaction in real time, based on card type, issuer, geography, and live performance data. More effective at scale, but needs transaction history to calibrate.

- Most production stacks run a hybrid: static rules where performance is established, dynamic routing where conditions still vary.

What is static payment routing?

Static routing is the default setup for most businesses starting out. Your payment provider assigns a fixed path – one acquirer, one set of rules. Every transaction follows it, regardless of where the customer is or what card they're using.

The configuration is set at onboarding and rarely changes. For instance, all Visa transactions go to Acquirer A, and all Mastercard transactions go to Acquirer B. That's it. No real-time evaluation. No performance feedback loop.

What is dynamic payment routing?

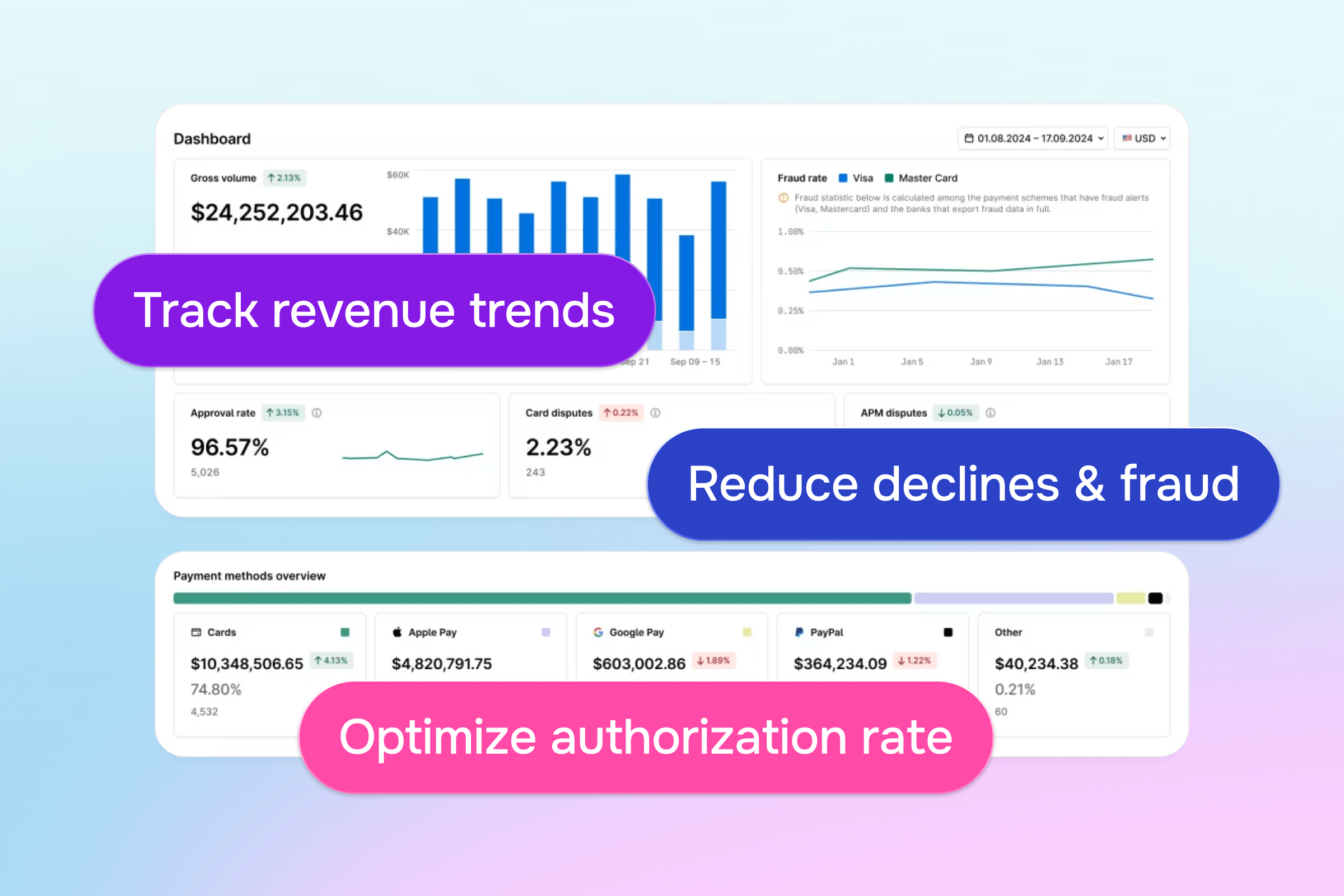

Dynamic makes routing decisions in real time, at the transaction level. Each transaction is evaluated against live performance data – card type, issuing bank, amount, geography, historical approval rates by acquirer. It then routes to the acquirer most likely to authorize it.

