Payment infrastructure: The complete guide for scaling businesses

Payments 101

Updated 16 Jul 2026

12 min

Artem Sadurskyy

Chief Product Officer, Solidgate

There's more happening behind your checkout than a gateway and a bank. Here's the full picture – how payment infrastructure works, where the money leaks, and how to stop it.

Most businesses don't think about payments infrastructure until it starts costing them:

- Authorization rates

- A subscription renewal campaign that returns fewer recovered payments than expected

- Finance spending two days a month reconciling settlement files across multiple providers

- A new market launch that stalls because the current provider doesn't support the local payment method customers expect

By the time those symptoms are visible, the infrastructure question is already overdue.

This guide covers what payment infrastructure actually is, how each layer works, where fragmented setups leak money, and what a practical improvement roadmap looks like.

TL;DR

- Payment infrastructure is the full technical and financial stack beneath every transaction – from checkout and routing to acquiring, settlement, and reconciliation.

- Most businesses hit a performance ceiling because their infrastructure is missing routing logic, local acquiring coverage, or retry intelligence.

- Fragmented setups leak revenue in four specific ways: authorization rate gaps, involuntary churn on subscription renewals, reconciliation overhead, and cross-border cost premiums.

- To improve your payments stack, focus on five levers: smart routing, network tokenization, intelligent retry logic, local payment method coverage, and centralized payment data.

- The choice between building, buying, or adding an orchestration layer depends on your volume, market footprint, and how much engineering time you can afford to spend.

What is payment infrastructure?

Payment infrastructure is the end-to-end system that enables a business to accept, process, and settle digital payments. It's not a single product or vendor. Businesses typically work with multiple payment infrastructure providers to handle everything from the moment a customer clicks "pay" to the moment funds land in their account.

Most people think of it as the checkout form and maybe the payment gateway behind it. But that's only the front end. Underneath is a more complex set of layers:

- The checkout and payment form that captures and transmits payment data

- The routing and authorization logic that decides which bank processes a transaction

- The card network rails that carry the transaction data

- The issuing bank that approves or declines it

- The settlement engine that moves cleared funds back to you

When that stack works well, it's invisible. When it doesn't – authorization rates drop, customers see errors at checkout, reconciliation takes days, and revenue disappears quietly into the gap between "attempted" and "collected."

Layers of payment infrastructure

The front-end layer: Checkout and acceptance

This is what your customer sees. It includes the checkout experience – either a hosted page that redirects to a provider's domain, or an that sits directly on your site.

It also covers the payment methods on offer (cards, digital wallets, buy now pay later, local alternatives) and the authentication layer. That includes 3D Secure (3DS) – the step-up challenge issuers use to verify cardholder identity.

The middleware layer: Routing, authorization, and risk

This is the intelligence layer. It sits between the checkout and the financial rails, and it's where most of the optimization work happens.

The key components here are:

- The payment gateway (the technical connection point between your platform and the acquiring bank)

- The (PSP), which may combine the gateway with acquiring services

- The routing logic that decides which acquirer gets each transaction

- The fraud and risk screening tools that score transactions before they're submitted for authorization

Explore the difference between a payment in our guide.

The back-end layer: Acquiring, networks, and settlement

This is the financial rails layer. It includes:

- The acquiring bank (the institution that processes card transactions on your behalf and holds a merchant account)

- The card networks (Visa, Mastercard) that carry authorization requests between acquirers and issuing banks

- The issuing bank that actually approves or declines the transaction on behalf of the cardholder

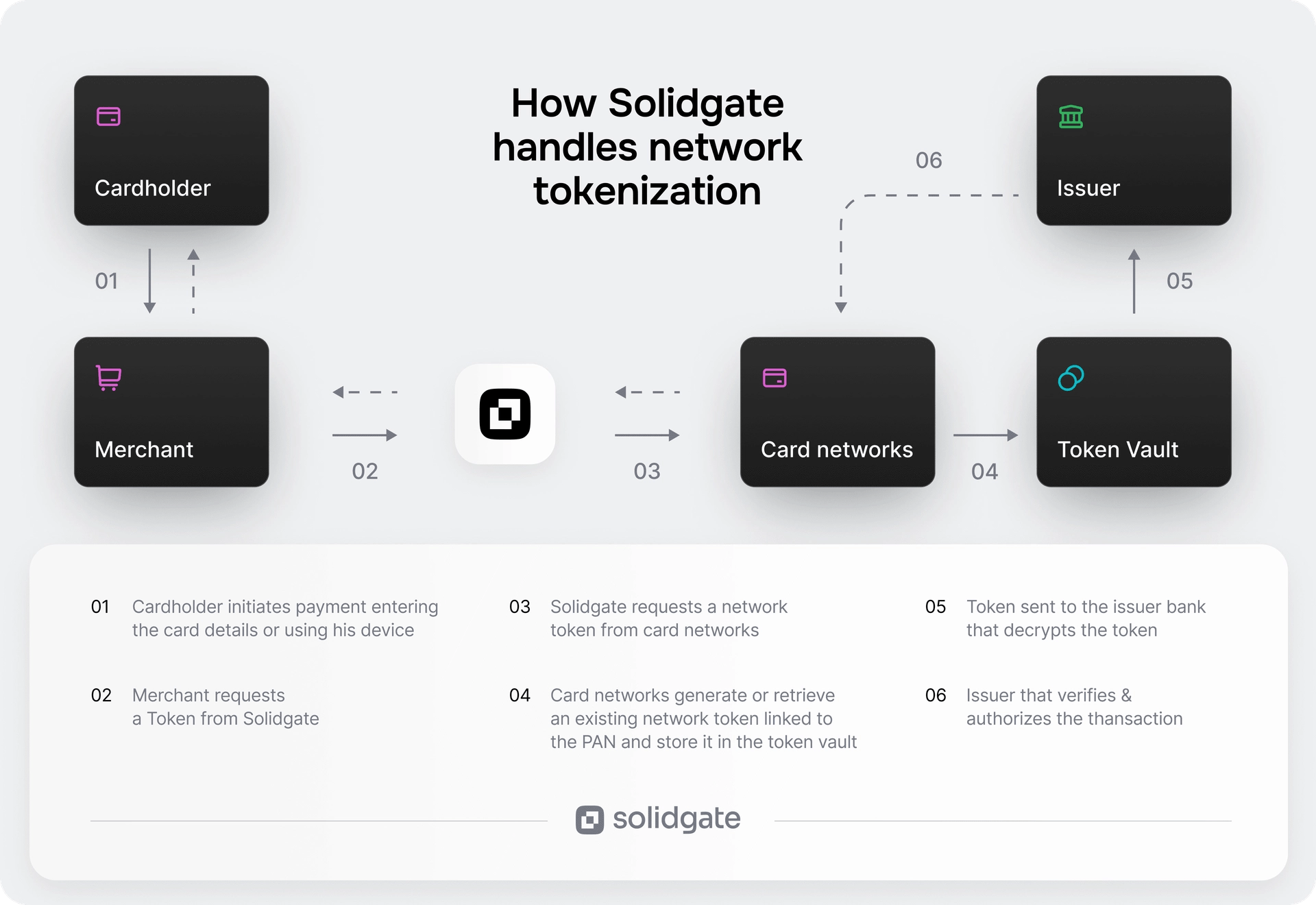

– specifically Visa Token Service (VTS) and Mastercard Digital Enablement Service (MDES) – sits in this layer too. It replaces static card numbers with dynamic network tokens that issuers treat as more secure.

Settlement and reconciliation also live here. Once a transaction clears, funds move through the acquiring bank to your settlement account, typically on a T+1 or T+2 cycle depending on your acquiring arrangements.

Core Insight: Most of the optimization work in your payments stack happens at the middleware layer – routing, authorization, and risk.

How payment infrastructure works: The transaction flow

Understanding the transaction flow helps you diagnose where things break. Here's what happens in the roughly two seconds between a customer clicking "pay" and getting a confirmation:

- Checkout submission. The customer enters card details or selects a wallet. The payment form tokenizes the card data and submits it to the payment gateway.

- Fraud screening. Before the transaction is submitted for authorization, risk tools score it. Suspicious transactions can be blocked or stepped up to 3DS challenge.