The routing engine runs this logic in milliseconds. While the customer sees nothing different, your authorization rate improves.

Some dynamic routing platforms incorporate machine learning to update approval probability scores continuously by acquirer and corridor.

Static vs dynamic payment routing [Comparison table]

The table below maps the key dimensions where static and dynamic routing diverge:

| Dimension | Static routing | Dynamic payment routing |

| Routing method | Fixed, pre-configured path set at onboarding | Real-time selection based on transaction data and rules |

| Adaptability | None – same acquirer for every transaction | Adjusts per card type, issuer, geography, and risk signal |

| Authorization rate | Locked to a single acquirer's performance ceiling | Routes to the acquirer with the highest approval probability |

| Failover on decline | Limited or manual – most declines are lost | Automatic retry through alternative acquirers by decline code |

| Cost efficiency | No mechanism to reduce processing fees across acquirers | Routes to lowest-cost acquirer, reducing processing fees |

| Cross-border payments | One-size-fits-all, often mismatched to local issuers | Routes to local acquirers aligned with issuer expectations |

| Fraud and compliance | Uniform 3DS approach regardless of risk | Applies authentication selectively based on risk profile |

| Performance monitoring | Manual review; outcomes visible after the fact | Real-time acquirer data continuously informs routing decisions |

| Revenue impact | Revenue loss due to unnecessary declines and rigid acquirer selection | Higher revenue retention from improved approval rates and automatic failure recovery |

| Best for | Single-market, low-volume, consistent transaction types | Multi-market, subscription-first, high-volume, cross-border |

What's the difference between static and dynamic payment routing?

The core differences between the two approaches come down to five dimensions:

Decision logic

Every time your routing sends a transaction to a provider that the issuer doesn't recognize – wrong geography, card type, or risk profile – it gets declined. found that up to 25% of card declines are false positives: legitimate transactions blocked not because of actual fraud, but because of that acquirer-issuer mismatch.

Static routing creates these mismatches systematically. It makes one routing decision at setup and applies it to every transaction indefinitely – no adjustment for shifting acquirer performance, no issuer-specific logic.

Dynamic payment routing makes a fresh decision on each transaction, matching it to the acquirer with the strongest track record for that specific card type, issuer, and geography. The mismatch rate drops, and so does the false decline rate.

Decline handling

Under static routing, a declined transaction has one path: notify the customer, retry later on the same acquirer, or lose the revenue. There's no logic connecting the reason for the decline to the response. Since every decline is treated the same, most recoverable ones aren't recovered.

Dynamic transaction routing changes this for general declines – where the issuer rejects a transaction without a specific reason. The engine reads the decline code and immediately cascades the transaction to an alternative acquirer. Rerouting on a general decline recovers 20–25% of transactions that would otherwise be permanently lost.

Timing-based recovery – retrying insufficient funds declines at the right window, stopping retries on hard declines – is handled by a smart retries engine that sits alongside routing. Together, the two systems cover the full picture.

Cost and approval control

Route to the wrong acquirer for a corridor and you pay more while approving less. Static routing has no mechanism to prevent this – one acquirer handles every transaction at a fixed rate regardless of geographic fit or cost.

Dynamic routing evaluates both approval probability and processing cost on every transaction. It selects the acquirer with the strongest issuer relationships in that market and the most competitive fee for that corridor.

In high-volume corridors, that selection repeated across thousands of transactions produces measurable improvements in both processing margin and authorization rates.

Adaptability

When major networks implement new authorization rules, static routing can see approval drops by up to 5–10%. When conditions shift, it keeps routing transactions the same way until someone identifies the cause and manually reconfigures the rules.

Dynamic payment routing responds to the same changes in real time. Routing logic updates continuously based on live approval rate data – when a corridor starts underperforming, volume shifts to a better-performing acquirer automatically. No manual diagnosis. No reconfiguration window. No approval rate gap while the team catches up.

Fraud and compliance

Static routing applies 3DS () uniformly – the same approach on every transaction regardless of risk level, geography, or transaction type. In markets with SCA (Strong Customer Authentication) requirements like the EU, that creates a binary problem.

Applying it to every transaction adds friction that hurts conversion. Skipping it on lower-risk transactions creates compliance exposure.

Dynamic routing, paired with an SCA exemption layer, can apply authentication selectively based on transaction risk signals. Low-risk transactions from trusted devices in familiar geographies pass through without a challenge. Higher-risk transactions trigger 3DS.

The result is a setup that meets regulatory requirements without applying authentication overhead to transactions that don't need it.

Core insight: Static routing executes the same rule on every transaction. Dynamic payment routing makes a new decision on each one – informed by live data, decline signals, cost, and geography.