- 3DS (where required). Under and Strong Customer Authentication (SCA) rules in Europe, many transactions require a cardholder verification step. Liability for fraudulent transactions shifts to the issuer when 3DS is completed successfully.

- Authorization request. The gateway routes the transaction to the acquiring bank, which forwards the authorization request through the card network to the issuing bank.

- Issuer decision. The issuing bank approves or declines. A hard decline means the transaction can't be retried (stolen card, do not honor). A soft decline – insufficient funds, technical issue – can often be recovered with a retry through a different acquirer or at a different time.

- Response routing. The authorization response travels back through the network to the acquirer, then to the gateway, then to the merchant.

- Capture and settlement. Authorized transactions are captured (the funds are claimed) and batched for settlement. The clearing process moves funds through the network; settlement deposits them into your merchant account.

Core Insight: A payment transaction moves through six sequential steps – checkout submission, fraud screening, 3DS authentication, authorization request, issuer decision, and capture/settlement.

The real cost of fragmented payments infrastructure

Most businesses don't calculate what their payment setup actually costs them. They look at the processing fee line and stop there. But the real cost is wider.

Authorization rate gaps

– the share of attempted transactions that get approved – vary significantly by acquirer, corridor, and card type. A business routing all transactions through a single provider in markets where that provider doesn't have strong local acquiring relationships will see unnecessary declines. Those aren't visible as a cost; they show up as missing revenue.

The gap between a well-optimized multi-acquirer setup and a single-provider setup can be 5–15 percentage points in approval rate, depending on the market. On a $5M/month processing volume, that difference is material.

Involuntary churn in subscription businesses

For subscription businesses, failed renewal payments are a direct drain on net revenue retention. Businesses can show average monthly involuntary churn rates ranging from 5.6% to 8.3% depending on vertical.

The cause is almost always preventable: expired cards, reissued card numbers that the billing system doesn't recognize, or soft declines that weren't retried intelligently.

Operational overhead at scale

A business running payments through multiple providers without a centralized reconciliation layer typically reconciles manually. This includes downloading settlement files from each provider, matching them against internal order data, and resolving discrepancies by hand.

At low volume, that's manageable. At $5M+ monthly, it consumes significant finance team time and introduces reconciliation errors.

Cross-border processing costs

Cross-border transactions carry interchange fees, scheme fees (charged by Visa and Mastercard), and FX conversion markups. Without the ability to route transactions to a local acquirer – one that can process in the customer's domestic market – every cross-border sale carries a cost premium that erodes margin.

Single-provider dependency risk

A business that routes all payment volume through one provider has no failover if that provider has an outage or degrades its approval performance. The payment stack becomes a single point of failure for revenue.

The dependency problem extends far beyond outages. If your provider's approval rate drops due to a change in their issuer relationships or routing configuration, you have no visibility into why and no lever to pull.

Core Insight: Fragmented payment infrastructure creates five cost categories. These are authorization rate gaps, involuntary subscription churn, manual reconciliation overhead, cross-border processing premiums, and single-provider dependency risk.

How to upgrade your payments infrastructure

Here's how to optimize your payments stack systematically:

Diagnose before you fix

Before changing anything, get a clear picture of where your current setup is underperforming. Pull authorization rates by market, acquirer, and card type. Identify where soft declines are clustering and what the primary decline codes are. Calculate your monthly involuntary churn rate for subscription renewals. Measure your reconciliation cycle time.

Most businesses can't answer these questions cleanly because their payment data sits across multiple provider dashboards. Getting it into one view is the precondition for everything else. You can't fix a routing problem you haven't located.

Add routing logic

If you're sending all transactions to one acquirer, adding a second provider without routing logic just doubles your integration overhead. The value of multi-acquirer infrastructure comes from the routing and cascading on top of it. This means directing each transaction to the acquirer most likely to approve it, and automatically falling back to a secondary when the primary declines.

Routing decisions can be based on:

- Geography (send Brazilian transactions to an acquirer with local acquiring in Brazil)

- Card type (route debit separately from credit, since approval rates differ)

- Issuer behavior (some issuers respond better to specific acquirers)

- Real-time performance data

Businesses that route transactions to the best-performing acquirer per market can see approval rate improvements of 5–10%. A Visa debit card from a Polish issuer gets routed differently from a Mastercard credit card from a UK issuer, even in the same checkout session. This is in practice.

Enable network tokenization

If you're not yet using VTS and MDES network tokenization, this is one of the highest-return improvements available. Tokenized transactions see better approval rates because issuers treat them as more secure – there's lower antifraud friction applied at the issuer level.

shows the surge in tokenized transaction volume delivered a 6% improvement in approvals and up to 30% reduction in fraud. Across the Solidgate merchant base, the gains go further – tokenized transactions outperform non-tokenized ones by up to 15 percentage points in acceptance rate.

Tokens also survive card reissuance, which directly reduces involuntary churn. The LTV impact, combining acceptance, retention, and one-click upsell conversion, is estimated at up to 42.5% over the customer lifecycle.

For Zeely, network tokenization delivered a 7–14 basis point lift in conversion rates after going live. When one of their tier-2 acquirers shut down, all tokens were preserved on the Solidgate side – the entire recurring payment tail transferred to the new acquirers with near-zero loss.

See the full .

Expand local payment method coverage

In most markets, there's at least one payment method that commands significant customer preference that card-only setups miss. iDEAL in the Netherlands, BLIK in Poland, PIX in Brazil, UPI in India.

The gap isn't just conversion rate – it's trust. A checkout that doesn't offer the method a customer expects signals that the merchant isn't local, which increases abandonment even for customers who do have a card. According to , 10% of shoppers leave because their preferred payment method isn’t present.

Enabling requires either building direct integrations (slow, maintenance-heavy) or accessing them through a provider that already has them live.

Through a single Solidgate integration, Nova Post went live with PayPal, BLIK, iDEAL, and Open Banking across 15+ markets – two weeks average onboarding per country, no additional development work per market.

See the full .

Implement smart retry logic for subscription renewals

A failed subscription renewal is not a lost customer. Soft declines account for 80–90% of all failed card-not-present payments – and the right retry strategy recovers 40–70% of them.

An "insufficient funds" decline from a consumer debit card retries differently from a "do not honor" from an issuer. The former often recovers with a retry in a different billing window, the latter may need a different acquirer. Time zone and billing calendar matter too: retrying a renewal in the middle of the night in the customer's local market reduces recovery rates compared to retrying during typical banking hours.

logic segments attempts by decline code and aligns timing to the cardholder's billing cycle. It also stays within card scheme retry limits – allows up to 20 retries within 30 days.

Across Solidgate's merchant base, intelligent retries deliver a +11.6% average LTV lift from recovered soft declines. First retry conversion improves by 51–67%, and retries made at the wrong time drop by 42.1% – which lowers transaction fees and protects issuer relationships.

Centralize your payment data

Manual reconciliation across providers consumes finance team time, introduces matching errors, and slows the close cycle. A unified payments view eliminates that work and flags exceptions automatically.

Your finance team gets a single source of truth for reporting, and ops can spot performance issues faster.

Core Insight: There are five levers to improve your payment processing infrastructure: smart routing, network tokenization, intelligent retries, local payment methods, and centralized data.

Build, buy, or orchestrate? Choosing your payment infrastructure approach

Most businesses face this question when they've outgrown their initial payment setup. There are three realistic paths.

Build in-house

Building payment infrastructure in-house gives you full control – over routing logic, data, acquirer relationships, and product decisions. It's the approach used by the largest platforms, where payment volume justifies the investment and custom infrastructure is a competitive advantage.

The cost is significant. Maintaining direct bank and network relationships, managing (Payment Card Industry Data Security Standard) compliance, building and operating the routing, tokenization, and reconciliation layers in-house requires a dedicated engineering team and years of accumulated operational knowledge.

Works best for: Businesses processing $1B+ in annual volume, where payments are a core product differentiator and engineering investment is justified.

Not the right fit if: You want to ship fast, expand into new markets, or focus engineering on your core product.

Buy a point solution

Point solutions – a PSP for card processing, a separate tool for subscription billing, another for fraud – are how most businesses start. They're fast to set up and well-suited to early-stage needs.