When static payment routing still makes sense

Static routing works well when you're processing in a single market with one acquirer and your transaction mix is predictable:

- There's no geographic complexity to route around

- No issuer variance to account for

- No high-volume subscription renewals to protect

A single well-configured relationship covers the job cleanly. The simpler the setup, the less there is to break and the faster your team can focus on product rather than .

Static routing is also a legitimate starting point in a new market. Dynamic payment routing needs transaction history to calibrate – approval rate data by corridor, decline patterns by card type, acquirer performance benchmarks.

Without that data, the routing engine has no performance baseline to work from. Static routing builds that history. Once you have six to twelve months of transaction data in a new corridor, you have the inputs to make dynamic routing work.

Core insight: Static routing works well when your volume is low and your market is single.

When dynamic payment routing becomes essential

Dynamic routing pays off most when transaction complexity outpaces what a fixed path can handle. There are three scenarios where this threshold is typically crossed:

Subscription billing at scale

Recurring payments face more issuer scrutiny than one-time transactions. Card data changes over time – expiry, reissuance, or closure. Dynamic routing routes each renewal to the acquirer with the best track record for that card type and billing window.

Combined with a engine that handles timing-based recovery, businesses recover an average of +11.6% of failed renewal attempts.

Cross-border expansion

When you expand into a new market using an international acquirer, local issuers treat your transactions as foreign and decline them at higher rates. Dynamic routing in payments addresses this directly, automatically routing cross-border transactions to local acquirers with established issuer relationships in the target market.

Across Solidgate's merchant base, switching to local acquiring increases by up to +17.9% in.

Processing cost under volume pressure

Processing fees vary by acquirer, card type, and geography – and at scale, that variance adds up. Without routing logic, you have no lever to manage it. Dynamic routing applies least-cost routing as one dimension of every routing decision, selecting the most cost-effective acquirer for each corridor without sacrificing authorization rates. At $5M+ monthly processing, a 3–5 percentage point improvement in routing efficiency translates to $1.8M–$3M in recovered margin annually.

Core insight: Dynamic payment routing becomes essential when subscription renewals, cross-border expansion, or processing cost at scale create gaps that a fixed routing path can't close.

The hybrid approach: combining static and dynamic rules

Most production payment stacks don't run pure static or pure dynamic routing. They run a hybrid: static rules govern high-certainty scenarios, and dynamic logic handles everything else.

MEGOGO, the international OTT streaming platform, ran into this decision directly. Their single-path setup handled domestic transactions well, but after they expanded into Poland and other markets, their approval rates varied by region. Per-transaction fees were constraining subscription economics, and renewal failures were driving preventable churn.

Working with Solidgate, they rebuilt their payment infrastructure around an layer that could route each market on its own terms.

In priority markets like Poland, they locked in local acquiring relationships with negotiated rates – fixed, predictable, and optimized for that corridor. For everything else, dynamic routing directed each transaction to the acquirer with the best combination of approval rate and cost for that scenario.

Routing locally in Poland also made BLIK available – an used by most Polish consumers that an international acquirer couldn't offer.

The result: +3.5% in payment conversion, -5% in subscription churn, and €100K in annual cost savings.

Read the full .

Core insight: Most mature payment stacks run a hybrid – static rules where performance is established, dynamic routing where conditions still vary.

Payment orchestration handles the routing decision for you

Static and dynamic routing are complementary tools that work best when something sits above them and decides which to apply, when, and for which corridor. Without that layer, the hybrid approach becomes a manual configuration problem.

Someone on your team has to monitor acquirer performance, identify underperforming corridors, and reconfigure rules every time conditions shift.

Payment orchestration removes that overhead. The routing logic – when to apply fixed rules, when to switch to dynamic selection, how to recover a failed transaction – runs automatically. It’s informed by live performance data across every acquirer in your stack.

If you're processing across multiple markets, explore Solidgate's or to discuss your setup.

Frequently asked questions

Static routing sends every transaction through a fixed, pre-configured acquirer path. It makes one routing decision at setup and applies it indefinitely. Dynamic payment routing makes a fresh decision on each transaction, selecting the acquirer with the highest approval probability based on card type, issuer, geography, and live performance data.

Dynamic routing matches each transaction to the acquirer most likely to authorize it, reducing false declines from acquirer-issuer mismatches. For general declines, it cascades immediately to an alternative acquirer. For cross-border transactions, it routes to local acquirers with established issuer relationships. For high-volume corridors, it selects the most cost-effective acquirer without sacrificing authorization rates.

Yes – and most mature payment stacks do exactly this. Static rules govern high-certainty corridors where acquirer performance is predictable. Dynamic routing handles everything else. A payment orchestration layer manages both automatically, without manual reconfiguration every time conditions shift.

Recent articles