The limitation shows up at scale. Each additional provider adds integration work, a separate data silo, and another reconciliation source. When you add a second acquirer for failover or cost optimization, you're managing two integrations independently. When you need local acquiring in a new market, that's a third.

Works best for: Early-stage businesses or those with narrow payment needs in a single market.

Not the right fit if: You're operating in multiple markets, running subscriptions, or managing multiple acquirer relationships.

Orchestrate

sits as a layer above your existing and future PSP relationships. Rather than replacing your current providers, an orchestration platform connects to them through a single API and adds the routing, tokenization, retry, and reconciliation logic on top.

The practical implications:

✔️You can add a new provider or a payment method for a new market without rebuilding your integration.

✔️You can switch the primary provider for a card type without touching your checkout.

✔️You can apply smart retry logic across multiple providers without building it yourself.

Through Solidgate, Tickets Travel Network got access to, which enabled a localized payment experience across North America, Europe, LATAM, India, and SEA. The company added Tier-1 payment vendors to their existing stack in a few clicks, with zero development effort per integration.

Read the full .

Works best for: Mid-market businesses processing across multiple markets, managing subscriptions, or with more than one PSP relationship.

Not the right fit if: You're at a very early stage with a single market and minimal volume – the overhead isn't justified yet.

Build vs. buy vs. orchestrate: A comparison table

| Approach | Upfront investment | Time to market | Flexibility | Best for |

| Build in-house | Very high | Slow | Full control | $1B+ TPV, payments as core product |

| Point solutions | Low | Fast | Limited at scale | Early stage, single market |

| Orchestration | Medium | Fast | High | Multi-market, multi-acquirer, subscriptions |

Core Insight: Businesses choose between three payment infrastructure approaches: building in-house, buying point solutions, or adding an orchestration layer. Building suits $1B+ TPV businesses that treat payments as a core product. Point solutions fit early-stage, single-market operations. Orchestration fits mid-market businesses running multiple acquirers, markets, or subscriptions.

Scale your payment infrastructure with Solidgate

Solidgate is a built for digital businesses processing across multiple markets. The platform connects to 100+ global and local acquirers, PSPs, and AMPs through a single API, so adding a new acquirer or payment method doesn't require rebuilding your integration.

On top of that connectivity, Solidgate provides:

- that directs each transaction to the best-performing acquirer in real time

- Network tokenization through VTS and MDES for better issuer acceptance and subscription continuity

- Smart retry and dunning logic for subscription renewals

- Value-added services such as subscription billing management, automated chargeback prevention and representment, fraud screening, and tax compliance

If your payments stack is starting to show strain, to identify where the gaps are and what fixing them is worth at your volume.

Frequently asked questions

A payment gateway is one component within a broader payment infrastructure. It handles the technical connection between a merchant's checkout and the acquiring bank – transmitting authorization requests and returning responses. Payment infrastructure encompasses everything else: the acquiring relationships, the routing and retry logic, the fraud screening layer, the card network rails, settlement, reconciliation, and compliance tooling.

Modern payment infrastructure is modular and acquirer-agnostic. An orchestration layer is connected to multiple acquirers and payment methods – with routing logic that optimizes each transaction based on geography, card type, and performance data. It often includes a token vault that keeps payment credentials portable across providers.

Solidgate, for example, connects merchants to 100+ global and local acquirers through a single API, with network tokenization, smart routing, subscription management, and reconciliation built into one platform.

Digital payment infrastructure costs fall into two buckets. Hard costs include interchange fees (set by card networks), scheme fees charged by Visa and Mastercard, acquirer or PSP processing fees, and any platform or subscription fees for orchestration tools. Soft costs include engineering time maintaining integrations, finance team time on manual reconciliation, and revenue lost to authorization rate gaps and involuntary churn.

Start with a diagnostic: your authorization rate by market and acquirer, your involuntary churn rate and primary decline codes, and your reconciliation cycle time. The highest-impact improvements for most mid-market businesses are:

- Adding smart routing across multiple acquirers

- Enabling network tokenization for better issuer trust and card continuity

- Implementing intelligent retry logic for subscription renewals

- Adding local payment methods in each target market

If you're running those capabilities across separate point solutions, consolidating them into a single orchestration layer reduces operational overhead and gives you a unified data view.

Recent articles